Call Girls Banaswadi Just Call 👗 7737669865 👗 Top Class Call Girl Service Ban...

Senior Project Analyst Report

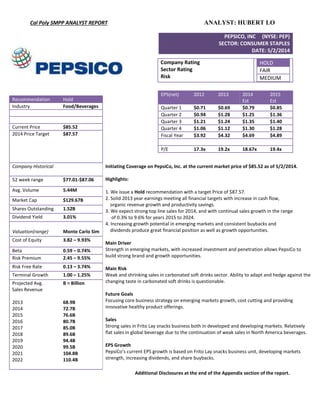

1. Cal Poly SMPP ANALYST REPORT ANALYST: HUBERT LO

Additional Disclosures at the end of the Appendix section of the report.

PEPSICO, INC (NYSE: PEP)

SECTOR: CONSUMER STAPLES

DATE: 5/2/2014

EPS(net) 2012 2013 2014

Est

2015

Est

Quarter 1 $0.71 $0.69 $0.79 $0.85

Quarter 2 $0.94 $1.28 $1.25 $1.36

Quarter 3 $1.21 $1.24 $1.35 $1.40

Quarter 4 $1.06 $1.12 $1.30 $1.28

Fiscal Year $3.92 $4.32 $4.69 $4.89

P/E 17.3x 19.2x 18.67x 19.4x

Company Rating

Sector Rating

Risk

HOLD

FAIR

MEDIUM

Recommendation Hold

Industry Food/Beverages

Current Price $85.52

2014 Price Target $87.57

Company Historical Initiating Coverage on PepsiCo, Inc. at the current market price of $85.52 as of 5/2/2014.

Highlights:

1. We issue a Hold recommendation with a target Price of $87.57.

2. Solid 2013 year earnings meeting all financial targets with increase in cash flow,

organic revenue growth and productivity savings.

3. We expect strong top line sales for 2014, and with continual sales growth in the range

of 0.3% to 9.6% for years 2015 to 2024.

4. Increasing growth potential in emerging markets and consistent buybacks and

dividends produce great financial position as well as growth opportunities.

Main Driver

Strength in emerging markets, with increased investment and penetration allows PepsiCo to

build strong brand and growth opportunities.

Main Risk

Weak and shrinking sales in carbonated soft drinks sector. Ability to adapt and hedge against the

changing taste in carbonated soft drinks is questionable.

Future Goals

Focusing core business strategy on emerging markets growth, cost cutting and providing

innovative healthy product offerings.

Sales

Strong sales in Frito Lay snacks business both in developed and developing markets. Relatively

flat sales in global beverage due to the continuation of weak sales in North America beverages.

EPS Growth

PepsiCo’s current EPS growth is based on Frito Lay snacks business unit, developing markets

strength, increasing dividends, and share buybacks.

52 week range $77.01-$87.06

Avg. Volume 5.44M

Market Cap $129.67B

Shares Outstanding 1.52B

Dividend Yield 3.01%

Valuation(range) Monte Carlo Sim

Cost of Equity 3.82 – 9.93%

Beta 0.59 – 0.74%

Risk Premium 2.45 – 9.55%

Risk Free Rate 0.13 – 3.74%

Terminal Growth 1.00 – 1.25%

Projected Avg.

Sales Revenue

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

B = Billion

68.9B

72.7B

76.6B

80.7B

85.0B

89.6B

94.4B

99.5B

104.8B

110.4B

2. Company Profile

PepsiCo Inc.

HQ Purchase, NY

Primary

Industry

Snacks &

Beverages

CEO Indra Nooyi

Exhibit 1: Sales Revenue in Products and

Geographies

Exhibit 2: Sales Revenue & Growth %

Breakdown

Business Description:

PepsiCo, Inc. is a leading company within the consumer staples sector that produces and sells food,

snacks, and beverages on a global basis. In 2012, PepsiCo owned 22 brands that each generated $ 1

Billion or more in annual retail sales. Some of company’s signature snack brands include: Lay’s

Ruffles, Doritos, Cheetos, Quaker Oatmeal; its beverage portfolio includes Pepsi, 7up, Mountain

Dew, Tropicana, Aquafina, and other beverage products.

As of 2013, the food snacks portfolio generates 52% of the company revenue, while the other 48% is

generated by its beverages portfolio. Snacks business generates 66% of growth in company while

beverages generate 33% growth. U.S. and other developed markets account for 65% of sales while

the developing/emerging markets account for 35%. In terms of growth, 66% is generated by

developing/emerging markets and 33% is in developed markets. Company is evenly split with 51%

of net revenue coming from outside U.S. and 49% within U.S.

Sales Performance: PepsiCo consists of 3 business units with six global segments: PepsiCo

Americas Food (PAF) which includes Frito Lay North America (FLNA), Quaker Foods North

America (QFNA), and Latin America Foods (LAF); PepsiCo Beverages America (PAB) which

includes all of its businesses in Europe and Asia, Middle East, and Africa (AMEA). In 2012, net

revenues were represented by the following in percentage, PepsiCo Americas Food (PAF) 37%,

PepsiCo Beverages America (PAB) 33%, PepsiCo Europe 20%, and PepsiCo AMEA 10%. The

following is a chart in terms of sales performance of 2012 FY vs 2013 FY in segments. We continue

to see strong growth in the foods/snacks business and markets outside of U.S. especially Latin

America and AMEA(Asia, Middle East, and Africa) markets, while the beverages continues to shrink

due to its weakening sales in the carbonated soft drinks business (CSD).

