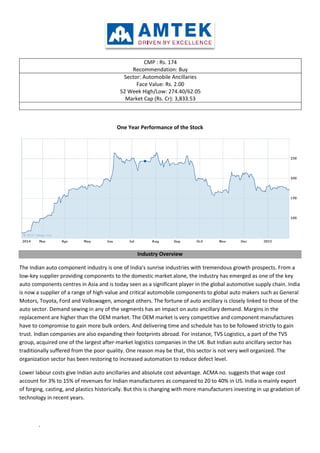

1. CMP : Rs. 174

Recommendation: Buy

Sector: Automobile Ancillaries

Face Value: Rs. 2.00

52 Week High/Low: 274.40/62.05

Market Cap (Rs. Cr): 3,833.53

One Year Performance of the Stock

Industry Overview

The Indian auto component industry is one of India's sunrise industries with tremendous growth prospects. From a

low-key supplier providing components to the domestic market alone, the industry has emerged as one of the key

auto components centres in Asia and is today seen as a significant player in the global automotive supply chain. India

is now a supplier of a range of high-value and critical automobile components to global auto makers such as General

Motors, Toyota, Ford and Volkswagen, amongst others. The fortune of auto ancillary is closely linked to those of the

auto sector. Demand sewing in any of the segments has an impact on auto ancillary demand. Margins in the

replacement are higher than the OEM market. The OEM market is very competitive and component manufactures

have to compromise to gain more bulk orders. And delivering time and schedule has to be followed strictly to gain

trust. Indian companies are also expanding their footprints abroad. For instance, TVS Logistics, a part of the TVS

group, acquired one of the largest after-market logistics companies in the UK. But Indian auto ancillary sector has

traditionally suffered from the poor quality. One reason may be that, this sector is not very well organized. The

organization sector has been restoring to increased automation to reduce defect level.

Lower labour costs give Indian auto ancillaries and absolute cost advantage. ACMA no. suggests that wage cost

account for 3% to 15% of revenues for Indian manufacturers as compared to 20 to 40% in US. India is mainly export

of forging, casting, and plastics historically. But this is changing with more manufacturers investing in up gradation of

technology in recent years.

.

2. GROWTH DRIVERS OF INDIAN AUTO ANCILLARIES INDUSTRY

Destination India:

According to the Investment Commission of India, global automobile manufacturers see India as a manufacturing

hub for auto components and are rapidly increasing the value of components they source from India due to

following facts..

India’s cost competitiveness in terms of labour and raw material.

Its established manufacturing base.

Makers of luxury cars are increasingly looking at making India a sourcing hub for components, besides using more

local components in cars for the Indian market.

BMW is likely to sign the first direct sourcing deal with local vendors by the end of this year. Skoda Auto India is

looking at increasing localization for its small car Fabia to over 50 per cent over the next two years. Mercedes Benz

India expects growth in sourcing from India to continue at 10 per cent.

Supply Side Drivers:

*Competitive

advantages facilitating

emergence of

outsourcing hub.

*Technological shift;

focus on R&D

Demand Side Drivers:

• Robust growth in

domestic automotive

industry.

Policy Support:

•Market liberalisation

•Establishing special

auto parks and virtual

SEZs for auto

components.

•Lower excise duty on

specific parts of hybrid

vehicles.

3. Porter Five Forces Model

Supply: Low for high technology products. Unorganized sector dominates the domestic component market due to

excise benefits. Generally, excess supply persists.

Demand: Linked to automobile demand. Export demand is linked to the increasing acceptance towards outsourcing.

Foreign Investments:

India enjoys a cost advantage with respect to casting and forging as manufacturing costs in India are 25 to 30

per cent lower than their western counterparts. Seeing the growing popularity of India in the automotive component

sector, the Investment Commission has set a target of attracting foreign investment worth US$ 5 billion for the next

seven years to increase India's share in the global auto components market from the existing 0.9 per cent to 2.5 per

cent by 2015.

Swiss auto clamps maker, Oeitker Group, has inaugurated the first phase of its manufacturing facility in

India. It has invested US$ 12.58 million in Phase I and hopes to start work on the second phase by the end of next

year.

Indian

Auto

Ancillaries

Sector

Will intensify, as global players

will enter the market leading

to consolidation.

Dereservation of SSI will result

in access to capital and

technology

Capital, technology, OEM

relationships, customer

service, distribution network

to meet replacement demand

Companies operating in the

export market face

competition at a global level.

