Supporting ‘Green’ electricity: Lessons learned from the Spanish Feed‐in tariff system

Paper read at 4th Atlantic Workshop on Energy and Environmental Economics (A Toxa, Spain), 07-2010. Lara Pérez Dueñas, GNERA Energía y Tecnología. Lecciones aprendidas del sistema español de apoyo a las renovables basado en un sistema de primas y tarifas. *** The Spanish economic support system for electricity from renewable energy sources has had a good reputation due to its good results in terms of number of new plants, installed megawatts, industrial development, etc. Nevertheless, in the last years we have assisted to major and sudden legislative changes motivated by different events that have put under discussion the system sustainability. After describing the main green electricity support systems available and the benefits of introducing renewable energies in the electricity market, this paper analyses the causes of the “boom and burst” of the Spanish support mechanisms and the main lessons learned.

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (20)

Similaire à Supporting ‘Green’ electricity: Lessons learned from the Spanish Feed‐in tariff system

Similaire à Supporting ‘Green’ electricity: Lessons learned from the Spanish Feed‐in tariff system (20)

Dernier

Dernier (20)

Supporting ‘Green’ electricity: Lessons learned from the Spanish Feed‐in tariff system

- 1. Supporting ‘Green’ electricity: Lessons learned from the Spanish Feed‐in tariff system Lara Pérez Dueñas Gnera Energía y Tecnología. Energy Consultant and Energy & Environment Engineer lpd@gnera.es ABSTRACT The Spanish economic support system for electricity from renewable energy sources has had a good reputation due to its good results in terms of number of new plants, installed megawatts, industrial development, etc. Nevertheless, in the last years we have assisted to major and sudden legislative changes motivated by different events that have put under discussion the system sustainability. After describing the main green electricity support systems available and the benefits of introducing renewable energies in the electricity market, this paper analyses the causes of the “boom and burst” of the Spanish support mechanisms and the main lessons learned. JEL code: Q4 Key‐words: electricity market, renewable energy, feed‐in tariff, renewable energy support instruments I. GREEN ELECTRICITY SUPPORT INSTRUMENTS Costs and benefits of renewables in the electricity market A sustained development of renewable energy (RE) is nowadays still not possible without the support of dedicated policy instruments. Much debate has been made to argue if renewable energies are ‘too expensive’ or not, leading to even emotional debates. Actually, the use of electricity from renewable energy sources has several direct and indirect effects on energy costs, as well on economics and social issues. Their quantification can allow us to have a more global vision of the incentives paid to renewable electricity producers. Let us briefly describe some of these positive and negative effects: - Environmental externalities: Actual energy costs do not include environmental externalities: health issues, energy dependency, energy resources depletion, supply and public security, accidents, climate change, global justice… - Economic and social benefits: Deloitte (2009) in its study on the macroeconomic impact of wind energy, compares the direct cost of incentives for wind power in Spain to other quantified benefits such as CO2 emissions, fewer fossil fuels import and other indirect economic and social benefits such as new job creation, direct and indirect increase in PIB, R&D… Morthorst (2010) also states that “if both the direct and indirect cost savings from renewable energy generation were taken into consideration, the net effect of the RES

- 2. support scheme would be negative, that is, the consumer would pay lower prices.” - Merit order effect: The introduction of renewable energy in an electricity market where price setting is based on merit order can result in lower electricity spot prices for consumers and eventually (but not necessarily) in lower retail prices, as will be further discussed. - Opportunity cost due to additional operating reserve: Most renewable energies are said to be “not administrable”, i.e. we cannot regulate their production on demand as it depends mainly on weather conditions (wind, sunlightning or rain) or on the lack of flexibility of the plant –which is also the case for nuclear power. Thus, we need to grant an additional operating reserve that will ensure the electricity supply on peak hours. Combined cycles are a valuable technology for operating reserve because of its high flexibility. Spain has bet on this technology and has greatly increased the installed capacity of combined cycles in few years. These plants, with a high marginal cost, are used increasingly as operational reserve due to the development of non administrable energies, causing them to be shut down most of the time, thus reducing its efficiency and its profitability. ‘Green electricity’ support instruments The theoretical start point of renewable energy economic support in the electricity market context is the existence of externalities for environmental, security and health associated costs in conventional energy plants (Finon et al, 2004). Putting it into other terms, the goal is to ensure the development of the technologies until grid parity is reached. Grid parity is defined as the point where renewable electricity is equal or cheaper than the reference cost for grid power. This point could be achieved by 2016 for Spanish PV, and will differ for different technologies and countries. Nevertheless the achievement of grid parity does not have to mean the removal of incentive regimes (KPMG, 2009). To overcome this “market failure”, the first idea that comes into mind is to introduce a direct pollution tax to make producers pay for actual environmental costs, for example a CO2 emissions tax. Other instruments have been developed that differ from a genuine “green tax”, but which pursue the same objective, in environmental and economical terms, such as: - voluntary market based on a certification for renewables, which consumers will buy with an extra cost (“origin guaranties”) - granted costs for every renewable kWh - tendering systems - quota exchange systems