Organic Revenue Growth within Global Segments

FY 2012 FY 2013

PepsiCo Americas Food 7% 7%

Frito Lay North America 4% 4%

Latin America Foods 14% 13%

Quaker Foods North

America

1% -0.5%

PepsiCo Beverages 1.5% -1%

Europe 4% 3.5%

Asia, Middle East, &

Africa

10% 11%

Overall 5% 4%

Sales Revenue within Global Segments

FY 2011 FY 2012 FY 2013

Frito Lay North

America

$13.32B $13.57B $14.12B

Latin America

Foods

$7.15B $7.78B $8.35B

Quaker Foods

North America

$2.65B $2.63B $2.61B

PepsiCo Beverages $22.41 B $21.40B $21.06B

Europe $13.56B $13.44B $13.75B

Asia, Middle East,

& Africa

$7.39B $6.65B $6.50B

Overall $66.50B $65.49B $66.41B

3. Cal Poly SMPP ANALYST REPORT ANALYST: HUBERT LO

Exhibit 3: Three Different Brand images

Fun-For-You

Better-For-You

Good- For – You

Exhibit 4: PepsiCo Products Globally

Company Strategy:

I. Brand Restructuring – build healthy brand image

PepsiCo played its brand strategy as its forefront in catering to the global changing trend of health

aware consumers by creating new innovative products as well as brand restructuring. Its brands are

segmented into three different brand images: Fun- for- You, Better- for – you, and Good – for –

you.The Fun – for – you brand includes treats and snacks that are beloved and are core of PepsiCo.

Its Better-for – you brands are low fat snacks, whole grains snacks, beverages with fewer or zero

calories and less added sugar. It’s Good- for- You portfolio is comprised of nutritious foods and

beverages, products with fruits, vegetables, low fat dairy, nuts, seeds and nutrients with levels of

sodium, sugar, and saturated fat in line with dietary recommendations.

II. Emerging and Developing Markets Growth Potential – grow market share

PepsiCo has continued its aggressive investments in emerging and developing markets. As of 2012,

PepsiCo was #1 food and beverage business in Russia, India, and Middle East. And #2 food and

beverage business in Mexico, and top 5 food and beverage businesses in Brazil, Turkey and many

other markets. Latin America delivered 13% organic revenue growth, with net revenue increased by

7% in 2013.

In January 2014, PepsiCo announced its plans to spend $5 billion in the next 5 years in Mexico

toward brand building, expanding products, production capacity and infrastructure. AMEA (Asia,

Middle East, Africa) has delivered great growth as well, in 2012 and 2013; organic revenue grew by

10% and 11% respectively, with PepsiCo making deals with Suntory Holdings Limited and Tingyi

Asahi Beverages Holding Co. Ltd, opening doors to efficient bottle refranchising and distribution in

Vietnam and China markets. On Feb 27, 2014, Shanghai Disney Resort announced a multi-year

strategic alliance with PepsiCo, Inc. and Tingyi Holding corp. which recognized PepsiCo and Tingyi

Holding as the primary beverage suppliers to the resort. Moreover, in Nov 2013, PepsiCo announced

that it will invest $5.2 billion in India by 2020 to increase its manufacturing capacity and innovation

of products.

In detail, PepsiCo has created new products to its portfolio catering to regional preference and taste.

For example, in 2012 and 2013, PepsiCo added Gatorade grapefruit drink, Lipton milk tea, Mirinda

plum and peach flavors, and also Sha La Cui, a new chip product that tastes like baked salad, all

catered toward the Chinese market. PepsiCo in 2014 will continue to innovate new products and

increase its diversified portfolio to cater to the changing international taste.

Global Sales Revenue Comparison

Sales Revenue FY 2012 FY2013

United States 33.34B 33.62B

Russia 4.86B 4.90B

Mexico 3.95B 4.30B

Canada 3.29B 3.19B

United Kingdom 2.10B 2.11B

Brazil 1.86B 1.83B

All Other Countries 16.07B 16.38B

Total 65.49B 66.41B

4. Exhibit 5: Net Change in Cash Graph

Exhibit 6: Dividend Payout Ratio Graph

Exhibit 7: Common Shares Outstanding

Industry Leaders Comparison

REV MCAP NOI

PepsiCo,

Inc.

66.4B 132.1B 6.7B

The Coca

Cola

Company

46.8B 179.6B 8.5B

Dr.

Pepper

5.9B 11.1B 624M

REV = Sales Revenue

MCAP = Market Capitalization

NOI = Net Income

III. Cash Flow, dividends, share buybacks – creating shareholder value -

PepsiCo is a company that values its shareholders immensely. It prides itself in creating value for the

shareholder by increasing cash flow, growing dividends and repurchasing share buybacks from year

to year. PepsiCo increased in 10 percent in 2013 to $8.2 billion and expects free cash flow to about

$10 billion in 2014. Of the last 20 years, only four of the years, the company came in with negative

net change in cash flow. The good cash flow generated from operations, investing and finance allows

the company to invest in long term capital and make big investments. The company is also strongly

committed in increasing dividend payout and share repurchases, consistently high levels.

Management: PepsiCo, Inc. currently has 30 executive officers on its core leadership management

team. Management team is led by the company’s Chairman & Chief Executive Officer, Indra K.

Nooyi.

Indra K. Nooyi has held the CEO position since 2006 and the role of Chairman since 2007.

Moreover, Nooyi has had extensive experience with the company. Since 1994, Nooyi has worked in

various functions including: Strategic planning, corporate strategy and development, finance,

business process optimization, information technology and investor relations. She understands and

knows the business.

Zein Abdalla, president of PepsiCo, assumed this role in 2012, and has been with the company since

1995. Abdalla, overlooks all of PepsiCo’s global category groups, operations and marketing services

and category strategies. His focus is to work with geographic business segments to create innovation

and build brand while significantly reducing cost within the process.

Hugh F. Johnston, executive vice president and Chief Financial Officer, assumed this role since

2010, and has been with the firm since 1987. Johnston is responsible for strategic financial

leadership, ensuring the company’s capital structure, financial systems and financial models are in

line with company’s strategy.

Industry Overview: Industry Characteristics: PepsiCo, Inc. operates in the Food and Beverages

industries. The global food and beverage retail industry has continued significant growth over the last

five years and is expected to continue, reaching approximately value of $5,776 billion dollars in 2017

with a compound annual growth rate of 5% over the next five years.

The global beverage market is divided between alcoholic and non-alcoholic.

Beverages Industry Key Trends: Beverage – The market is flooded with innovative products which

lead to the global beverage industry’s highly competitive nature. Customer loyalty is vital to the

industry’s growth and to attain this, companies constantly need to develop innovative high quality

products that satisfy customers taste.

PepsiCo only offers non-alcoholic products. Their beverages products are diversified including:

bottled water, juice, regular coffees, dairy drinks, energy drinks, sports drinks, soft drinks and others.

