Recommandé

Recommandé

Contenu connexe

Similaire à ACTIVITY BASED COSTINGService TypeActivity Dri.docx

Similaire à ACTIVITY BASED COSTINGService TypeActivity Dri.docx (20)

Plus de normanlane62630

Plus de normanlane62630 (20)

Dernier

Dernier (20)

ACTIVITY BASED COSTINGService TypeActivity Dri.docx

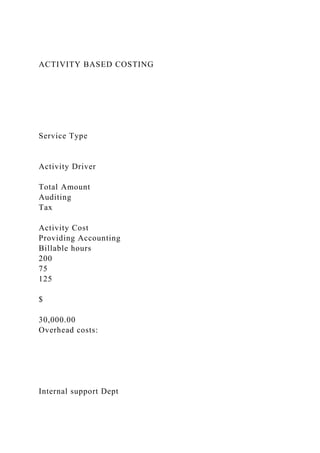

- 1. ACTIVITY BASED COSTING Service Type Activity Driver Total Amount Auditing Tax Activity Cost Providing Accounting Billable hours 200 75 125 $ 30,000.00 Overhead costs: Internal support Dept

- 2. Preparing documents docs 30 16 14 $ 4,000.00 Occupying office space hours 200 75 125 $ 1,200.00 Utilties hours 200 75 125 $ 350.00

- 3. External support departments Registering documentation docs 30 16 14 $ 1,250.00 Consultants days 6 5 1 $ 10,000.00 Contract services days 6 5 1

- 4. $ 5,000.00 Total overhead costs $ 51,800.00 Gotham Accounting Firm provides tax and auditing services to a variety of clients. Attorneys keep track of the time they spend on each case, which is used to charge fees to clients at a rate of $300 per hour. A management advisor commented that activity- based costing might prove useful in evaluating the costs of its services, and the firm has decided to evaluate its fee structure by comparing ABC to its alternative cost allocations. The following data relate to a typical month at the firm. During a typical month the firm handles seven mediation cases and three litigation cases. Required Determine the cost of providing services to each type of case using activity-based costing (ABC). Determine the cost of each type of case using a single plantwide rate for nonattorney costs based on billable hours.

- 5. Determine the cost of each type of case using multiple departmental overhead rates for the internal support department (based on number of documents) and external support department (based on billable hours). Compare and discuss the costs assigned under each method for management decisions. COST VOLUME PROFIT Texon Co. manufactures and sells three products: product 1, product 2, and product 3. Their unit sales prices are product 1, $40; product 2, $30; and product 3, $14. The per unit variable costs to manufacture and sell these products are product 1, $30; product 2, $20; and product 3, $8. Their sales mix is reflected in a ratio of 6:3:5. Annual fixed costs shared by all three products are $200,000. One type of raw material has been used to manufacture products 1 and 2. The company has developed a new material of equal quality for less cost. The new material would reduce variable costs per unit as follows: product 1 by $10, and product 2, by $5. However, the new material requires new equipment, which will increase annual fixed costs by $50,000. Required If the company continues to use the old material, determine its break-even point in both sales units and sales dollars of each individual product. If the company uses the new material, determine its new break- even point in both sales units and sales dollars of each individual product. What insight does this analysis offer management for long-term planning?

- 6. VARIABLE COSTING Navaroli Company began operations on January 5, 2014. Cost and sales information for its first two calendar years of operations are summarized below. Manufacturing costs Direct materials $80 per unit Direct labor $120 per unit Factory Overhead Variable

- 7. $30 per unit Fixed $14,000,000 Nonmanufacturing costs Variable Selling and administrative $10 per unit Fixed selling and administrative $8,000,000

- 8. Production and sales data Units produced in 2014 200,000.00 Units sold in 2014 140,000.00 Units in ending inventory, 2014 60,000.00 Units producd in 2015 80,000.00 Units sold in 2015 140,000.00 Units in ending inventory 2015

- 9. 0 Sales price per unit $600 Required 1. Prepare an income statement for the company for 2014 under absorption costing. 2. Prepare an income statement for the company for 2014 under variable costing. 3. Explain the source(s) of the difference in reported income for 2014 under the two costing methods. 4. Prepare an income statement for the company for 2015 under absorption costing. 5. Prepare an income statement for the company for 2015 under variable costing.

- 10. 6. Prepare a schedule to convert variable costing income to absorption costing income for the years 2014 and 2015. MASTER BUDGETS November Company's management asks you to prepare its master budget using the following information. The budget is to cover the months of April, May, & June 2015 Additional Information Sales for March total 10,000 units. Each month's sales are expected to exceed the prior month's results by 5%. The product's selling price is $25 per unit. Company policy calls for a given month's ending inventory to equal 80% of the next month's expected unit sales. The March 31 inventory is 8,400 units, with a value of $126,000 which complies with the policy. The purchase price is $15 per unit. Sales representatives' commissions are 12.5% of sales and are paid in the month of the sales. The sales manager's monthly salary will be $3,500 in April and $4,000 per month thereafter. Monthly general and administrative expenses include $8,000 administrative salaries, $5,000 depreciation, and 0.9% monthly interest on the long-term note payable. The company expects 30% of sales to be for cash and the remaining 70% on credit. Receivables are collected in full in the month following the sale (none is collected in the month of the sale). Beginning accounts receive is $175,000. All merchandise purchases are on credit, and no payables arise from any other transactions. One month's purchases are fully paid in the next month.