- 3. In Europe, Member States are required by different Directives to support electricity from renewable energy sources. Countries are given freedom to choose their preferred support scheme. Given different national priorities and segmentation in electricity market (despite the market opening since early 2000’s), the support schemes differ in each country and we can state that the 27 Member States operate 27 different support schemes. No harmonisation is foreseen at the short‐middle term, and a coordinated approach is preferred (European Commission, 2008). Implemented policy tools in Europe and worldwide can be divided into two main categories: price‐based instruments and quantity‐based instruments. Price‐based instruments (as Feed‐in Tariffs or Premiums, as developed in Germany, France or Spain) will fix a price for electricity, and the quantity will be determined by industry development and market evolution. Quantity‐based instruments, on the contrary, will fix an established volume of energy or power for the country, communities or companies, and the price will be set by the competition between operators. Examples for quantity‐based instruments are green certificates (UK, Belgium, Italy, Sweden) or tendering systems (Ireland, France). FIT and premiums In a Feed‐in Tariffs (FIT) scheme, producers are granted an amount of money for every kWh generated. This can be a fixed tariff or a premium paid on top of the electricity market price. The utility is obliged to purchase all electricity generated, or to give it preference, with the generator obliged to sell all electricity generated to the utility. The tariff or premium is granted for a long period of time, typically 15‐20 years. This provides a long term degree of certainty, thus lowering the market risk. Rates can be differentiated based on RE source, technology type, capacity size, the date the system becomes operational, or location of the project. Tariff adjustments can be made in the future, based on inflation or on installed capacity or generation costs (Burgie, 2009). Quota Obligations Under a quota obligation, governments impose an obligation on consumers, suppliers or producers to source a certain percentage of their electricity from renewable energy. This obligation is usually facilitated by tradable green certificates. Accordingly, renewable electricity producers sell the electricity at the market price, but can also sell green certificates, which prove the renewable source of the electricity. Suppliers prove that they reach their obligation by buying these green certificates, or they pay a penalty to the government (European Commission, 2008). Theoretically, this system could have great advantages that have led to a keen interest for green certificates in the last years: it is in the line of electricity market and is financed directly and equally by the operators. Nevertheless, it results on high transaction costs and high risk associated costs, which have been poorly taken into account in the past. Moreover, quota obligations benefits the lower cost technologies, already mature, but doesn’t support emerging technologies with a great potential.