Soft Drinks Industry is separated into mature developed markets where growth is flat and developing

markets where growth still exists. Bottled water continues to show great strength in growth with

projected growth rate of 5.4% in volume terms this upcoming year. Energy drinks have also shown

great prospects with average growth in the past 5 years being 10% per year.

Key Industry Players: The Coca Cola Company, with its main strength in its Coke product and most

recognized brand name in the world and Dr. Pepper Snapple Group, prides itself in diverse portfolio

of CSD and non CSD products including brand names such as 7-Up and Snapple.

5. Cal Poly SMPP ANALYST REPORT ANALYST: HUBERT LO

Exhibit:8

Industry Leaders North America Market

Share

Beverages

Snacks

PEP Key Mergers & Acquisitions

2006 - IZZE Beverage Company ACQ

2007 - Naked Juice Company ACQ

2009 - Calbee Foods Strategic Alliance

2010 - Wimm-Bill-Dann ACQ

2011 - Tingyi Holding Strategic Alliance

2012 - Diamond Star Agreement

2013 - The Müller Group JV

ACQ = Acquisition

JV = Joint Venture

Innovative Products: Within the food and beverage industry, it is very important to constantly

produce new and trendy products that consumers like. Companies that are able to produce new and

innovative products that consumers like are able to build brand loyalty and are more likely to be

industry leaders. In 2013, PepsiCo was able to release four new products, Mountain Dew Kick Start,

Gatorade Frost Glacier Cherry, Starbucks Iced Coffee, and Lipton Pureleaf; each individually

achieved $100 million in sales. Currently, PepsiCo has been in efforts of releasing three types of

Pepsi-Cola products made with real sugar. The three offerings: “Pepsi Made with Real Sugar”, in its

original, vanilla and cherry flavors.

The Coca Cola company also released Diet Coke Frost, a new product as low calorie frozen

carbonated beverage, and also Coca Cola Life, coke that made with a blend of sugar and stevia, as

opposed to artificial sweeteners. Recently, the Coca Cola company released a new Sprite 6 Mix, a

limited flavor of cherry and orange taste. Companies need to constantly create innovative products to

appeal to the ever changing consumer taste.

Aggressive Advertisement/ Efficient Pricing: Marketing is an essential investment in growing and

sustaining the consumer market especially when introducing new products into the market. All major

industry players are at the forefront with marketing and advertising. PepsiCo with its heavy

investments in 2014 Super Bowl celebrations ads, and holding Ad campaign contests including

“Create to Celebrate” a Black history month art contest. Whereas, Coke has recently partnered as the

main drink provider with 2014 Winter Olympics and the upcoming 2014 FIFA World Cup this

summer. Companies in the beverage industry also are very diligent in their competitive pricing

strategy against their competitors, where all their products act on very small margin, therefore it is

essential for them to get the least cost of goods possible and selling it at the highest price they can in

comparison with their competitor.

Supply Chain Management: In the food and beverages industry, it is essential to have an effective

and efficient supply chain between company and third-party companies such as beverage bottlers.

Industry leaders are able to create supply chain networks that can help company generate great

productivity savings. PepsiCo is expected to generate $5 billion dollars in savings from 2015 to 2019.

While, Coke’s “2020 vision” plan is expected to save $1 billion through its supply chain in the next

two years. In more detail, for example, PepsiCo is plans to invest in 1 self-manufacture plant versus

the usage of eight to ten distribution centers lessens vehicle, fuel, transportation, and other overhead

costs that it takes in the process. Companies who have an integrated supply chain network definitely

have an upper hand within the industry.

Barriers to Entry: In the food and beverage industry, it is hard for new companies to create a well-

established brand name for themselves. For a company to be successful in this industry one must

have quality and innovative products that have consumers recognize. It is all about the brand loyalty.

For industry leaders like the Coca Cola Company, PepsiCo, and Dr.Pepper, they are all big well

established companies that have been in the industry for a long time and basically control this

industry. These industry players analyze consumers’ habits in great detail, and have dedicated

departments looking for the next big consumer trend in developing their next innovative product. For

a newly established company in this industry, it is hard; it must compete against the big industry

leaders for consumer attention.

Mergers & Acquisitions: M&A is key trend within the food and beverage industry, as big industry

leaders are constantly looking for innovation, and most often coming from smaller companies to

acquire. Some of the key PepsiCo, Inc. recent M&A and JV include: Izze Beverage Company (2006),

Naked Juice (2007), Wimm- Bill-Dann (2010), Tingyi Holding (2011), Diamond Star (2012), The

Müller Group (2013). These partnerships and acquisitions have enhanced PepsiCo’s product

portfolio as well as gain advantages such as international growth and efficient distribution channels.

6. PROS:

Dividend Aristocrat

Productivity Savings

Strength in Snacks Business

Strength in Emerging Market

CONS:

Slowing sales in CSDs

QUESTIONABLE:

PepsiCo Split Up

Exhibit 9: Annual Cash Dividends

Exhibit 10: Productivity Savings

Investment Summary: PepsiCo, Inc. is currently trading at a fair valuation compared to historical

averages. We issue a HOLD recommendation for PepsiCo because we have a target price of $87.57

and the share price currently is hovering around $ 85. And for a number reasons listed below,

PepsiCo is a good company to hold in any diversified portfolio as of right now.

Strong Commitment to Shareholder Value/Dividend Aristocrat: Company is a cash dividend

company that values its shareholders, as it looks to increase its dividends and share repurchases in

2014. The company has announced a 15% increase from 2013 annual dividend of $2.27 per share to

$2.62 per share. This marks the 42nd

consecutive annual increase in dividends per share. Moreover, it

will also increase its share repurchases program from 2013 of 3 Billion to 2014 of approximately 5

billion.

Commitment to Productivity Savings/Cost Cutting: Company is unleashing and extending their

$ 1 billion annual productivity savings target through 2019. PepsiCo seeks to improve productivity

by focusing on automation, shared services, restructuring manufacturing, and restricting global

transportation management system. (i.e., capital reduction, less usage of trucks and fleets, fuel &

inventory reduction.)