At the domestic level, market

structure is fragmented for a

large number of ancillary

products. Most companies

adopt low cost and

differentiation strategies. In

some products (like batteries),

only two or three companies

control over 80% of the

market

Low with OEMs. Relatively

high in the replacement

market

4. The Tamil Nadu state cabinet recently gave clearance to the French tyre major, Michelin’s proposal to set up

a US$ 851.5 million Greenfield project near Chennai, Tamil Nadu.

A memorandum of understanding (MoU) has been signed by the US auto giant, Ford Motors, with the Tamil

Nadu government to set up a unit with a capacity of 250,000 engines a year.

German auto company, Volkswagen has commenced sourcing components from India for its Russian plant

and is also looking at sourcing light systems, plastic related items and metals for its European plants.

Domestic Investments:

The market is so large and diverse that a large number of players can be absorbed to accommodate buyer

needs. The sector not only has global players looking to invest and expand but leading domestic component

companies are also pumping in huge sums into expanding operations. An auto park is coming up near Hyderabad

with investments worth over US$ 409.30 million from around 34 automotive ancillary units. This is in addition to a

US$ 245.59 million Greenfield project being set up by MLR Motors near the park.

Moreover, Indian tyre makers are rolling out investment plans worth US$ 1.24 billion, due to the rising

popularity of radial tyres in the commercial vehicles segment.

Some other investments include:

Apollo Tyres is to scale up investment at its upcoming radial tyre project at Oragadam in Tamil Nadu from

US$ 106.4 million to US$ 447.04 million. Hero Motors will invest US$ 19.84 million in association with Austrian firm

BRP Power train for manufacturing automotive transmissions in India. Indian arm of Swedish automotive component

maker SKF is investing US$ 30 million in a new ball bearings manufacturing plant at Haridwar.

Policy Initiatives

The government has taken many initiatives to promote foreign direct investment (FDI) in the industry.

Automatic approval for foreign equity investment up to 100 per cent of manufacture of automobiles and

components is permitted. The automobile industry has been DE licensed. There are no restraints on import of

components. The government has envisaged the Automotive Mission Plan 2016 to promote growth in the sector. It

targets:

Emerging as the global favourite in the area of design and manufacture of automobiles and auto components.

Taking the output to US$ 145 billion, accounting for more than 10 per cent of the GDP.

R&D

• Joint R&D with

Indian companies

for new product

development and

process

innovation

Process&Design

• Partnerships

with Indian SMEs

to address

product and

process

technologies

• Offshoring

manufacturing

design work to

JVs or partners

based in India

CustomerService

• Opportunity for

strategic alliance

to cover global

customers

Manufacturing

• Greenfield

manufacturing

facilities in India

to meet the

robust domestic

demand potential

• Establish India as

a key link in the

global auto

components

supply chain

5. Offering additional employment to 25 million people by 2016.

Looking Ahead

With investments around US$ 15 billion slated for the sector over the next few years, the prospects

for India's auto market are bright.

Even though India's auto component industry has conventionally relied on exports for its profits, the

domestic market itself is ripe with rapidly growing opportunities.

Industry experts are hopeful that the country will be able to offset China and other Southeast Asian

countries' traditional manufacturing advantage in the coming years, facilitating the industry's

achievement of its targeted market value of US$ 50 billion by 2015

.

SWOT Analysis

Strengths:

Global scale of operations.

Flexible production system.

New innovative and world class technology.

High growth rate.

Amtek is among the world’s largest player in casting, forging, and mchining with global market share of 20% in

turbocharger housing and 15% in ring gears

Weaknesses

Tight liquidity position, reluctance on the parts of banks to finance vehicles and firming up of interest rates would

affect vehicle demand which in turn could impact the company's revenues and profits.

Increase in the prices of inputs like metals, fuel oil etc., and movements in exchange rates and volatility in foreign

exchange markets may create pressure on operating margins.

The Company is also exposed to the risk of Environment and pollution controls, which is associated with such

type of industries.

Opportunities

A growing middle income population, rise in their average income levels and demand for a better lifestyle, all

augur well for the automotive industry both in terms of personal transportation requirements as well as freight

movement.

Continued improvement in roads in the coming years is expected to boost automobile demand.

India continues to be a cost effective source for automotive industry globally both for vehicles and components.

The Government has continued its thrust on infrastructure despite the economic slowdown. The Power sector is

also showing robust growth potential.

Responsiveness to changes in market conditions and product profiles. Dynamic and Progressive leadership,

willing to implement change.

Decreased interest rate will help in cost cutting

Decrease in price of crude will help in cost cut and it will also increase in demand in automobile sector.