- 4. Tendering In a tendering system, the Government sets an objective for the energy mix and tries to reach it trough a succession of tenders. As a result, the producer will get a long term contract at the price set in its bid, with a buying obligation for Utilities. The proposals are ranked from low to high until the auction is reached. Theoretically, tendering would allow a better control of quantities that have to be paid to renewables, would limit global costs as they support in the first place the lower costs technologies and would stimulate innovation. In practice, nevertheless, the experiences have not been so positive. Other systems Other instruments, such as voluntary agreements, CO2 taxes, investment incentives or Fiscal incentives (tax exemptions or reductions), obligations on fuel suppliers, public procurement policy, research and development... are mainly used as a complement, in addition to the main support scheme. Comparison between support instruments The European Commission (2008) has measured the success of a policy with its effectiveness in increasing renewable electricity generation and by the level of payment received by generators in comparison to the level they require for profitability. As a general rule, the criteria for evaluating the support system quality can be summed up as: 1‐a reasonable cost for community, 2‐system stability, 3‐avoiding administrative barriers and 4‐ensuring grid access. As we will further discuss, although the Spanish system was well rated in the 2008 European Commission's study, in practise some of these criteria have not been met, resulting in most of the problems attributed to Spanish FIT. Today, FIT is the most prevalent renewable energy policy in the world. In Europe, with the recent shift of the United Kingdom towards a combination of ROC (renewable obligation certificates) and FIT, 70% of member states have implemented a feed‐in tariffs policy. Worldwide, forty‐five countries had adopted this kind of system in 2008 and even in North America, traditionally reluctant to tariff systems, FIT policies have been implemented in some US states and in a Canadian province (Ontario) and are being carefully considered in a number of other US states (Burgie, 2009). The European Commission has been very favourable in the past to green certificates instruments, but has evolved in its lasts reports: “Comparing the two main types of support schemes, namely quota obligations and feed‐in tariffs, historic observations from EU Member States suggest that feed‐in tariffs achieve greater renewable energy penetration, and do so at lower costs for consumers.” (European Commission, 2008)

- 5. Tendering was in place in the UK at the time where Germany and Denmark started their wind development through a feed‐in tariffs system. The comparison between wind industry developments in all three countries is clearly in favour of FIT (Finon et al, 2004). Nowadays, it is generally considered that tendering is not a well adapted instrument to build a renewable energy support policy except as a complement for other instruments (Hadjsaïd, 2009). In Denmark, for instance, tendering is used as a stimulus for the development of a particular technology –off‐shore wind. II. THE SPANISH FEED‐IN TARIFFS SYSTEM Spain has bet on Feed‐In tariffs since early 90's, following Germany and becoming a world pioneer and leader in this kind of policy. The basis for the current FIT system was established in 1994 for small capacity facilities, obliging utilities to buy the renewable electricity surplus at a price that depended on retail price. With the opening of the market, developed with Royal Decree (RD) 2818/1998, the producers could sell their energy directly in the market or at a fixed tariff. Later, RD 436/2004 introduced the obligation of forecasting when penalizing deviations between energy prediction and real production, and gave the possibility of choosing between a fixed tariff or the market price plus a fixed premium. RD 661/2007 separates finally the support from the reference electricity price (the tariff or premium is not a % of the electricity price any more). It also introduces a cap and floor for some technologies to avoid a too high or too low retribution due to possible strong fluctuations of spot market price. In 2008, RD 1578/2008 introduced a quota and registry for solar plants, which was also applied for the rest of the technologies included in the “Special Regime” (i.e.: all renewables and CHP plants with less than 50MW) in 2009. In 2010 a new Royal Decree is expected to come. Next, will be described the most relevant differentiating characteristics of Spanish FIT and its evolution. • Electricity market agents Since the liberalisation of the market, the different agents have to be juridically separated to avoid vertical integration. The following agents participate in the generation market: - Producer - Independent System Operator (REE): is in charge of the technical management of the system and of the security of supply - Independent Market Operator (OMEL) - Independent regulatory body (CNE): regulates the system and centralises all the information - Utilities: own the lines and distribute the electricity - Representative agent: acts as the speaker between producers and other agents. It is interesting to note that the representative agent is given the possibility to have a so‐called “portfolio effect”, i.e. to send predictions of many plants in the same