Strong Sales in Snacks Business: PepsiCo’s Frito Lay division continues to lead the company with

great growth. In the recent fourth quarter of 2013, PepsiCo’s snacks division volume grew 3% and

brought in $7.9 billion in revenue. And in third quarter of 2013, snacks division posted 7% organic

revenue growth including 5% revenue growth in the Frito – Lay division. The snacks business as

noted earlier generates 66% growth of PepsiCo overall. We believe that this will continue to be the

forefront driver in leading PepsiCo, as Frito Lay is one of the most well-known and recognizable

snack brands.

Strength in Emerging Markets/Diversification of Products: PepsiCo continues its strong

performance in emerging markets. The heavy investments in India, Asia, and Russia, are showing

promising results in these key markets. There is still a lot of room for PepsiCo to grow in these

countries, and being able to leverage themselves with their promising snacks brands in these

countries such as India and China will be key. Moreover, we believe that PepsiCo’s diversification in

their products selections with both snacks and beverages (i.e., juice & water brands) will help them

succeed in the emerging markets.

Slowing Sales in Carbonated Soft Drinks Industry: Key risk when looking at the PepsiCo, as the

consumption of CSDs continues to decline. Since 1998, the per capita consumption of CSD dropped

from 54 gallons to today’s figure of 44 gallons a year, and the consumption of CSDs is forecasted to

drop significantly in the next five years. With the continuation of increasing awareness of consumers

about negative health impact of CSDs and also regulations put forth on unhealthy snacks and soda,

we would expect to see the numbers and sales in CSD for PepsiCo to continue to decline in growth.

However, we should pay close attention to the new products that PepsiCo has stated that it will

release as natural sweeteners products, if consumers will react positively to these new products, we

may see flat to low single digit growth for PepsiCo in the CSD market again.

Active Investor wants Split Up: Throughout 2013 until now, Nelson Peltz, owner of $1.2B common

shares of PepsiCo has been on the forefront of pushing for separation of snacks and beverages into

two independent entities which he argues would create more shareholder value. On the other hand,

board of directors and mgmt. have argued the company to stay as “one”. We believe, if there was a

split-up, it would not happen anytime soon, at least not within the next one or two years. Nextly, we

believe that a split up will not be a good long term goal. A unified company with snacks and

beverages complement one another for the average consumer.

7. Cal Poly SMPP ANALYST REPORT ANALYST: HUBERT LO

CAPM Legend

= risk free rate (yield curve)

= beta of PepsiCo

( ) = risk premium

= epsilon of PepsiCo

PepsiCo, Inc. Target Prices

PCTL DCF RI

20% $68.87 $70.64

25% $71.09 $73.05

30% $73.20 $75.34

35% $75.47 $77.46

40% $77.77 $79.67

45% $79.90 $81.94

50% $82.10 $84.25

55% $84.75 $87.04

60% $87.57 $89.93

65% $90.32 $93.10

70% $93.60 $96.76

75% $97.78 $101.0

80% $103.0 $106.0

( )

Valuation:

Two detailed valuation models were constructed to value PepsiCo, Inc. and they are: Discounted

Cash Flow & Residual Income. Residual income model values the firm from today’s common equity

plus the Present Value of future Residual Income. Discount Cash Flow Model values the firm from

today’s common equity plus the Present Value of future Free Cash Flow.

Pro-Forma Financial Statement: Based on PepsiCo, Inc. for being an industry leader in the

consumers staples industry since 1965, the model assumes constant growth within range, which

means that we have omitted all outlier years or years with extreme high or low growth.

Sales Growth Forecast: The sales growth is the most important, and first line of financial statement

variables. We looked at the historical 20 years (1993 – 2012) sales revenue growth, and believe it

was adequate to use Min 0.3%, Avg 6.2%, and Max 9.6%.

Other Forecast Estimates: Forecasts of other financial statement items are based on their historical

value and relative relationship to sales growth. (i.e., cost of goods sold as percentage of sales

revenue). Moreover, for each financial statement item, Min, Avg, and Max are provided with

forecasted estimates.

Terminal Growth Forecast: The terminal sales growth is assuming top line sales to grow into

infinity; therefore, using a rather conservative estimate is a good decision. A small change in estimate

will have a big effect on our valuation. In the historical 20 years, company grew at 2% from 25

Billion to 65Billion in sales revenue. Given our current market conditions and saturated market in

both U.S. and emerging market with more competitors, we believe a range of 1 to 1.25% terminal

growth is reasonable.

Cost of Capital/ Discount Rate: Both models require an appropriate estimate of cost of equity to

effectively value PepsiCo, Inc. The capital asset pricing model (CAPM) as shown in the following

equation is main model to calculate discount rate for our model. Beta, risk premium, and epsilon are

all simulated values using triangular distribution based on CAPM input assumption estimates. The

only variable not simulated is our risk free rate. All cost of equity calculations and assumptions are

shown in (appendix IV).

Target Price: We arrived at our average target price of $82.10 and $84.75, with discounted cash

flow and residual income model respectively. We also believe that PepsiCo, Inc. price will likely fall

between 35 – 65 percentiles which is range of $75.47 - $ 90.32 for the 52 week range going forward.

The free cash flow to common equity and residual income calculations are shown in appendix 5 and

6).

(Valuation- Appendix 2-6)

8. Exhibit 11: PepsiCo, Inc. Gross Profit &

Sales Revenue(Net) Comparison

(1993- 2013)

Exhibit 12: PepsiCo, Inc. Sales & Cost of

Goods Financials (2008 – 2013)

Exhibit 13: Current Ratio & Quick Ratio

Comparison (1993 -2013)

Exhibit 14: Operating Cash & Market

Securities(1993- 2013)

Financial Analysis:

Increasing Profit PepsiCo, Inc. has proven its ability to increase its profit. PepsiCo is a profitable

company. And it is forecasted to continue its profitable trend going onward. Key findings including:

PepsiCo’s top line sales have increased from 43 billion in 2008 to 66 billion now which is a 53%

increase. Similarly, it has also grown its gross profit dramatically within the five years from 24

billion to 37 billion now which is a 55% increase. PepsiCo has proven to grow their sales through

careful management and knowing what consumers want. The company also focuses itself on

effective cost-cutting.

