Three Types of Markets

•Télécharger en tant que PPT, PDF•

0 j'aime•84 vues

Three Types of Markets

Recommandé

Contenu connexe

Tendances

Tendances (20)

Similaire à Three Types of Markets

Similaire à Three Types of Markets (20)

Plus de narman1402

Dernier

Dernier (20)

Three Types of Markets

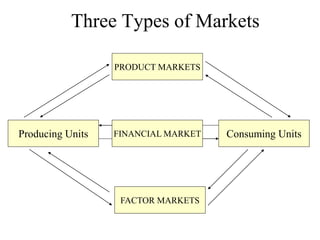

- 1. Three Types of Markets PRODUCT MARKETS FINANCIAL MARKET Producing Units Consuming Units FACTOR MARKETS

- 2. What is a Market? • An institution set up by society to allocate resources that are scarce relative to the demand for them. • Determines what goods and services will be produced and what quantities • Accomplished through changes in prices • Distribute income • Financial market is a market in which financial assets (securities) such as stocks and bonds can be purchased or sold

- 3. Savings and Investments • Savings (S) – Households: Income - Consumption – Businesses: Current Retained Earnings – Government:Current Revenues – Current Expenditures • Investments (I) – Households: Cars, homes, durable goods – Businesses: Fixed assets – Government: Highways, buildings

- 4. Demanders of Funds Business firms Government Suppliers of Funds Households Rest of the World Savings(Loanable funds) Financial services, incomes, and financial claims Exchange of current income for future income and transformation of savings into investments. Suppliers receive only promises (financial claims) Financial asset is a claim against the income or wealth of a business firm, household, or a unit of government represented by a certificate, receipt, computer file, etc.

- 5. Broad Classification of Financial Markets • Money versus Capital Markets • Primary versus Secondary Markets • Organized versus Over-to-Counter Markets • Open versus Negotiated Markets • Spot versus Futures, Forward, and Option Markets • Bank-dominated financial systems versus security-dominated financial systems

- 6. Primary versus Secondary Markets • Primary – New issues – Exchange of funds for financial claim – Funds for borrower • Secondary – Trading previously issued securities – No new funds for issuer – Provides liquidity for seller

- 7. Primary Markets versus Secondary Markets • Primary Markets – Users of Funds (corporations)…Investment Bank…..Suppliers (public) – IPO and underwriting • Secondary Market – FM……….Securities Brokers……….Other Suppliers of Funds – Stocks: NYSE, AMEX, and NASDAQ – Bonds: OTC – Large trading volume – Liquidity and diversification benefits for investors – Liquidity and information about the prices or the value for borrowers – Low transaction costs at centralized markets • Group Question – Issuers receive no funding from secondary market transactions; thus, they do not care about these transactions. Do you agree or disagree? Explain.

- 8. Money Markets versus Capital Markets • Money Markets (Maturities one year or less) – Securities: Commercial paper, federal funds and repurchase agreements, U.S. Treasury bills, negotiable CDs, banker’s acceptances – Participants: Banks, mutual funds, corporations, Federal Reserve Bank, etc. – Very small price fluctuations • Capital Markets – Securities: Stocks, residential mortgages, corporate bonds, Treasury securities, state and local government bonds, U.S. government owned agencies, U.S. government sponsored agencies, bank and consumer loans • Financial Market Regulations – Securities and Exchange Commission (SEC)

- 9. Popular Securities • Type Issued by Maturity • Treasury bills Fed Gov’t 13,26,52 weeks • CDs Banks&Savings Inst 7 days to 5 yrs • NCDs Large banks&Savings Ins 2 weeks to 1 yr • Commercial paper Banks, Large firms 1 day to 270 days • Eurodollar deposits Banks outside U.S 1 day to 1 yr • Banker’s acceptances Banks 30 days to 270 days • Federal funds Depository institutions 1 day to 7 days • Repurchase agreements F, FI 1 day to 15 days • Treasury notes and bonds Fed Gov’t 3 to 30 years • Municipal bonds State and local gov’t 10 to 30 yrs • Corporate bonds Firms 10 to 30 yrs • Mortgages Households and firms 15 to 30 years • Equity securities Firms No maturity

