Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (20)

Similaire à Samridhi agri products private limited

Similaire à Samridhi agri products private limited (20)

Plus de prabhat_rbl

Dernier

Dernier (20)

Samridhi agri products private limited

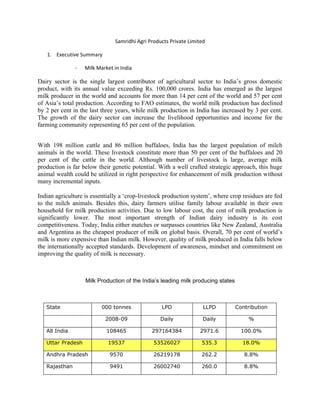

- 1. Samridhi Agri Products Private Limited 1. Executive Summary - Milk Market in India Dairy sector is the single largest contributor of agricultural sector to India’s gross domestic product, with its annual value exceeding Rs. 100,000 crores. India has emerged as the largest milk producer in the world and accounts for more than 14 per cent of the world and 57 per cent of Asia’s total production. According to FAO estimates, the world milk production has declined by 2 per cent in the last three years, while milk production in India has increased by 3 per cent. The growth of the dairy sector can increase the livelihood opportunities and income for the farming community representing 65 per cent of the population. With 198 million cattle and 86 million buffaloes, India has the largest population of milch animals in the world. These livestock constitute more than 50 per cent of the buffaloes and 20 per cent of the cattle in the world. Although number of livestock is large, average milk production is far below their genetic potential. With a well crafted strategic approach, this huge animal wealth could be utilized in right perspective for enhancement of milk production without many incremental inputs. Indian agriculture is essentially a ‘crop-livestock production system’, where crop residues are fed to the milch animals. Besides this, dairy farmers utilise family labour available in their own household for milk production activities. Due to low labour cost, the cost of milk production is significantly lower. The most important strength of Indian dairy industry is its cost competitiveness. Today, India either matches or surpasses countries like New Zealand, Australia and Argentina as the cheapest producer of milk on global basis. Overall, 70 per cent of world’s milk is more expensive than Indian milk. However, quality of milk produced in India falls below the internationally accepted standards. Development of awareness, mindset and commitment on improving the quality of milk is necessary. Milk Production of the India’s leading milk producing states State 000 tonnes LPD LLPD Contribution 2008-09 Daily Daily % All India 108465 297164384 2971.6 100.0% Uttar Pradesh 19537 53526027 535.3 18.0% Andhra Pradesh 9570 26219178 262.2 8.8% Rajasthan 9491 26002740 260.0 8.8%

- 2. Punjab 9387 25717808 257.2 8.7% Gujarat 8386 22975342 229.8 7.7% Source – Animal Husbandry Department We need to use data pertaining to same time period and not for time difference more than 2 – 3 years.

- 3. - Current Demand and Supply Situation Demand Scenario Despite being the largest milk producer in the world, per capita availability and consumption of milk in India is still relatively low, although it is high by developing country standards. The per capita availability of milk reached about 232 grams per day in 2004/05. Between There is, however, considerable variation in consumption of milk across income classes and a strong positive association between quantity of milk consumed and income level. Several factors have contributed to the increased demand for milk and dairy products in the country, including the strong cultural significance of milk in India where a large proportion of the population is lacto-vegetarian. The demand for milk and dairy products is income elastic; growth in per capita income is expected to increase demand for milk and milk products. Urbanization and changing food habits and lifestyles have also reinforced growth in demand for dairy products. Further, per capita consumption of milk is 1.5-times higher among urban households than rural households. Nevertheless, the per capita consumption of milk has been increasing faster in the rural areas. Between 1983 and 1999, consumption of milk increased by 71% in rural households and 63% in urban households. This suggests that, although urbanization would remain a key driver of demand, sustained growth in rural incomes would fuel rapid growth in rural demand for livestock products. In 1999/2000 livestock products accounted for 12.9% of the total household consumption expenditure of rural households. This is slightly higher than that of urban households (12.6%). In rural areas, the share of livestock products increased from 11.0% in 1983,