Key Financial Ratios: PepsiCo, Inc. key profitability ratios show that is a company profitable among

its peers in the industry. Return on equity 28.7%, net profit margin 10.14%, return on assets 8.86%,

return on investment (TTM) 14.70%.

Liquidity: A company’s financial ability to pay off short term and long term debt is a key

consideration in looking when valuing a company. PepsiCo, Inc. in terms of its liquidity and ability

to pay off debt is in its moderately fair range. Mainly, company is able to meet its short-term

obligations with good current ratio and quick ratios; however the downfall is that the company holds

too much long term debt.

Short Term Obligations: Since 2011, PepsiCo has improved its current ratio and quick ratios

substantially to current levels of 1.24 and 0.93 respectively. Both ratios look at the components of

current assets against the current liabilities. This shows that PepsiCo is improving its liquidity

position which is good, financially prepared in terms of market downturns.

Long Term Debt to Capital Structure: PepsiCo, Inc. has held a more leveraged position since 2006,

borrowing more long term debt for financing, and has increased their debt to equity ratio dramatically

from 0.16 to 1.40., which is now slightly above the industry average, but still fairly in sync within the

consumer staples sector.

Good Cash Flow: Holding a good amount of cash and having efficient cash flow is good for any

operating business. PepsiCo, Inc. is strong in holding vast amount of Operating Cash and Market

Securities, and has grown this asset account on the balance sheet to its current new high of 9.68

billion. Moreover, as mentioned earlier, the firm has a positive annual net change in cash.

Intangibles/Value: PepsiCo, Inc. is a big global food and beverage company with many different

patents and valuable reputational brands. Therefore, the intangible account is a big part of the firm’s

balance sheet. Since the year of 2010, there has been a huge jump in intangibles growth making its

current intangibles value to be at its company’s highest level. The intangibles value on the balance

sheet justifies that the company has a very well-known brand and is a company that creates value for

shareholders. Moreover, key acquisitions and partnerships including Wimm- Bill-Dann and Tingyi

Holding Company, in 2009 and 2010 is justifiable in creating the huge spike in intangible value.

Turnover Ratios: In order to understand how effective a company is in generating sales compared to

its input variables, different ratios such as net operating asset, working capital, PP&E turnover ratios

are used. PepsiCo, Inc. in recent trends have underperformed in all three of these ratios showing

slightly below company historic average levels, showing that company can improve on its efficiency

in terms of generating sales from its assets, working capital(current money available for immediate

usage), and long term plant property and equipment investments. The company management has

certainly made note of these low and decreasing ratio levels, as they have pin-pointed cost cutting

and making productivity more efficient to be a key business strategy going forward.

(Financial Analysis – Appendix 7)

9. Cal Poly SMPP ANALYST REPORT ANALYST: HUBERT LO

Key Investment Risks: All companies face various risks. In order to truly value PepsiCo accurately,

it is essential in understanding the various risks that the company faces. The following are key risk

factors that affect PepsiCo, Inc.

Macroeconomics Risks – Moderate - PepsiCo is a global company that operates in many different

countries, unfavorable economic conditions including: adverse changes in interest rates, volatile

foreign exchange markets, and commodity markets will have major financial effects on the company.

Interest Rates: PepsiCo uses various interest rate derivative instruments to hedge and manage their

interest expense and foreign exchange risk. Therefore, an increase in interest rate will have adverse

results in increasing company’s net interest expense. In 2014, interest rates are expected to rise, as the

economy grows and unemployment rates decrease. We believe that there is more upside in the

interest rates rising, which will cause borrowing to be more costly.

Foreign Exchange: PepsiCo operates on a global scale, as 49% of the company’s net revenue is

earned outside of the U.S. (Russia, Mexico, UK & Brazil accounts for 25%). This makes the

company susceptible to currency exchange risk. In early 2013, the devaluation of the Venezuelan

Bolivar had major negative effects on the 2013 first quarter financials. The devaluation of the

Venezuelan Bolivar from 4.3 VEF/USD to 6.3 VEF/USD had depreciation effects of $111 million

dollars. However, we believe that PepsiCo is prepared, as other currencies that the company operates

in will offset the depreciation effects, moreover company also uses foreign currency derivatives to

hedge against currency risk.

Commodity Prices: PepsiCo utilizes vast amount of raw materials and goods including: sugar cane,

corn, wheat, rice, oats, potatoes, and various fruits to produce their products, making them

susceptible to changes in commodity prices. We expect commodity prices to inflate in 2014 due to

the economy growing again; prices of commodity are going to rise. PepsiCo is prepared for the

commodity price inflation. The company uses hedging strategies such as derivatives with short term

contracts of less than 3 years to economically hedge price fluctuations related to metals, energy, and

agricultural products. We also expect the company to increase prices of products to offset this

commodity price inflation.

Market Risks – Moderate

Changing Consumer Taste/Health Awareness: One of the increasing trends within the soft drinks

industry is the changing preference of consumers. As obesity and health issue continues to be a

concern globally given USA and Mexico are the two top countries with obesity problems, they are

also two key markets to PepsiCo. Recent quarter sales have shown the decline in CSD volume

continues, and it is affecting all the major companies in the industry including Dr. Pepper & Coca

Cola. PepsiCo has been on the forefront of this problem, by diversifying its portfolio of products and

innovation of new products with stevia and aspartame replacing sugar.

Regulations/ Mexico Taxes: Regulations will continue to play a key risk in the snacks and soft

drinks industry. Regulations in the recent years have increased in its efforts in trying to limit

consumption of sweetened drinks and snacks. In October 2013, Mexico regulators passed a tax

excising 1 MXN per liter on sugary drinks and 5% tax on snack foods. We believe that it will have

negative effects on Latin America sales volume, but the growth potential in this region is so high, it

will offset the cons of the taxes. Going onward, we will see more progression in regulations;

however, we believe that the company has diversified itself well enough, outside of sugary drinks and

unhealthy snacks that it has hedged against this risk fairly well.

10. Current Analyst Research Notes and other Company News:

May 6, 2014: PepsiCo Inc. declares a 15 percent increase in annual dividend, from an annual rate of

$2.27 to $2.62 per share on common stock. Payable on June 30 to shareholders of record as of June 6.

