Recommandé

Contenu connexe

Tendances

Tendances (10)

En vedette

En vedette (11)

Dernier

Dernier (20)

Working Capital Management is King

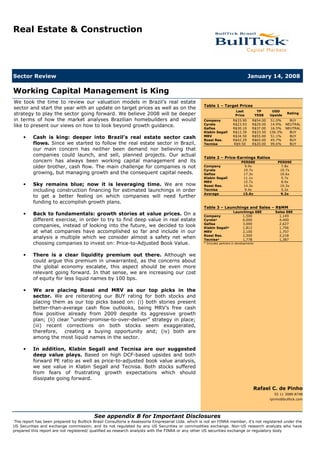

- 1. Real Estate & Construction Sector Review January 14, 2008 Working Capital Management is King We took the time to review our valuation models in Brazil’s real estate Table 1 – Target Prices sector and start the year with an update on target prices as well as on the Last TP USD strategy to play the sector going forward. We believe 2008 will be deeper Rating Price YE08 Upside in terms of how the market analyses Brazilian homebuilders and would R$33.90 R$54.00 51.0% BUY Company R$23.93 R$29.00 14.9% NEUTRAL Cyrela like to present our views on how to look beyond growth guidance. R$30.10 R$37.00 16.5% NEUTRAL Gafisa R$12.39 R$33.50 156.3% BUY Klabin Segall R$34.50 R$55.00 51.1% BUY MRV Cash is king: deeper into Brazil’s real estate sector cash • R$42.29 R$65.00 45.7% BUY Rossi Res. flows. Since we started to follow the real estate sector in Brazil, R$9.50 R$20.00 99.6% BUY Tecnisa our main concern has neither been demand nor believing that companies could launch, and sell, planned projects. Our actual Table 2 – Price-Earnings Ratios concern has always been working capital management and its PER08E PER09E older brother, cash flow. The main challenge for companies is not 9.9x 7.8x Company 19.7x 10.7x Cyrela growing, but managing growth and the consequent capital needs. 17.3x 10.6x Gafisa 11.1x 5.7x Klabin Segall 15.7x 8.9x MRV Sky remains blue; now it is leveraging time. We are now • 14.3x 10.3x Rossi Res. including construction financing for estimated launchings in order 9.4x 5.2x Tecnisa Average 15.6x 9.2x to get a better feeling on which companies will need further funding to accomplish growth plans. Table 3 – Launchings and Sales – R$MM Launchings 08E Sales 08E Back to fundamentals: growth stories at value prices. On a • 1,500 1,149 Company different exercise, in order to try to find deep value in real estate 6,000 4,400 Cyrela* 3,000 2,627 Gafisa companies, instead of looking into the future, we decided to look 1,812 1,706 Klabin Segall* at what companies have accomplished so far and include in our 2,100 1,707 MRV 2,500 2,218 Rossi Res. analysis a multiple which we consider almost a safety net when 1,778 1,387 Tecnisa* choosing companies to invest on: Price-to-Adjusted Book Value. * Includes partners in developments There is a clear liquidity premium out there. Although we • could argue this premium in unwarranted, as the concerns about the global economy escalate, this aspect should be even more relevant going forward. In that sense, we are increasing our cost of equity for less liquid names by 100 bps. We are placing Rossi and MRV as our top picks in the • sector. We are reiterating our BUY rating for both stocks and placing them as our top picks based on: (i) both stories present better-than-average cash flow outlooks, being MRV’s free cash flow positive already from 2009 despite its aggressive growth plan; (ii) clear “under-promise-to-over-deliver” strategy in place; (iii) recent corrections on both stocks seem exaggerated, therefore, creating a buying opportunity and; (iv) both are among the most liquid names in the sector. In addition, Klabin Segall and Tecnisa are our suggested • deep value plays. Based on high DCF-based upsides and both forward PE ratio as well as price-to-adjusted book value analysis, we see value in Klabin Segall and Tecnisa. Both stocks suffered from fears of frustrating growth expectations which should dissipate going forward. Rafael C. de Pinho 55 11 3089-8748 rpinho@bulltick.com See appendix B for Important Disclosures This report has been prepared by Bulltick Brasil Consultoria e Assessoria Empresarial Ltda. which is not an FINRA member, it’s not registered under the US Securities and exchange commission, and its not regulated by any US Securities or commodities exchange. Non-US research analysts who have prepared this report are not registered/ qualified as research analysts with the FINRA or any other US securities exchange or regulatory body