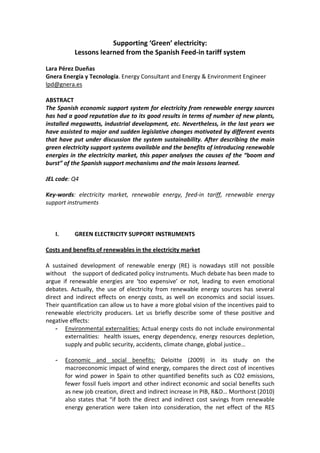

- 6. programme unit (like a virtual plant), thus consolidating its deviations. This leads to an easier management of supply for the System Operator, as well as reduced deviations costs for generators. • Choosing between tariff or market A big particularity of Spanish FIT system is that producers can opt for either getting a fixed tariff per kWh produced or being paid a premium on top of market price. Premium FITs have the advantage of introducing competition between producers in the electricity market and helping to give an incentive to renewable electricity production during peak periods. To avoid excessive costs when prices rise or too low income for producers when prices sink, Spain has introduced in 2007 a cap and floor system which “restrains” the final price. Today, cap and floor exists for wind power, small hydropower, biomass and biogas, whereas photovoltaic can opt only for a fixed tariff. Caso de Tarifa Regulada b.7.1 Caso de la opción Mercado + Prima Precio Horario Electricidad (€/MWh) 140 90 80 120 70 100 60 Prima opción Mercado (€/MWh) 50 Prima Equivalente 80 Precio horario Mercado (€/MWh) Precio horario Mercado (€/MWh) 40 Techo 60 30 Suelo 20 40 10 20 0 H1 H2 H3 H4 H5 H6 H7 H8 H9 H10 H11 H12 H13 H14 H15 H16 H17 H18 H19 H20 H21 H22 H23 H24 0 Horas H1 H2 H3 H4 H5 H6 H7 H8 H9 H10 H11 H12 H13 H14 H15 H16 H17 H18 H19 H20 H21 H22 H23 H24 Figure 1: Illustration of the two market options: fixed tariff and premium on top of spot price with cap and floor. For tariff option, the (variable) difference between tariff and spot price is called “equivalent premium” • Forecasts Few countries require RE generators to forecast their output and to provide this information to grid operators (Spain, Slovenia, Estonia): since November, 2009, Spanish generators over 450kW are required to forecast their generation 24 hours in advance, or through the intraday market (until that date, forecasting was requested only for plants bigger than 1MW). However, only Spain charges generators if their actual electricity output deviates from their predictions. A deviation may incur in a penalty if this deviation goes against the regulating system. That means that if a generator has produced more energy than forecasted, and that the global system has less energy than predicted, then the deviations of this particular generator will have no cost, and vice‐versa. • Daily markets To allow better adjustments of forecasting and actual production, and to sharpen the System Operator regulation, several markets have been established: The day‐ahead market (spot market) is a physical market in which prices and amounts are based on supply and demand. It takes place in one daily session and fixes the trading for the 24 hours of the next day.

- 7. The intraday market has been established in order to introduce adjustments to the day‐ahead market. This way, the operators can adjust the forecasts to the real production, resulting in a better regulation of power market and reducing the deviations. It is developed in six different intraday sessions, and the new bids or adjustments to the spot market can be introduced three to four hours before the next session. In addition to these, technical restrictions and deviations from predictions are regulated through a regulating power market and a balancing market, with different prices. • Differentiated support levels Tariff levels have been set to get a rate of return of 7% after tax (Kema, 2009). Both the tariff and premium option are differentiated by technology and by size ‐through capacity thresholds‐ to take into account economies of scale in larger plants. Capacity thresholds, however, instead of linear capacity progression can lead RE developers to size to the limit of the highest rate, focusing on capacity rather than actual output (Burgie, 2009). Note that Spain was the first country to introduce a FIT for solar thermal technology. Whenever the fixed tariff option has been chosen, generators can receive differentiated FITs for peak or off‐peak hours. CHP (incl. biomass CHP) in peak hours will receive a bonus of +37% of the tariff and a penalisation of ‐36% in off‐peak (small hydro and biomass can have a more limited bonus and penalisation). Moreover, to discourage speculative queuing grid access deposits are required: 500€/kW for photovoltaic and 20€/kW for the rest of the special regime. Note that biomass pricing has been difficult. At first, market for biomass did not respond to FIT comparably to solar or wind, as happened as well in Germany (Kema, 2009). This technology, with slower reaction times and very particular challenges (fuel supply logistics, feed stocks, diversity of technologies, etc.), needed a higher support level and longer to be pushed up. Now in Spain we assist to an incipient but generalised development in the whole country of biogas and waste biomass plants. In case of voltage dips (short drops in voltage in a system), a decoupling from the grid is required for security reasons. This can lead however to the decoupling of a whole wind farm, which can totally destabilise the electric system. There has been a great effort made in Spain (although not yet implemented in Portugal, which affects the Iberian electric system) to make wind power farms able to ride through these electric faults. Wind installations capable for short drop in voltage may perceive an economic incentive. Thus, according to Red Eléctrica de España, in 2009 the biggest wind power loss due to voltage dips has been 700MW despite having a total installed capacity of 19.000MW. This complement may be introduced also for photovoltaic in the future. • FIT adjustment and revision