- 10. Foreign Exchange Markets (FX) • Spot Market – The immediate exchange of currencies at the current (spot) exchange rate • Forward Market – The exchange of currencies at a given exchange rate (forward exchange rate) at some prespecified date in the future. (Usually for one-,three-, or six-month periods) • Companies operating globally face foreign exchange risk. – Foreign exchange risk: The sensitivity of the value of cash flows on foreign investments to changes in the foreign currency’s price in terms of dollars. • OTC Market and FIs continuously trade foreign currencies among themselves. • Techniques for hedging FX risk (futures, options, swaps) • Rapid growth of mutual funds and pension funds • Increased consolidation of financial institutions via mergers • Increased competition between financial Institutions • Growth of financial conglomerates

- 11. Organized versus Over-to-Counter • Organized OTC – Visible place Wired network of dealers – Members trade No central, physical place – Securities listed – NYSE Securities traded off exchanges

- 12. Open versus Negotiated • Open Negotiated – Highest bidder Private contracting • Spot versus Futures, Options – Spot Futures Options – Immediate delivery – Future delivery – Right to buy/sell

- 13. Types of Financial Institutions • Direct Finance: Borrowers(Users)…Cash...Lenders(Suppliers) • Indirect Finance: Users…… FI…..Suppliers Depository FI Commercial banks Savings institutions Credit unions Nondepository FI Insurance companies Mutual funds Pension funds Securities brokers and dealers Finance companies Mortgage companies Real estate investment trusts

- 14. Financial Institutions • Recent Trends – Rapid growth of mutual funds and pension funds – Increased consolidation of financial institutions via mergers – Increased competition between financial Institutions – Growth of financial conglomerates

- 15. Functions of FI: Benefiting Lenders • Monitoring Costs – Suppliers…….FI as a delegated monitor……Borrowers – Aggregation of funds and thus large size of FI provide incentives to collect information and monitor the borrowers. – FI ability – Lower costs of monitoring (economies of scale) • Liquidity and Price Risk – Provide additional claims to lenders, thus acting as asset transformers – Liquidity attributes are superior to primary securities – Usually fixed principal and a guaranteed rate – FIs’ ability to diversify away some of their investment risks allow them to convert less liquid, higher price risk securities into more liquid and less price risk securities. • Reduced Transaction Costs • Maturity Intermediation • Denomination Intermediation (Mutual Funds)

- 16. Functions of FI: Benefiting the Financial System • Transmission of Monetary Policy – Definitions of money supply: M1, M2, and M3 – Depository institutions are instrumental in determining the size and growth of the money supply – Depository institutions are designated as the primary conduit for FR actions. • Credit Allocation – Particular sectors being in special need of financing • Intergenerational Wealth Transfers or Time Intermediation – Pension plans and life insurance companies • Payment Services

- 17. Risks Faced by FI • Interest rate risk • FX Risk • Market risk • Credit risk • Liquidity risk • Off-Balance sheet risk • Technology risk • Operational risk • Country or Sovereign risk

- 18. Valuation and Efficient Markets • Value a function of: – Future cash flows – When cash flows are received – Risk of cash flows – Market conditions • Present value of cash flows discounted at the market required rate of return • Value determined by market demand/supply • Market efficiency – Security prices reflect available information – New information is quickly included in security prices – Investors balance liquidity, risk, and return needs – Disclosures and asymmetry of information

- 19. The Efficient Market Hypothesis (EMH) • Information: Past, publicly available, insiders • Prices reflect information • No excess return by trading on information • Each asset generates a normal return commensurate with its level of risk.

- 20. Asymmetric Information: Remedies Public disclosure SEC (Security Exchange Commission: Financial reports) GAAP (Generally accepted accounting principles) RAP (Regulatory accounting principles) CAMEL ratings (Capital adequacy, Asset quality, Managerial ability, Earnings, and Liquidity) Safety and Soundness Capital regulation of FI Stock Market Circuit Breakers

- 21. Regulations of FI: Why are FI regulated? • To Promote Efficiency High level of competition Efficient payments mechanism Low cost risk management contracts • To Maintain Financial Market Stability Prevent market crashes Prevent Inflation--Monetary policy Prevent Excessive Risk Taking by Financial Institutions • To Provide Consumer Protection • Provide adequate disclosure • Set rules for business conduct • To Pursue Social Policies • Transfer income and wealth • Allocate saving to socially desirable areas • Insolvency risk

- 22. Globalization of FM and FI • Increased international funds flow – Increased disclosure of information – Reduced transaction costs – Reduced foreign regulation on capital flows – Increased privatization • Group Question: Do the governments of emerging economies have a role to play in determining how much net capital inflow they receive and where it is employed?