- 4. to 13.1% in 1987/88 and to 13.9% in 1993/94, and then slightly declined to 12.9%. In urban areas, however, it increased slightly during 1980s, but declined during 1990s. Both the rural and urban consumers spent about 70% of the total allocation to livestock products on milk and dairy products. Given the relatively high income elasticity, the demand for milk and dairy products is expected to grow rapidly. Supply Scenario The Indian dairy industry underwent substantial growth during the 1980s and 1990s: production of milk increased from 32 million tonnestones in 1980/81 to 91 million tonnes in 2004/05. Buffalo and cow are both important dairy species with a share of 55% and 43%, respectively, in total milk output; goats account for most of the rest. Growth in total milk production, however, has decelerated marginally from 5.3% during 1980s to 3.95% from 1990-2004. The deceleration has been observed in the case of both cow and buffalo milk production. This rapid and sustained growth in milk heralded the country into an era of self-sufficiency towards the late 1990s; dependence on imports reduced considerably. This has not only made India the number one milk producer in the world, but also represents sustained growth in the availability of milk and milk products for the burgeoning population of the country. The per capita availability of milk has also increased to a level of about 232 grams per day; this is still low as compared to most developed nations or the world average of 285 grams per day, but is high compared to most developing countries. However, throughout all of this period, the informal traditional sector has dominated and continues to play by far the largest role in the market, with a share of over 80% in the total market of milk and milk products. - Gap and time it is likely to take to meet the gap - Who are we and why are we doing this? Samridhi Agri Products Private Limited (SAPPL) is a registered company under the Companies Act, 1956 and was formed on 11 Dec 2009. SAPPL is an initiative of young likeminded, professionally qualified people having rich experience in diversified sectors. Did we want to do this even without Sanchetna also or not? What happens if Sanchetna is not there?

- 5. Samridhi is in the field of providing credit plus activities to the members of Sanchetna Financial Services, a Microfinance Institution working in the rural areas across five districts surrounding Lucknow. Having a common set of promoters for both Sanchetna and Samridhi, there is a good amount of synergy between the two which in turn is benefiting the villages where both companies operate. The mandate of the organization is to procure 1, 00,000 litres of milk from over 30,000 milk producers in the next three years. Samridhi will strive to reach at least 70 % of the areas in which Sanchetna is working. The objective of the organisation is to get into the value chain of the economic activities carried out by the populace of rural India and benefit the members and potential members of SFSPL. - Whom we want to serve and where Dairying seems to promote gender and social equity: 58% of the total workers engaged in the dairying sub-sector are women, although in urban areas it is only 37%. The participation of women in other activities, including agriculture, is low compared to that in animal husbandry, particularly dairying. Further, the majority of dairy workers belong to socially and economically disadvantaged communities: Scheduled Tribes (STs), Scheduled Castes (SCs) and Other Backward Castes (OBCs) together constitute about 69% of the persons employed in dairy sector (Table 19). Further, about 92% of workers in the dairy industry are engaged in farming and allied activities pertaining to primary production, including cattle rearing, goat rearing for milk production, breeding, ranching and grazing. It is widely accepted by various studies that the livestock sector provides much higher employment and more regular income than any other agricultural or allied activity. - How we want to do this? - there is too much of operational details here. We will have to prune it further and make it high level Having been in the business for over a year and half, the company has so far experienced two lean seasons. The company started its Village Level Collection (VLC) centres by appointing a Sanchalak from the village. The Sanchalak was paid a minimum salary and was incentivized on the quantity of milk procured. The company provided the complete testing equipments along with the Gerber Machine to the Sanchalak. The Sanchalak did the testing for all the farmers pouring milk in the VLC. The company’s milk van collected the milk from the Sanchalak’s doorstep. The payments were made on a weekly basis. The payments made to the farmers were based on the challans given by the Sanchalaks. The model had a few shortcomings which were reflected from the lower margins earned by Samridhi.