- 8. In Spain, the tariffs and premiums are fixed for the entire life of the plant. The level of support decreases however for some technologies: after 15 years for biomass and biogas, and after 25 years for photovoltaic. These tariffs are planned to be inflation adjusted yearly according to the consumer price index (CPI) and fuel prices. This is a way to protect investors, which are committed to renewable energy project for as much as forty years (Burgie, 2009). Revision is a broader process in which the FIT may be substantively altered. RD 661/2007 established that, as 85% of capacity cap for 2010 would be covered, they would be given at least 12 months to receive the same tariff, which happened for solar already in 2007. Table 1 shows the rate of fulfillment of these caps in April 2010, and shows that the 85% capacity cap has been exceeded for solar and for wind. Installed Capacity cap Rate of capacity (MW) (MW) fulfilment (%) CHP 6.312 9.215 68% Solar PV 3.472 1.331 261% Solar termal 136 500 27% Wind 18.401 20.155 91% Wind (repowering) 0 2.000 0% 1.405 2.400 59% Small hydro =< 10MW Biomass 510 1.317 39% Biogas and manure 180 250 72% Solid waste 279 350 80% Table 1: Capacity caps and rate of fulfilment in April 2010 (CNE, 2010) • RE Quotas After the unexpected boom of PV in 2008, the government decided to set a solar quota, not only through a new cap for 2009, 2010, and so on, but also with the addition of a registry that will keep record of each new project. If the quota is reached, the actual tariff decreases each year 10%, starting in 2009 with 32 c€/kWh. This quotas and registry system was extended to the rest of the Special Regime in 2009, to break down an incipient “bubble” in solar thermal technology. Analysis of the Spanish case and lessons learned If we analyse the development of renewable electricity in Spain with its FIT system in terms of its effectiveness in increasing installed capacity and energy generation, the results are quite spectacular (Figure 2). Nevertheless since 2007 we have assisted to several sudden changes in regulation that show the difficulties of the system adopted. Let us analyse this turbulent evolution and other critics raised to Spanish FITs. 1. The evolution of RE installation and of changing legislation

- 9. 35.000 30.000 TRAT.RESIDUOS 25.000 RESIDUOS 20.000 BIOMASA HIDRÁULICA 15.000 EÓLICA SOLAR 10.000 COGENERACIÓN 5.000 0 90 92 94 96 98 00 02 04 06 08 19 19 19 19 19 20 20 20 20 20 MW Figure 2: Evolution of installed capacity of technologies in Special Regime in Spain (CNE, 2010). Despite a relatively stable policy in theory (Spain is the only country to date where tariffs are granted during the whole lifetime of the installation), investor certainty has not been provided. If we look at the boom and burst of solar PV in Spain, we see that in august 2007 the 85% of the 2010 capacity cap set for solar had already been reached. A revision of tariffs was expected for September 2008, but the new tariff was not known before. This led to a great uncertainty among project developers, who rushed to complete PV projects on time for fear of getting a lower tariff (which could have even lead to fraud in some cases). This caused a spectacular increase in PV capacity in 2008 (Figure 2) and caused the developers rush installing new plants which could lead to an overdevelopment and lock‐in of inferior technologies at the best resource sites. As he himself claimed, the government had relied on the forecasts of industry associations and could not keep track of the actual projects that were being installed. The 2008 result was therefore a surprise for them. Actually, in 2010 the 2010 capacity cap has been exceeded by a 261% (Table 1). After this, the government decided to create a registry for new projects (first for photovoltaic, and then for the rest of technologies), as described before, and a degressive tariff after the reach of a quota. The uncertainty goes on today: a global revision of retributive system seems to be currently on the table, but no official draft has been released yet. In 2010 after denunciation in press of possible frauds in PV, rumors have been circulating on radical tariff cuts and even on the possibility of being retroactive, which have lead to a collapse on the stock exchange for renewables industry and to the halting of new investments. In 2010 is also expected a new “Renewable Energy Plan” (former plan was in force 2005‐2010) and the revision of the Special Regime Royal Decree. On the other hand, the tariff set for PV has been criticised for being set too high from the outset (similar tariffs than in Germany with much more sunshine). A balance has to be found between a sufficient FIT that will allow the development of a yet unmature

