2013-14 Budget Expectations for Auto, Oil & Gas, Power and Banking Sectors

•Télécharger en tant que PPT, PDF•

0 j'aime•226 vues

Union budget 2013-14 expectations Pushkaraj Jamsandekar MMS - Finance Contact - +09869139507 Email - pushkarajjamsandekar@yahoo.com Perception Research & Advisory (Grey Research)

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (20)

En vedette

Similaire à 2013-14 Budget Expectations for Auto, Oil & Gas, Power and Banking Sectors

Similaire à 2013-14 Budget Expectations for Auto, Oil & Gas, Power and Banking Sectors (20)

2013-14 Budget Expectations for Auto, Oil & Gas, Power and Banking Sectors

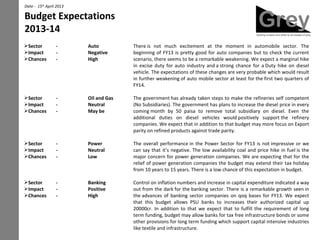

- 1. Date - 15th April 2013 Budget Expectations 2013-14 Sector Impact Chances - Auto Negative High There is not much excitement at the moment in automobile sector. The beginning of FY13 is pretty good for auto companies but to check the current scenario, there seems to be a remarkable weakening. We expect a marginal hike in excise duty for auto industry and a strong chance for a Duty hike on diesel vehicle. The expectations of these changes are very probable which would result in further weakening of auto mobile sector at least for the first two quarters of FY14. Sector Impact Chances - Oil and Gas Neutral May be The government has already taken steps to make the refineries self competent (No Subsidiaries). The government has plans to increase the diesel price in every coming month by 50 paisa to remove total subsidiary on diesel. Even the additional duties on diesel vehicles would positively support the refinery companies. We expect that in addition to that budget may more focus on Export parity on refined products against trade parity. Sector Impact Chances - Power Neutral Low The overall performance in the Power Sector for FY13 is not impressive or we can say that it’s negative. The low availability coal and price hike in fuel is the major concern for power generation companies. We are expecting that for the relief of power generation companies the budget may extend their tax holiday from 10 years to 15 years. There is a low chance of this expectation in budget. Sector Impact Chances - Banking Positive High Control on inflation numbers and increase in capital expenditure indicated a way out from the dark for the banking sector. There is a remarkable growth seen in the advances of banking sector companies on qoq bases for FY13. We expect that this budget allows PSU banks to increases their authorized capital up 20000cr. In addition to that we expect that to fulfill the requirement of long term funding, budget may allow banks for tax free infrastructure bonds or some other provisions for long term funding which support capital intensive industries like textile and infrastructure.

- 2. Sector Impact Chances - Infrastructure Positive High Pushkaraj Jamsandekar MMS - Finance Contact – +09869139507 Mail ID – pushkarajjamsandekar@yahoo.com Perception Research & Advisory Infrastructure, one of the widest concepts is broadly divided into two types. First, economic infrastructure and second is social infrastructure. The economic infrastructure broadly covers four major sectors -transportation (utility), power, telecom and water irrigation while, social infrastructure covers most important sector -The real estate and construction of judicial departments. The major concern of the companies which are working for these sectors are debt portion on their balance sheet. The drop in interest rate and positive budget for banking sector should definitely boost the infrastructure ahead. We expect some more tax relaxation on infrastructure sector and benefits for key driver of the sector.

- 3. Investment Criteria & Disclaimer Rating Low Risk Medium Risk High Risk Buy Over 15 % Over 20% Over 25% Accumulate 10 % to 15 % 15% to 20% 20% to 25% Hold 0% to 10 % 0% to 15% 0% to 20% Sell Negative Returns Negative Returns Negative Returns Risk Description Predictability of Earnings / Dividends / Price Volatility Low Risk High predictability / Low volatility Medium Risk Moderate predictability / volatility High Risk Low predictability / High volatility Company & Analyst Details Pushkaraj Jamsandekar Perception Research & Advisory (Grey Research) MMS - Finance Capital Market – Equity Investment Contact - +09869139507 perception.research@yahoo.com Email ID - pushkarajjamsandekar@yahoo.com https://www.facebook.com/pages/Grey-Research/475908969095732 Disclaimer This document is for private circulation and information purposes only and should not be regarded as an investment, taxation or legal advice. Investors should seek financial advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this publication and should under-stand that statements regarding future prospects may not be realized. In no circumstances it be used or considered as an offer to sale or a solicitation of any offer to buy or sell the securities mentioned in it. We and our affiliates, officers, directors and employees including persons involved in the preparation or issuance of this material may: (a) from time to time, have long or short positions in, and buy or sell the securities thereof, of company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) dis-cussed herein or act as an advisor or lender or borrower to such company or have other potential conflict of interest with respect to any recommendation and re-lated information and opinions. The information contained in this publication may have been taken from trade and statistical services and other sources, which we believe are reliable. We does not guarantee that such information is accurate or complete and it should not be relied upon as such. Any opinion ex-pressed reflects judgments at this date and are subject to change without notice. Caution: Risk of loss in trading & investment can be substantial. You should carefully consider whether trading & investment is appropriate for you in light of your experience, objectives, financial resources and other relevant circumstances. Source: Perception Research