- 6. The reason for this was that the Sanchalak being the intermediary between the farmer and the company started manipulating the quality readings leading to a losses for both the farmers and Samridhi. The company has made a few changes in the model recently where the Sanchalaks have been replaced by the company’s own employee. The person responsible for procurement looks after the procurement in 3 villages. Each village is assigned a fixed time in which the villagers are expected to come and pour their milk. This way now we have full control over the quality and the company has more or less minimized the difference in the purchase price and the price realized while selling. As far as the infrastructure is concerned, the company has installed a Bulk Milk Cooler (BMC) with a storage capacity of 1160 litres. The BMC has been installed within a radius of 15 kilometers from the VLCs. This way the bacterial growth in the milk is being minimized. The company has a Tata Ace which is used for collecting the milk from the villages. The company has signed an MOU with a local dairy plant who procures the entire - What we want to achieve With Sanchetna having over 25% of its clientele involved in dairy activities, Samridhi started its first village collection centre on 12th April, 2010. At present the company has a presence in 9 villages near Dewa Sharif town in Barabanki district with over 140 farmers as its customers. Samridhi aims to open a total of 20 VLCs and benefit over 500 milk producers by the end of this calendar year. - What is in it for investors? 2. Current Market - Demand for liquid milk - Supply for milk

- 7. - Factors of production - Reasons for slow growth 3. Who we are - Background - Team Details - Reasons for doing this – Business Potential and Social Good - What makes it work for us

- 8. Lean and mean Ops structure The model has been tested, tweaked and is easily scalable - Will be able to pull it off The entry of newer and bigger players such as Mother Dairy, Paras, Namaste India, etc will reduce our dependability on one source of supply. Also the competition will help in fetching better prices for our farmers leading to an increase in procurement. Since we have learnt from our mistakes, we are better prepared for facing the future. 4. Market Segmentation - Who is our target market – production as well as supply side - Which geography we want to target and why? Currently focus on Barabanki and then spread to surrounding districts wherever Sanchetna is operating - What advantages we have? Synergy with Sanchetna, especially its cattle loans which is leading to an increase in the bovine population in the region Tried and tested model Vintage and having survived two lean seasons Experienced and qualified set of promoters and management 5. Strategy and Products - How do we reach out to? - What services do we provide and with what set-up? - Manpower requirements - Infrastructure requirements - Expansion strategy 6. What we want to achieve - How many - By when

- 9. - Revenue projections - Assumptions 7. Projected financials - Financial statements - Details about structure - ROE 8. SWOT SWOT Analysis Table 1: Strengths and Weaknesses of SFSPL Internal Environment Strengths: Weaknesses/Areas for Improvement: 1. Symbiotic relationship with Sanchetna 1 Institutionalisation of Standard Processes Financial Services Private Limited. 2 Limited financial resources 2. Young and professional management team 3 Developing internal control systems for rapid with diverse background scale up and growth 3. Infusion of own equity, gives flexibility of 4 Dependency on single dairy player (source of control. milk supply) 4. Clarity of vision among the senior management and staff 5. Survived two lean seasons leading to enhanced credibility in the villages 6. Timely and Better than market prices given to farmers 7. Transparent pricing method based on scientific milk testing in the villages External Environment Opportunity: Threat: 1. Entry of national players such as Mother 1. Perish ability of milk Dairy, Paras, etc. Will open more 2. Seasonal Fluctuations opportunities 3. Long marriage seasons leading to lesser 2. Lean and mean Ops structure procurement 9. Competitive Advantages 10. Risk Mitigation 11. Competition

- 10. The Markets that Samridhi is in is quite competitive as a lot of small and marginal players dominate the scene but if we closely study the value chain of Milk products, we find a lot of inefficiency created due to following two factors: a) No communication between the actual consumer and the producer b) Distance between the actual place of consumption and actual place of production. Organisations operating in this space easily command a minimum margin of close to 20-30 percent. The toughest entry barrier for a new player is to fight the perishable nature of the product which needs to be processed at the earliest. Value additions of various kinds also increase the shelf life of the various dairy products. We are currently supplying our entire milk to a national level dairy player who has a plant with capacity of1.25 lac litres per day. The company has entered into a formal agreement with the dairy plant and has also signed a MOU for the same. We have completion from the following: a) PARAG ( Pradashik Co-operative Dairy Federation) b) Mother Dairy (procuring milk in nearby districts) c) Few organized local players such as Gyan, Namaste India, Singhania, Sudama, etc. d) Presence of a strong network of dudhias belonging to a community involved in milk business for centuries e) Local Dairies sourcing milk from through VLC model f) Presence of people involved in producing khoa and other dairy items in the villages At present we are present in only few villages (9) and hence we are yet to get noticed by the above competitors, though in we have already built a significant amount of goodwill in our areas of operations.