- 10. technology and a too high tariff that incentivise a technology still inefficient, uneconomic or even speculative. 2. Cost for the community Despite a rise on fuel prices and therefore on generation costs and electricity prices, the consumer tariffs where not correspondingly increased by the government. This decoupling between the electricity tariff and the actual cost was made possible with the RD 1432/2002 and has created the so‐called “energy deficit”: difference between the amount collected from consumers through the tariff set by the Government and the actual costs of generation, transportation, distribution, etc. The different items included in this cost and their distribution in volume are detailed in Figure 3. This deficit will be amortized in the next years, therefore it is a debt to be paid for future consumers although created by current consumption. Special Regime FITs were included into this consumer’s tariff, representing 37% of 2010 total costs. Even if the rise in renewables and CHP retribution cannot be considered the sole cause of the energy deficit, the exponential increase of solar in 2008 with its high retribution had a relevant impact on the actual costs and therefore on the deficit. Thus, the Government himself stated in the decree 1578/2008, despite his declared commitment towards renewables, that "Energy sources under this special regime constitute a risk for the system's sustainability because of their effects on power prices." This suggests that RE were blamed for the energy deficit, as the tariff has not risen that much. The total payment for renewables and CHP amounted in April 2010 €660 million, from which FV and wind power were both paid about €210 million. For 2009 tariffs and premiums paid for RE amounted for 5.000 million (CNE, 2010). The energy deficit, however, is not circumstantial but really structural, as it has been used by the government as a strategy to fix a consumption tariff whose maximum rise was determined in advance: electricity rates were kept artificially low. Otros costes Servicio gestión 3% interrumpibilida d Transporte 3% 9% Primas Régimen Distribución Especial 31% 37% Déficit tarifario Moratoria 11% Compensación Nuclear extrapeninsular 0% 6% Figure 3: Distribution of the different costs in the access toll of consumption electricity tariff (BOE, 2009)

- 11. 3. Impact on prices: reaching zero spot prices Figure 4 describes the price fixation based on merit order, while crossing demand and supply curves. The demand curve is inelastic; therefore minor changes in the supply can result in major price changes. As renewable power, like wind or solar, has a low marginal cost due to zero fuel costs, their bids enter the supply curve at the lowest level. This shifts the supply curve to the right, resulting in a lower power price. This ‘merit order effect’ can range, according to various studies, 3‐23€/MWh for wind power (Morthost, 2010). The total amount of savings made due to the wind power penetration has been evaluated within a range of €1.3‐5 billion per year in Germany or €0.1 billion for 2006 in Denmark. Figure 4: Demand and supply curve for price fixation (www.omel.es) In Spain, GELABERT et al. (2009) have concluded that an increase in the generation of renewable energy sources under the Special Regime by 1 GWh would result in a decrease on electricity prices by around 2.5 Euros on average, or around 5%. However, the decrease of electricity price (pool) will not directly affect consumers, as price is set by tendering. It is nevertheless important to note that this effect can be just temporary because “when this decrease in electricity prices takes place, the signal for investment is also reduced and thus future investments are reduced, bringing about a subsequent increase in electricity prices. In addition, when market power exists, traditional producers may bid higher in order to keep the price level as before” (GELABERT et al, 2009). The merit order effect can eventually result in zero spot prices, part of which can be attributed to renewable power generation. Low or zero spot price results in lower incomes for generators, but also in a lower cost for the general system. Nevertheless, Spanish government and energy producers consider this as a failure of the system and ways of avoiding it are being discussed. The whole electricity system could be revised and Special Regime could be taken off the spot market.

