Pending court case is not a bar for land tax payment

•

0 j'aime•607 vues

Pending court case is not a bar for land tax payment Solve your land problems in Kerala - we provide Legal support, assistance and monitoring of your complaints in Bhoomi tharam mattom, nilam , purayidom , thottam ,michabhoomi issues, pattayam , thandapper , pokkuvaravu , land tax , building tax , digital survey , resurvey ,klc , puramboke , pathway disputes, fair value , data bank , issues . James Joseph Adhikarathil , Former Deputy collector Alappuzha 9447464502. Service available all over Kerala

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (20)

Similaire à Pending court case is not a bar for land tax payment

Similaire à Pending court case is not a bar for land tax payment (20)

Plus de Jamesadhikaram land matter consultancy 9447464502

Plus de Jamesadhikaram land matter consultancy 9447464502 (20)

Dernier

Dernier (20)

Pending court case is not a bar for land tax payment

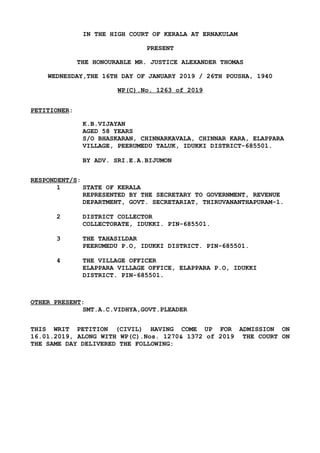

- 1. IN THE HIGH COURT OF KERALA AT ERNAKULAM PRESENT THE HONOURABLE MR. JUSTICE ALEXANDER THOMAS WEDNESDAY,THE 16TH DAY OF JANUARY 2019 / 26TH POUSHA, 1940 WP(C).No. 1263 of 2019 PETITIONER: K.B.VIJAYAN AGED 58 YEARS S/O BHASKARAN, CHINNARKAVALA, CHINNAR KARA, ELAPPARA VILLAGE, PEERUMEDU TALUK, IDUKKI DISTRICT-685501. BY ADV. SRI.E.A.BIJUMON RESPONDENT/S: 1 STATE OF KERALA REPRESENTED BY THE SECRETARY TO GOVERNMENT, REVENUE DEPARTMENT, GOVT. SECRETARIAT, THIRUVANANTHAPURAM-1. 2 DISTRICT COLLECTOR COLLECTORATE, IDUKKI. PIN-685501. 3 THE TAHASILDAR PEERUMEDU P.O, IDUKKI DISTRICT. PIN-685501. 4 THE VILLAGE OFFICER ELAPPARA VILLAGE OFFICE, ELAPPARA P.O, IDUKKI DISTRICT. PIN-685501. OTHER PRESENT: SMT.A.C.VIDHYA,GOVT.PLEADER THIS WRIT PETITION (CIVIL) HAVING COME UP FOR ADMISSION ON 16.01.2019, ALONG WITH WP(C).Nos. 1270& 1372 of 2019 THE COURT ON THE SAME DAY DELIVERED THE FOLLOWING:

- 2. WP(C).Nos. 1263, 1270 & 1372 of 2019 -:2:- ALEXANDER THOMAS, J. = = = = = = = = = = = = = = = = = W.P.(C) Nos.1263, 1270 & 1372 of 2019 - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - Dated this the 16th day of January, 2019 J U D G M E N T The prayers in Writ Petition (Civil) No.1263 of 2019 are as follows: “i) A writ of mandamus or any other appropriate writ or order directing the 4th respondent to accept the property land tax in Sy.No. 1006/6 of Elappara Village in Peerumedu Taluk. ii) any other appropriate writ, order or direction as the Hon'ble Court may pleased to grant in the circumstances of the case.” 2. The prayers in Writ Petition (Civil) No.1270 of 2019 are as follows: “i) A writ of mandamus or any other appropriate writ or order directing the 4th respondent to accept the property land tax in Sy.No. 1006/2 of Elappara Village in Peerumedu Taluk. ii) any other appropriate writ, order or direction as the Hon'ble Court may pleased to grant in the circumstances of the case.” 3. The prayers in Writ Petition (Civil) No.1372 of 2019 are as follows: “i) A writ of mandamus or any other appropriate writ or order directing the 4th respondent to accept the property land tax in Sy.No. 1019 of Elappara Village in Peerumedu Taluk. ii) any other appropriate writ, order or direction as the