6. Favourable policy measures aiding growth

Threats

Increase in fuel prices has an adverse impact on automobile demand as was seen in the previous year.

Hardening of consumer interest rates coupled with tightening of liquidity position and reduction in exposure to

vehicle financing by banks could have an adverse impact on the automotive industry.

Stringent emission norms and safety regulation could bring new complexities and cost increases for automotive

industry.

WTO, Free Trade Agreements could make the market more competitive for local manufacturer.

The domestic passenger vehicle demand could be adversely impacted by the introduction of rapid mass road and

rail transport systems.

Global economic recovery may take longer than expected, which will affect exports from India.

• Automatic approval for 100 per cent foreign equity investment in auto component

manufacturing facilities

• Manufacturing and imports in this sector exempt from licensing and approvals

• Setting up of a technology modernisation fund focusing on small and

medium enterprises

• Establishment of automotive training institutes and auto design centres,

special auto parks and auto component virtual SEZs

• Set up at a total cost of USD 388.5 million to enable the industry to

adopt and implement global performance standards

• Focus on providing low-cost manufacturing and product development

solutions

• Created a USD 200 million fund to modernise the auto components

industry by providing an interest subsidy on loans and investment in new

plants and equipment

• Provided export benefits to intermediate suppliers of auto components

against the Duty Free Replenishment Certificate (DFRC)

• Concessional excise duty of 6 per cent has been extended up to 31 March 2015 for

manufacturers of batteries supplying to producers of electrically operated vehicles

• Exemption from basic customs duty on lithium-ion automotive batteries for

manufacture of lithium-ion battery packs for supply to manufacturers of hybrid and

electric vehicles

7. Financial Analysis

Company’s debt level

Year 2010 2011 2012 2013 2014

Total debt 380865.88 629175.06 822857.59 1413291.56 1516925.00

Financial performance

RatioYear 2010 2011 2012 2013 2014

Debt to equity 0.83 1.08 1.33 2.00 1.94

Debt to capital 0.45 0.52 0.57 0.67 0.66

Debt to asses 0.40 0.43 0.45 0.54 0.50

Financial leverage 2.05 2.31 2.76 3.39 3.80

Interest coverage 2.91 3.34 2.98 2.33 2.24

Company’s debt is increasing highly because company’s inorganic approach for expansion. Company has

acquired many bigger and smaller companies in recent years. These acquisitions helped it in being a major

market share holder. Ideal Debt to equity ratio is 2:1 but here is below than that so debt to equity ratio

here is not a concern. Increasing debt here correlates with the growth of sales and revenue, so this is good

for company and makes it credit worthy.

Sales growth

year 2010 2011 2012 2013 2014

Net sales 369,084.97 486,211.84 720,698.52 988,874.30 1,545,458.00

CAGR of sales for the period 2010-14 is 33%. The company sales shows steady and consistent growth

Sales growth is powerd by inorganic expansion .

Profitability ratio

PROFITABILTY RATIO 2010 2011 2012 2013 2014

NET PROFIT MARGIN 0.07 0.14 0.10 0.07 0.06

GROSS PROFIT MARGIN 0.25 0.26 0.27 0.23 0.22

OPERATING PROFIT MARGIN 0.16 0.18 0.20 0.16 0.16

PRE TAX MARGIN 0.11 0.17 0.13 0.10 0.09

ROA 0.03 0.06 0.05 0.03 0.03

ROE 0.06 0.13 0.12 0.11 0.13

OPERATING RETURN ON

ASSET 0.06 0.08 0.09 0.08 0.09

RETURN ON TOTAL CAPITAL 0.07 0.08 0.10 0.08 0.11

Company’s gross profit margin is in the healthy range of 25%, it shows on the operational side the

company is performing at its best. But heavy debt incurred during acquisitions is having a impact on

the net profit margin.

Return on equity of 13% shows a shareholder can earn a decent return upon investing.

8. Valuation analysis

Year 2011 2012 2013 2014

EV 1,070,335.31 1,318,907.17 1,933,905.83 2,221,205.00

EV/EBIDTA 8.20 6.50 7.79 6.43

EV/SALES 2.20 1.83 1.96 1.44

PE 10.77 4.06 3.95 4.31

BV 248.79 280.02 322.47 355.45

P/BV 0.53 0.39 0.23 0.47

EPS 12.28 26.71 19.16 38.78

With PE around 4, valuation looks cheap for this company and it is a bargain to invest at this

point of time.

With EV/Sales ratios around 2 , it is better than the peers.

Earnings per share has improved very much with CAGR of 31 %.