- 11. Beginning accounts payable is $156,000. The minimum ending cash balance for all months is $50,000. If necessary, the company borrows enough cash using a short-term note to reach the minimum. Short-term notes require an interest payment of 1% at each month-end (before any repayment). If the ending cash balance exceeds the minimum, the excess will be applied to repaying the short-term notes payable balance. Beginning balance in short-term note is $12,000. Dividends of $100,000 are to be declared and paid in May. No cash payments for income taxes are to be made during the second calendar quarter. Income taxes will be assessed at 35% in the quarter. Equipment purchases of $55,000 are scheduled for June. Required: Prepare the following budgets and other financial information as required: 1. Sales budget, including budgeted sales for July. 2. Purchases budget, the budgeted cost of goods sold for each month and quarter, and the cost of the June 30 budgeted inventory. 3. Selling expense budget. 4.

- 12. General and administrative expense budget. 5. Expected cash receipts from customers and the expected June 30 balance of accounts receivable. 6. Expected cash payments for purchases and the expected June 30 balance of accounts payable. 7. Cash budget. 8. Budgeted income statement. 9. Budgeted statement of retained earnings. 10. Budgeted balance sheet. Flexible Budgets Pacific Company provides the following information about its budgeted and actual results for June 2015. Although the expected June volume was 25,000 units produced and sold, the company actually produced and sold 27,000 units as detailed

- 13. here: Budget Actual 25,000 units 27,000 units Selling price $ 5.00 $ 5.23 Variable costs

- 14. Direct materials $ 1.24 $ 1.12 Direct labor $ 1.50 $ 1.40 Factory supplies $ 0.25 $

- 17. 485.00 Other $ 750.00 $ 900.00 In dicates factory overhead item: $0.75 per unit or $3 per direct labor hour for variable overhead, and $0.25 per unit or $1 per direct labor hour for fixed overhead. Standard costs based on 25, 000 units output

- 18. Per unit of output Quantity to be used Total Cost Direct materials, 4 oz @ $0.31 per ounce $ 1.24 100000 oz $ 31,000.00 Direct labor, 0.25 hour @ $6 per hour $ 1.50 6250 hrs $ 37,500.00

- 19. Overhead $ 1.00 $ 25,000.00 Actual costs Direct materials 4 oz @ 0.28 $ 1.12

- 20. 108,000 oz $ 30,240.00 Direct labor .2 hr @$7 per hr $ 1.40 5400 hrs $ 37,800.00 Overhead $ 1.20 $ 32,400.00 Standard costs based on 27, 000 units output

- 21. Per unit of output Quantity to be used Total Cost Direct materials, 4 oz @ $0.31 per ounce $ 1.24 100000 oz $ 33,480.00 Direct labor, 0.25 hour @ $6 per hour $ 1.50 6750 hours $

- 22. 40,500.00 Overhead $ 26,500.00 Required Prepare June flexible budgets showing expected sales, costs, and net income assuming 20,000, 25,000, and 30,000 units of output produced and sold. Prepare a flexible budget performance report that compares actual results with the amounts budgeted if the actual volume had been expected. Apply variance analysis for direct materials and direct labor. Compute the total overhead variance, and the controllable and volume variances. Compute spending and efficiency variances for overhead. Prepare journal entries to record standard costs, and price and quantity variances, for direct materials, direct labor, and factory overhead. PROCESS COSTING PROBLEM Spectre Chemicals produces Canovic in a two department process.

- 23. Information on the two departments for March and April, 2016 are as follows: March 2016: Department 1: The Company had beginning inventory of 6,000 units, 40% completed with a cost of $45,000. During the month, the department transferred in 22,000 units of the direct materials with a cost of $10 per unit. Ending inventory was 7,000 units, 30% completed. Direct labor is $310,500 and factory overhead is $103,500. Department 2: The Company had beginning inventory of 5,000 units, 70% completed with a cost of $80,000. During the month, direct labor was $175,000 and factory overhead was $87,500. Ending inventory was 10,000 units, 50% completed. April 2016: Department 1:

- 24. During the month, the department transferred in 20,000 units of the direct materials with a cost of $11 per unit. Direct labor is $209,000 and factory overhead is $104,500. Ending inventory is 10,000 units 60% completed. Department 2: During the month, direct labor is $175,000 and factory overhead is $87,500. The company had ending inventory of 5,000 units, 70% completed with a cost of $80,000. Required: Compute the Equivalent Units of Production, Material costs, and Conversion costs for each department for March and April, 2014. Complete the attached chart – one for each department and each month Prepare a cost of production report for March and April 2014.