- 3. WP(C).Nos. 1263, 1270 & 1372 of 2019 -:3:- Hon'ble Court may pleased to grant in the circumstances of the case.” 4. Heard Sri. E.A. Bijumon, the learned counsel appearing for the petitioner in these three cases and Smt. A.C.Vidhya, the learned Government Pleader appearing for the respondents. 5. According to the petitioner, he is the absolute owner having title, possession and enjoyment of the respective properties covered by Ext.P-2 and the petitioner had submitted applications as per Ext.P-1 produced in these three cases on 10.12.2018 before the 4th respondent- Village Officer for accepting of basic land tax in respect of the above said properties concerned. It is stated that the 4th respondent has taken the adamant stand that he will not even act upon the said application, on the ground that some civil case is pending in the said property. Ext.P-2 is the encumbrance certificate issued by the Sub Registrar concerned in respect of the aforesaid properties concerned. On account of the pendency of a civil suit (O.S. No.75 of 2017) on the file of the Sub Court, Kattappana, the petitioner would assert that no orders had been passed by the Civil Court in that O.S. or in any other civil proceedings, whereby the revenue officials concerned have been interdicted from accepting basic land tax in respect of the properties concerned. It is stated that in a similar case, the petitioner herein was constrained to approach this Court as the very same 4th

- 4. WP(C).Nos. 1263, 1270 & 1372 of 2019 -:4:- respondent-Village Officer had refused to accept basic land tax in respect of another property citing the pendency of a civil suit and this Court as per judgment dated 15.10.2018 in W.P.(C) No.30997/2018 had held that the said stand of the 4th respondent-Village Officer is illegal and had directed him to immediately accept the basic land tax of the properties concerned and it is only thereafter the 4th respondent was willing to accept basic land tax, in respect of the said property from the petitioner. Further, even if the said property thereafter the petitioner had submitted application for grant of possession certificate and non-attachment certificate for that property, which was also being refused by the very same 4th respondent -Village Officer and this Court as per judgment dated 16.01.2019 in W.P.(C) No.1305 of 2019 had directed the 4th respondent-Village Officer to immediately issue the possession certificate and non-attachment certificate of the said property, etc. It appears that the apprehension of the petitioner is that, as he had previously approached this Court in respect of different property by filing W.P.(C) No.30997/2018, in which this Court had intervened in his favour, the 4th respondent would be taking a prejudiced attitude. Be that as it may, it is only to be held that mere pendency of a civil suit can by no stretch of imagination, be the legal justification for a competent revenue official like the 4th respondent, so as to refuse

- 5. WP(C).Nos. 1263, 1270 & 1372 of 2019 -:5:- acceptance of the basic land tax. The question in that regard, has no longer res integra and does not require any citation of the judicial authority in that regard and it has been so held in catena of rulings of various High Courts and the Apex Court. However, if the 4th respondent-Village Officer has any doubt in that regard, despite the previous judgment rendered by this Court on 15.10.2018 in W.P.(C) No.30997/2018, it is only to be observed that in very many judgments as in Tulasibhai v. State of Kerala[2010(4) KLT 215], it has been held by this Court that pendency of civil suit, revenue recovery proceedings, attachment proceeding etc. cannot be the legal basis for competent revenue official like Tahasilar and Village Officer, to refuse to accept basic land tax from the land holder concerned, as there are no provisions in the Transfer of Registry Rules and Kerala Land Tax Rules, which prohibits the competent revenue officials concerned for accepting of basic land tax on account of mere pendency of such proceedings. The said provision has also been reiterated in the subsequent judgment of this Court as in Nevin Raju v. S. Basheer & Ors.[2015 (3) KLJ 197]. Accordingly, it is only to be ordered and declared that the stand of the 4th respondent-Village Officer that he will not accept basic land tax in respect of the property covered by Exts.P-1 and P-2 on account of pendency of O.S.No.75 of 2007 on the file of the Sub Court, Kattappana or any other