- 12. During the first four months of 2010, Spanish market has experienced 293 hours of zero spot prices (CNE, 2010), i.e. 10% of the total amount of hours. This can be attributed to the high production of wind and hydro power and a lower demand. To finish, we can note that the Spanish system “special regime” has not been thought for broad distributed generation. This makes Spanish goals different from Germany (where one third of Germany’s wind power is owned by 200.000 local landowners) or Denmark (where 150.000 families own 80% of installed turbines) (WFC, 2009). This is not necessarily a planning error, but makes it more difficult to implement a distributed generation system where renewable energies supply local demand and go beyond the problems created by a centralised regime. III. FINAL REMARKS Spain has embraced more than 15 years ago a green electricity support policy which has since then proven to be one of the most efficient tools for promoting renewable energies in the electricity market. This pioneer position can explain some of the difficulties experienced by the successive governments which have lead to a major discussion on the sustainability of the system. Anyway, difficulties should not make us forget the innovative and interesting solutions implemented in Spanish market to ensure a great and high quality integration of electricity from renewable energy sources: ‘Green’ electricity represented almost 40% of the electricity generation in April 2010. The main difficulty is perhaps the lack of a consistent, clearly defined, long‐term strategy, which leads therefore to a great uncertainty for investors and project developers. It is certain that it is difficult to adjust a tariff from the outset for a new, immature technology as was the photovoltaic; but effectively the tariff seemed to have been set to high, without a good capacity cap control, encouraging uncontrolled development and promoting quantitative capacity increase at the expense of quality and with an exponential costs escalation. A well defined revision mechanism and a degressive tariff, among other measures, could have helped. An additional problem was the decoupling between actual generation costs and consumers tariff due to a political decision to contain the tariff rise. As the amount paid to FIT system grows, the debt for future consumers due to energy deficit has to be kept, entering a vicious circle. Again, the numerous and sudden legislative adjustments to try to solve the detected problems have contributed to investors uncertainty. 2010 might be a key year to solve this uncertainty and design a new, re‐adapted system.

- 13. REFERENCES BOE (2009): Orden ITC/3519/2009, de 28 de diciembre, por la que se revisan los peajes de acceso a partir de 1 de enero de 2010 y las tarifas y primas de las instalaciones de régimen especial BURGIE, B. and CRANDALL, K. (2009): The Application of Feed‐in Tariffs and Other incentives to Promote Renewable Energy in Colorado, Colorado Public Utilities Commission, Denver CNE (2010): “Informe mensual de ventas de energía del régimen especial”, 10/04/2010 COMISIÓN EUROPEA (2008): The support of electricity from renewable energy sources, SEC(2008)57. COMISIÓN EUROPEA (2009): The renewable energy progress report, SEC(2009) 503 final. DECC (2010) : Feed in Tariffs. Government’s response to the Summer 2009 consultation, Department of Energy & Climate Change, London. DEL RÍO, P. (2009): “La Promoción de la electricidad renovable en España en el contexto europeo”, ICE nº 847 DELOITTE (2009): Estudio macroeconómico del impacto del sector eólico en España FINON, D. and MENANTEAU, P. (2004): “La promotion des énergies renouvelables dans les nouveaux marchés électriques concurrentiels », Anales des Mines‐Réalités Industrielles FRONDEL D., RITTER, N. and VANCE, C. (2009): Economic impacts from the promotion of renewable energies: the German experience, RWI GELABERT, L., LINARES, P. and LABANDEIRA, X. (2009) 'Renewable Energy and Electricity Prices in Spain', Working Paper AEEE 09‐2009 HADJSAÏD, N.(2010): La distribution d’énergie électrique en présence de production décentralisée, Lavoisier. KEMA(2009): California Feed‐In Tariff design and policy options, Oakland KPMG (2009): Informe estratégico para el sector fotovoltaico en España: acercándonos a la paridad de red MITYC (2010): “Energías renovables: situación y objetivos”, Ministerio de Industria, Turismo y Comercio. April 2010, Madrid. MORTHOST, P. E. et. Al (2010): Wind energy and electricity prices. Exploring the ‘merit order effect’, Pöyry. WFC(2009): FITness testing: Exploring the myths and misconceptions about feed‐in tariff policies, World Future Council, Washington