May 5, 2014: PepsiCo, Inc. and The Coca Cola Company have announced to remove controversial

ingredient called brominated vegetable oil from their drinks. As ongoing petitions and advocacy has

pressured both companies to do so. The BVO ingredient is currently used in Mountain Dew, Amp

energy, and Gatorade products.

April 8, 2014: PepsiCo, Inc. plans to release three types of Pepsi-Cola sweetened with real sugar and

not with high fructose corn syrup. They will be marketed as “Pepsi Made with Real Sugar”, coming

in three flavors: original, vanilla, and wild cherry.

April 7, 2014: Cheetos and Doritos, two of PepsiCo’s Frito- Lay division are releasing a new snack

mix called “Cheetos Flamin’ Hot/Doritos Dinamita Chile Limon Mix” which is a one of a kind snack

mix combining Cheeto’s Flamin Hot snacks with Doritos Dinamita Chile Limon snacks.

April 4, 2014: PepsiCo, Inc. reported 2014 first quarter earnings with $12.6 billion in first quarter,

ahead of analysts’ estimates of $12.4 billion. Net income was up 13% to $1.22 billion and earnings

per share came in at 79 cents; 10 cents per share higher than a year earlier. Still maintaining its

forecast for the year and expects organic revenue to rise by mid-single digit percentage this year.

April 2, 2014: PepsiCo, Inc. and Major League Baseball Properties agree on a multi-year extension of

their sponsorship agreement, building on the over 15 year partnership.

February 27, 2014: Shanghai Disney Resort announced a multi-year strategic alliance with PepsiCo,

Inc. and Tingyi Holding Corp., which recognizes PepsiCo and Tingyi Holding as the primary

beverage suppliers to the resort.

February 13, 2014: PepsiCo, Inc. reported 2013 fourth quarter earnings with $20.12 billion and $66.4

billion for the 2013 full year. The company also posted $1.05 per share, $0.04 ahead of analysts’

expectations. Strong performance from Frito Lay North America of 4% organic revenue growth, and

developing and emerging markets also showed strength with 10% organic revenue growth.

Disclosure Notice:

I, Hubert Lo, hereby certify that the analysis provided in this assignment reflects my

personal opinion about PepsiCo, Inc. Neither my compensation, nor my academic

performance will be directly or indirectly enhanced by the opinions outlined above.

11. Cal Poly SMPP ANALYST REPORT ANALYST: HUBERT LO

APPENDIX SECTIONS

-Valuation-

Appendix 2: Sales Growth Forecast Assumption: The sales growth is the most important, and first line of the

financial statement variables, because it has a trickle-down effect on every financial statement item. Therefore, it is

essential and look at this item in detail. I created graph of sales growth for the past twenty years (1993 – 2012), the outlier

years of high sales growth and low sales growth were omitted, (1994, 1997, 1999, 2002, 2010, 2011, 2012). The min,

average, and max were used for sales growth forecast estimates after omitting outliers. Min 0.3%, average 6.2%, maximum

9.6%.

Appendix 3:

The following is the Pro-forma Assumptions used in DCF and Residual Income Valuation:

Minimum Average Maximum

Income Statement

Assumptions

Sales Growth 0.3% 6.2% 9.6%

Cost of Goods/ Sales 40.0% 41.2% 42.2%

R&D/ Sales 0.5% 0.8% 1.0%

SG&A/ Sales 35.2% 37.2% 39.4%

Dep & Amort/ Avge

PP&E and Intang.

7.5% 8.2% 8.8%

Net Interest Expense/

Avge Net Debt

5.0% 6.8% 7.9%

Non-Operating

Income/Sales

0.1% 0.6% 1.3%

Effective Tax Rate 23.0% 26.0% 30.5%

Minority Interest/After

Tax Income

0.3% 0.5% 0.6%

Other Income/Sales 0.0% 0.0% 3.1%

Ext. Items & Disc. Ops.

Sales

0.0% 0.0% 0.0%

Pref. Dividends/ Avge.

Pref. Stock

0.0% 0.0% 0.0%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

1 3 5 7 9 11 13 15 17 19

Sales Growth(1993 - 2012)

Sales Growth

12. Minimum Average Maximum

Balance Sheet

Assumptions

Working Capital

Assumptions

Ending Operating

Cash/Sales

5.2% 7.4% 9.6%

Ending

Receivables/Sales

10.1% 10.4% 11.1%

Ending Inventories/Sales 10.0% 12.5% 13.7%

Ending Other Current

Assets/Sales

1.9% 2.4% 2.8%

Ending Account

Payable/Cost of Goods

Sold

13.0% 16.0% 20.4%

Ending Taxes

Payable/Sales

0.5% 1.1% 2.0%

Ending Other Current

Liabilities/Sales

9.7% 11.4% 13.0%

Other Operating Asset

Assumptions

Ending Net PP&E/ Sales 26.7% 27.8% 29.6%

Ending

Investments/Sales

9.2% 10.0% 10.9%

Ending Intangibles/Sales 20.8% 22.2% 24.5%

Ending Other Assets/

Sales

1.5% 3.3% 4.1%

Other Operating Liability

Assumptions

Other liabilities/Sales 10.4% 12.0% 14.0%

Deferred Taxes/Sales 4.2% 5.6% 6.7%

Financing Assumptions

Current Debt/Total

Assets

1.5% 1.8% 2.0%

Long Term Debt/Total

Assets

15.8% 18.6% 23.6%

Minority Interest/Total

Assets

0.0% 0.0% 0.1%

Preferred Stock/ Total

Assets

0.0% 0.0% 0.1%

Dividend Payout Ratio 34.0% 36.5% 40.0%

13. Cal Poly SMPP ANALYST REPORT ANALYST: HUBERT LO

Appendix 4: Cost of Capital Estimation

CAPM Model: ( )

Beta ( : The Beta of PepsiCo, Inc. was calculated by finding the stock price of S&P 500 and stock price of PepsiCo,

Inc. for the last 20 years into monthly data from (January 1993 to December 2012). Secondly, we then utilize the natural

logarithm of the prices to find our returns in monthly data. Thirdly, we use linear regression with X variable as S&P 500

monthly returns and Y variable as PepsiCo, Inc. monthly returns and analysis shows us a beta being 0.67 and standard error

of 0.07. The following output is regression analysis of S&P 500 and PepsiCo, Inc. monthly returns:

Below are the Beta assumptions inputs into the CAPM model in calculating the discount rate:

Beta Assumptions Minimal Average High

0.59 0.67 0.74

Standard Error 0.0741

We simulated the three betas, (min, average, and max), with the triangular distribution, as an input into our capital asset

pricing model.

