The computer story an armchair researcher's view

•

1 j'aime•423 vues

Despite being a “high-tech” industry, the Law of Diminishing Return to Scale hold good for the computer Industry. As industry has matured and efficiency seems to have peaked for traditional computers, we see big firms facing margin decline, resulting into major industry shakeouts. This is also, perhaps, the primary reason that caused IBM exit personal computer market. Merger of HP and Compaq and more recently HP’s plan to exit PC industry (though it did not finally) could also be attributed to this (to a great extent). Industry has been commoditized to a great extent and firms are struggling to create value proposition to charge any premium.

Recommandé

Contenu connexe

Dernier

Dernier (20)

En vedette

En vedette (20)

The computer story an armchair researcher's view

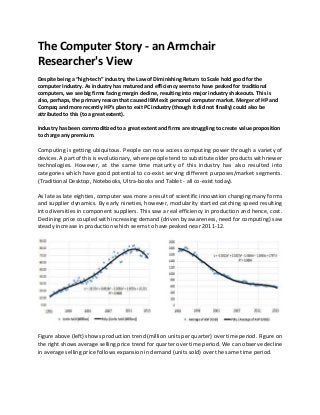

- 1. The Computer Story - an Armchair Researcher's View Despite being a “high-tech” industry, the Law of Diminishing Return to Scale hold good for the computer Industry. As industry has matured and efficiency seems to have peaked for traditional computers, we see big firms facing margin decline, resulting into major industry shakeouts. This is also, perhaps, the primary reason that caused IBM exit personal computer market. Merger of HP and Compaq and more recently HP’s plan to exit PC industry (though it did not finally) could also be attributed to this (to a great extent). Industry has been commoditized to a great extent and firms are struggling to create value proposition to charge any premium. Computing is getting ubiquitous. People can now access computing power through a variety of devices. A part of this is evolutionary, where people tend to substitute older products with newer technologies. However, at the same time maturity of this industry has also resulted into categories which have good potential to co-exist serving different purposes/market segments. (Traditional Desktop, Notebooks, Ultra-books and Tablet - all co-exist today). As late as late eighties, computer was more a result of scientific innovation changing many forms and supplier dynamics. By early nineties, however, modularity started catching speed resulting into diversities in component suppliers. This saw a real efficiency in production and hence, cost. Declining price coupled with increasing demand (driven by awareness, need for computing) saw steady increase in production which seems to have peaked near 2011-12. Figure above (left) shows production trend (million units per quarter) over time period. Figure on the right shows average selling price trend for quarter over time period. We can observe decline in average selling price follows expansion in demand (units sold) over the same time period.

- 2. Desktop PC – Computing initially became personal (current form) by introduction of desktop PC. Pace of market expansion (indicated by quantity sold) was slow but cost efficiency (indicated by average selling price) happened at relatively faster pace. Notebook PC – As opposed to Desktop, which is fixed at a place; Notebook added mobility to computer. This was quite an innovation with potential to make computer ubiquitous. However, it saw initial lower adoption due to high price and also due to lower awareness of PC in general. Desktop and Notebook anyway was initially targeted at different user segments and was expected to co-exist. However, as price of notebooks continued declining due to decline in cost of components and efficiency driven by modularity and production shifting to lower cost locations; demand for this surged at a very fast pace. This phase was also significantly supported by increase in computer literacy and demand for notebook for services oriented organizations. Substitution – Between Desktop and Notebook: - Figure below shows trend of notebook and desktop units sold over a period of time. We can clearly see catch up between these two.

- 3. This phase was, also, significantly supported by increase in computer literacy and demand for notebook for services oriented organizations. It is interesting to note here that initially there was huge difference between average selling price of Notebooks and Desktops and consequently (it appears) Notebook sales growth was quite less compared to desktop. In the later part (around 2008 and later) the gap between ASP of Notebook and Desktop narrowed to a great extent and, at the same time period, we can notice sales of notebook surpassing that of desktop. This seems to be a case of substitution where, within a comparable price level, people tend to substitute Desktop with Notebooks. Evolution of computing product portfolio: - Substitution and Co-Existence We checked this by adding another next generation technology (Ultra-Slim Notebooks) to the analysis. Ultra-Slim notebook uses SSD (solid state drive) compared to usual HDD (Hard Disk Drive) used in traditional Desktops and Notebooks. SSD is takes much less space and energy compared to HDD and this makes the form factor Ultra-Slim. This has added another engine to growth of PC

- 4. market. As it’s a new technology, we started noticing sales of Ultra-Book post year 2008. As with most of the new technology, initially it was priced much higher than both Desktop and Notebook. As a result (it appears) it witnessed slower adoption and growth till average selling price was brought down to narrow the gap and drive adoption. Looking at figures above (sales of Desktop, Notebook and Ultra-Slim Notebooks) and tallying this with figure below (average selling price of Desktop, Notebook and Ultra-Slim Notebooks) we observe that, substitution of PC (convergence of Desktop, Notebooks and Ultra-Slim Notebook) were accelerated as price difference narrowed (post year 2012) Despite being a “high-tech” industry, the Law of Diminishing Return to Scale hold good for the computer Industry. Smaller firms grow faster than the larger firms until they attain a size after which it is not possible to improve efficiency any further. However, this is truer for hardware firms than software firms. In fact the trend is reverse for software firms – after attaining a threshold size software firms grow with increase in size.

- 5. Fast commoditizing market and customers’ acceptance/adoption of common/open standard, have made radical innovation unattractive for manufacturers. Hence PC makers are pushed to incremental innovation by component makers who introduce frequent changes in their products (faster speed, greater capacity, smaller form factor, longer life) in efforts to gain greater market share within their industry sector such as semiconductors, storage or power supply. As a result, PC makers have tended to concentrate on operational efficiency, marketing, and distribution, rather than trying to use product differentiation as a source of sustainable competitive advantage. Moreover, the effect of these factors has led to a consolidation in the computer industry, with the largest firms becoming bigger. Prakash Kumar