- 6. WP(C).Nos. 1263, 1270 & 1372 of 2019 -:6:- civil proceedings or revenue recovery proceedings or attachment proceedings, etc. would be is nothing; but illegal, ultra vires and would also amount to abdication of the statutory duties and responsibilities under the Kerala Land Tax Act and the Kerala Land Tax Rules, which mandates that competent revenue official like the 4th respondent is bound to collect land tax from the land holder concerned as understood in Section 3(3) of the Kerala Land Tax Act. This is the specific mandate of the legislature as made in Section 5(2) read with Section 3(3) of the Kerala Land Tax Act, 1972. As already observed by this Court in very many cases of this nature, the Kerala Land Tax Act and the Kerala Land Tax Rules appears to be the only branch of taxation law, wherein the tax payers are running after the tax collectors to pay the tax dues, and the tax collectors (competent revenue officials) in many a case are taking the adamant stand in delaying or refusing to accept the basic land tax on irrelevant and grounds which are not germane for such refusal. This leads to the inevitable result that aggrieved parties are forced to litigate before this Court in matters which should have been routinely resolved by the competent revenue officials concerned. 6. Even though the Transfer of Registry Rules, which is a non- statutory rule, is subservient to the provisions of the Kerala Land Tax Act

- 7. WP(C).Nos. 1263, 1270 & 1372 of 2019 -:7:- and the Kerala Land Tax Rules, more so in view of the mandate of Section 4 of the said Act, still for the sake of completion of procedural formalities , it will be only in the fitness of things that the petitioner makes separate applications for grant of mutation in respect of the separate properties covered in these three petitions, in case of mutation has not so far been effected. Irrespective of that, it is ordered that the 4th respondent-Village Officer may immediately take up the request made by the petitioner in Ext.P-1 application for acceptance of basic tax and will afford a reasonable opportunity of being heard to the petitioners and will consider the said request and grant it, if it is otherwise in order, within three weeks from the date of production of a certified copy of this judgment. 7. It is also ordered that in case, the properties have not been mutated in the name of the petitioner, then the said application for mutation should also be considered, after due notice to the petitioner and decision thereon will be taken without much delay. Further, it is also ordered in order to avoid unnecessary future litigative proceedings that in case, the petitioner makes formal application for grant of possession certificate, location sketch, non-attachment certificate, etc. the said requests will also be considered and will be granted, if it is otherwise in order. It is hoped and expected that the 4th respondent will not

- 8. WP(C).Nos. 1263, 1270 & 1372 of 2019 -:8:- unnecessarily make the petitioner to run from pillar to post and this Court expects that a competent and responsible revenue official like the 4th respondent would rise up to the occasion, fully keeping in mind, the heavy responsibilities placed on his shoulders by the legislature to collect basic land tax as imposed in Section 5(2) of the Kerala Land Tax Act from “land holders” as understood in Section 3(3) of the said Act. With theses observations and directions, these Writ Petitions (Civil) will stand disposed of. Sd/- ALEXANDER THOMAS JUDGE DST

- 9. WP(C).Nos. 1263, 1270 & 1372 of 2019 -:9:- APPENDIX PETITIONER'S/S EXHIBITS: EXHIBIT P1 TRUE COPY OF THE APPLICATION DATED 10.12.2018. EXHIBIT P2 TRUE COPY OF THE ENCUMBRANCE CERTIFICATE DATED 30.11.2018. RESPONDENTS' EXHIBITS:NIL //True copy// P.A.To Judge