Epsilon( : The epsilon term is the residual values component within the regression output, and is component of the

Capital Asset Pricing Model that measures the firm’s specific idiosyncratic risk which is also same as the error term in the

regression model. We ran a regression model of S&P 500 returns and PepsiCo returns as in the output shown above and

calculated the residual values, and for monthly data and sum up the residuals into annual residuals, and omitted outliers and

similarly calculated the average epsilon and standard error of epsilon to compute low and high epsilon. Based on this

regression model, the epsilon term has little to medium effect on the capital asset pricing model, because the standard error

deviation is high. Similarly, we inserted these assumptions following a triangular distribution into our model.

Below are the Epsilon assumptions inputs into the CAPM model in calculating the discount rate:

Epsilon Assumptions Minimal Average High

-3.14% -0.003682% 2.41%

Standard Error 2.773%

14. APPENDIX 4 CONT:

Risk Free Rate of Return ( : The risk free rate is theoretical rate of return of an investment with zero risk. We based the

risk free rate return using the yield curve from today’s rate (year 1 to year 12) and using 30 year yield rate for our terminal

value. We utilized the current yield rates and inputted into our capital asset pricing model. The following is a yield curve

as of 3/7/2014.

Below are the risk free rate of return assumptions inputs into the CAPM model in calculating the discount rate:

Risk

Free

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2043

0.13% 0.38% 0.79% 1.22% 1.65% 1.96% 2.27% 2.48% 2.64% 2.80% 3.72%

Risk Premium( : The risk premium is the expected return in excess of the risk free rate of return, I gathered the

historical 20 year monthly data from January 1993 to December 2013 of S&P 500 Price Close, and Libor Rates close. Then

calculated the returns for both S&P 500 and Libor Rates using natural logarithm and compounding methods respectively,

and calculated the difference to obtain the risk premium monthly rates. Next, we sum up the monthly risk premium rates

into annual basis, and created a graph of the risk premium over the last 20 years. Then we omitted the outlier years and

found the minimum, average, and maximum risk premium values with the plus or minus standard deviation as our input

assumptions for the triangular distribution that we inserted into our capital asset pricing model. We thought this was

adequate risk premium range, because our model is a conservative long run model that is stable, on average risk premium

of the past has deviated roughly between 5-7%, and setting our maximum and minimum with the plus or minus calculated

3.55% is reasonable.

Below are the risk premium assumptions inputs into the CAPM model in calculating the discount rate:

Risk Premium Minimum Average Maximum Standard

Deviation

2.45% 6.00% 9.55% 3.55%

Exhibit: Yield Curve as of 3/7/2014

15. Cal Poly SMPP ANALYST REPORT ANALYST: HUBERT LO

APPENDIX 4 CONT.

Cost of Equity Assumptions:

Below are the all assumptions used inputs into the CAPM model in calculating the discount rate:

Other Assumptions Minimal Average High

Beta 0.59 0.67 0.74

Risk Premium 2.45% 6.00% 9.55%

Epsilon -3.14% -0.003682% 2.41%

Risk Free Rate Range

0.13% 3.72%

Each of the inputs, BETA, Risk Premium, Risk Free Rate are all simulated with triangular distribution to utilize random

error and ultimately the average cost of capital (output) is calculated as randomly generated number between the range of

3.82% and 6.47%. (2013 – 2022)

Average Cost of Common Equity using Monte Carlo Simulation (10,000 Simulations):

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Average

Cost of

Common

Equity

3.82% 4.06% 4.45% 4.49% 5.31% 5.63% 5.94% 6.14% 6.32% 6.47%

16. APPENDIX 5: Discounted Cash Flow (DCF) Valuation

To effectively value the current price of Pepsi, Co Inc., we utilized both the discounted cash flow model (DCF) and Monte

Carlo Simulation in E-Val. Discount Cash Flow (DCF) model values the firm from today’s common equity plus the present

value of future free cash flow. Monte Carlo Simulation was also used to incorporate simulation for random errors, allowing

for all items of our pro-forma financials to be all random, in consistence with our historical 20 year values. (1993 to 2012).

Free Cash Flow to Common Equity

Based on simulated cost of equity and terminal sales growth, the eVal model analyzes the forecasted cash flow. The

following is a table showing simulation average estimated cash flow of estimated free cash flow to equity for next 10 years

(2013 to 2022).

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

$6.88 m $7.39m $7.77m $8.23m $8.62m $9.16m $9.60m $10.1m $10.63m $11.26m

Average Present Value of Free Cash Flow:

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

$6.63 m $6.81 m $6.85m $6.81m $6.65m $6.59m $6.44m $6.33m $6.18m $6.10m

The free cash flows are then discounted and used in calculating PepsiCo, Inc’s price per share. Taking into account of a

simulated cost of capital, and simulated terminal growth rate, we discount the present value beyond 10 years and also the

present value of the first 10 years, ultimately coming up with a value attributable to common equity in today’s time. This

value is then divided by 1.54 million shares outstanding to come up with a forecast price per share. We then run 10,000

trials using the Monte Carlo simulation on the forecast price per share, and the 50th

percentile price or fair price value that

we come up with is $82.24.The following are exhibits on the 20th percentile to 80th percentile forecasted target prices and

also the normal distribution showing the same data.

17. Cal Poly SMPP ANALYST REPORT ANALYST: HUBERT LO

APPENDIX 5 CONT:

Valuation (Discounted Cash Flow) Method:

We came up with our target price by firstly forecasting the top sales line data and other financial statement accounts. Then

analyzed the last 20 years data (1993 – 2012) and omitted the outliers, and pin pointed the minimum, average, and

maximum assumptions as mentioned previously.

After defining the assumptions in the income statement, balance sheet -working capital, operating capital, operating asset,

operating liability and financing. We utilized the triangular distribution function to create randomize values following a

triangular shape function within our value assumptions. Next, we ran 10,000 Monte Carlo simulations for the price per

share calculated by discounted cash flow.

Overall, we believe with our discounted cash flow valuation model that current price of PepsiCo, Inc., $82.15 is trading

near its fair value price of $82.10. We have set a price target of $87.57 looking at the value price 60th percentile. We also

believe that the range that PepsiCo, Inc. price will likely fall between 35 and 65 percentile which is range of $75.47 to

$90.32 for the 52 week range going onward.

Percentiles DCF

Target

Price

20% $68.87

25% $71.09

30% $73.20

35% $75.47

40% $77.77

45% $79.90

50% $82.10

55% $84.75

60% $87.57

65% $90.32

70% $93.60

75% $97.78

80% $103.04

18. APPENDIX 6: Residual Income Valuation

The residual income valuation model is used to find the earnings for a period in excess of investor’s required return on the

beginning of period investment (common equity). We use the residual income model to see the amount of income generated

by the company taking already into account for the cost of equity capital. Based on simulated cost of equity and terminal

growth rate, the following simulated average residual income:

Residual Income

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

6.40m 7.69m 8.01m 8.32m 8.66m 9.03m 9.43m 9.86m 10.36m 10.86m

The residual income values are then discounted to present time, firstly discounting the present value of the first 10 years

(2013 – 2022) and the present value of beyond 10 years. Then, the present value of first 10 years discounted, present value

of beyond 10 years discounted, and common equity as of December 31, 2012, the three are added to sum up the value

attributable to common equity and divided by 1.54 million common shares outstanding to come up with the forecast price

per share using the residual income valuation model. Then we simulated using the Monte Carlo simulation for the

forecasted price per share by 10,000 trials, and the 50th

percentile price we came up with is $84.25 per share. The following

is the normal distribution and percentiles of Residual income target price for PepsiCo Inc.

Percentiles RI Target

Price

20% $70.64

25% $73.05

30% $75.34

35% $77.46

40% $79.67

45% $81.94

50% $84.25

55% $87.04

60% $89.93

65% $93.10

70% $96.76

75% $101.03

80% $106.04

19. Cal Poly SMPP ANALYST REPORT ANALYST: HUBERT LO

APPENDIX 7: Financial Statement Analysis

Profitability

Liquidity Ratios

21. Cal Poly SMPP ANALYST REPORT ANALYST: HUBERT LO

Exhibits Appendix

Exhibit 3: Three Different Brand Images: Fun- for- you, good- for- you, better-for-you.

Exhibit 1: Sales Revenue in Products and Geographies

Exhibit 2: Sales Revenue & Growth % Breakdown

22. Exhibit 4: PepsiCo Products Globally

Exhibit 5: Net Change in Cash Graph

Exhibit 6: Dividend Payout Ratio Graph

Exhibit 7: Common Shares Outstanding

23. Cal Poly SMPP ANALYST REPORT ANALYST: HUBERT LO

Exhibit 8: Industry Leaders North America Market Share

Data Source: 2013 Company Annual Report

24%

21%

9%

8%4%

4%

5%

25%

U.S. Liquid Refreshment Beverage Category

Share % Retail Sales in Measured Channels

PepsiCo, Inc.

Coca Cola

Dr. Pepper Snapple Group, Inc.

Private Label.

Monster

Red Bull

Nestle

Other

37%

10%

4%

7%

3%

3%

6%

30%

U.S. Savory Snacks % Retail Sales in

Measured Channel

PepsiCo

Private Label

Kraft

Kellogg’s

Conagra

Synder’s Lance

Mondelez

Other

PepsiCo, Inc. 24.3%

Coca Cola 21.1%

Dr. Pepper

Snapple

Group, Inc.

8.9%

Private Label. 8%

Monster 4%

Red Bull 4.2%

Nestle 5.2%

Other 24.4%

PepsiCo 36.6%

Private Label 10.0%

Kraft 3.6%

Kellogg’s 6.9%

Conagra 3.3%

Synder’s Lance 3.5%

Mondelez 5.6%

Other 30.4%

24. Mergers & Acquisitions Timeline

2006 - IZZE Beverage Company ACQ

PepsiCo acquires Izze Beverage Company, an all-natural sparkling juices company.

2007 - Naked Juice Company ACQ

PepsiCo acquires Naked Juice Co., a line of healthful, preservative free juice drinks company.

2009 - Calbee Foods Strategic Alliance

PepsiCo and Calbee Foods Company announce a strategic alliance to make and sell a wide range of

food products in Japan.

2010 - Wimm-Bill-Dann ACQ

PepsiCo acquires Wimm-Bill-Dann, Russia’s leading branded food and Beverage Company.

2011 - Tingyi Holding Strategic Alliance

PepsiCo and Tingyi Holding, one of the major food and beverages companies in China, announce an

agreement to form a strategic alliance in China.

2012 - Diamond Star Agreement

PepsiCo announces an agreement with Diamond Star, one of the largest consumer packaged goods

distributors in Myanmar, to import, sell and distribute Pepsi-Cola, 7-Up and Mirinda.

2013 - The Müller Group JV

Müller Quaker Dairy, a joint venture between PepsiCo and The Müller Group open a new yogurt

manufacturing facility in New York.

25. Cal Poly SMPP ANALYST REPORT ANALYST: HUBERT LO

Exhibit 9: Annual Cash Dividends

Exhibit 10: Productivity Savings

Source: company annual report

Exhibit 11: PepsiCo, Inc. Gross Profit & Sales Revenue (Net) Comparison (1993- 2013)

26. Exhibit 12: PepsiCo, Inc. Sales & Cost of Goods Financials (2008 – 2013)

Exhibit 13: Current Ratio & Quick Ratio Comparison (1993 -2013)

$43.25 $43.23

$57.84

$66.50 $65.49 $66.42

$18.84 $18.60

$24.06

$29.07 $28.80 $28.77

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13

Last 5 years Sales Revenue & COGS

Comparison - billions

Sales Revenue Cost of Goods Sold