- 2. Cash is king: deeper into Brazil’s real estate sector cash flows Since we started to follow the real estate sector in Brazil, our main concern has neither Our main concern regarding been demand nor believing that companies could launch, and sell, planned projects. Our the real estate sector has always been working capital actual concern has always been working capital management and its older brother, cash management. flow. The main challenge for companies is not growing, but managing growth and the consequent capital needs. As shown on Exhibit 1, typical working capital exposure to an average project should hover between 20-30% of a project’s potential sales value (PSV). This is only possible due to the use of construction financing, which allows companies to finance on average 70% of the cost of the building. So far, the return on newly developed projects has been quite high on an IRR or NPV perspective. However, this return is only assured by the project delivery, which is tied to managing correctly the cash flow. Exhibit 1: Typical project cash exposure with SFH financing Considering construction Potential Sales Value (PSV) 100,000 financing, typical cash flow Gross Margin 40% exposure should hover Total Cost (60,000) between 20-30% of a project’s PSV. Land Cost (15% of PSV) (A) (15,000) Building Costs (45,000) SFH Financing = 70% of Building Costs 31,500 Building Cash Exposure (B) (13,500) Total Cash Exposure (A) + (B) (28,500) Source: Bulltick Our cash flow exposure exercise depends on the companies being able to get financing to reduce their own cash exposure to projects. A substantial stake of the capital Brazilian banks are obliged to invest in real estate projects goes in the form of construction financing. On Exhibit 2, we show the difference between a typical project cash flow leveraged by construction financing and another one without the line. Exhibit 2: Typical project cash flows, SFH financing impact 45% Cash Exposure as % of PSV 30% 15% 0% 1Q 2Q 3Q 4Q 5Q 6Q 7Q 8Q 9Q 10Q 11Q 12Q -15% -30% -45% -60% With SFH leverage Without SFH leverage Source: Bulltick Until now, the outlook for the Brazilian macroeconomic scenario suggests that the growth As we assume the growth cycle for homebuilders is cycle for homebuilders is sustainable. This opinion seems to be shared by the companies sustainable, we included in the sector: the average growth in launchings estimates by company managements is construction financing in around 30% per year for the 2009-07 period. our models… 2

- 3. Given this scenario, we have decided to include in our models the construction financing …allowing us to better evaluate those companies in for projects within the SFH scope in order to better evaluate those companies in which which extra funding should extra cash will be needed to meet guidance going forward. If the financing conditions for be needed, given current real estate projects are unchanged, some of these companies may attempt to raise cash market conditions. either through debt or equity issues. In the case of equity issues, the potential EPS dilution for shareholders is a concern. Exhibit 3: Free cash flow-to-equity, 2008-2012 Cash Position Free Cash Flows-to-Equity Company (R$ MM) 2008 2009 2010 2011 2012 Cyrela 800 (68) (1,225) (2,174) (2,678) 843 Tecnisa 156 (237) (419) (420) (237) 319 Klabin Segall* 238 37 (209) (222) 83 195 Rossi Residencial 377 (221) 74 (88) (161) 210 Company 128 (196) (379) (231) (234) 4 MRV 882 (164) 69 345 565 720 Gafisa 372 (447) (264) 309 327 410 Source: Bulltick * Cash adjusted for recently issued debentures Back to fundamentals: growth stories at value prices On a different exercise, in order to try to find deep value in real estate companies, We included Price-to- instead of looking into the future, we decided to look at what companies have Adjusted Book Value accomplished so far and include in our analysis a multiple which we consider almost a multiples to our analysis in safety net when choosing companies to invest on: Price-to-Adjusted Book Value. order to find deep value plays. As the accounting for homebuilders does not help much our analysis, distorting financial statements, especially given the high growth experienced over the last 2 years, we have decided to make a simple adjustment to reported book value for the companies: we added the backlog profits. The recognition of such profits is dependable only on building and delivery. At this point, we think it is fair to assume sold apartments will be delivered. Below, we present a table including the price-to-adjusted book value multiples for companies under our coverage. Exhibit 4: Adjusted price-to-book values R$ Millions, unless noted Company Cyrela Gafisa Klabin MRV Rossi Tecnisa Average/Sum Market Cap 1,221 8,511 3,867 731 4,666 3,335 1,381 23,710 3Q07 Reported Book Value 328 1,994 1,493 400 1,339 1,177 735 7,466 Price / Book 3.73x 4.27x 2.59x 1.83x 3.49x 2.83x 1.88x 3.18x Premium / Discount to Average 17.3% 34.4% -18.5% -42.5% 9.7% -10.8% -40.8% Backlog Revenues to recognize 337 2,099 1,209 386 327 853 150 5,361 Cost to recognize (206) (1,202) (744) (257) (145) (546) (92) (3,192) Gross Profit to recognize 131 897 466 128 181 307 58 2,169 Net Profits to recognize 101 698 356 89 144 247 46 1,680 428 2,692 1,850 489 1,483 1,424 781 9,146 Adjusted Book Value - Backlog Profits Price / Adj. Book Value 2.85x 3.16x 2.09x 1.50x 3.15x 2.34x 1.77x 2.59x Source: Bulltick As with PE ratios, Price-to-Book value analysis in real estate also shows some inconsistency. First, we assume that the average project return between different companies is similar. In addition, we remind investors that entry barriers in real estate are relatively low, thus, exaggerated premiums are not sustainable in the long run, even when a liquidity premium/discount is considered. For investors looking to buy value in the sector, departing from price-to-adjusted book Departing from this simple value, companies like Klabin Segall and Tecnisa call our attention, especially when this metric, Klabin Segall and analysis is coupled with SFH financing analysis and with forward PE multiples. Tecnisa call our attention. 3

- 4. Exhibit 5: Price-to-Earnings 2009E 12.0x Even when considering a 10.7x 10.6x liquidity premium/discount, 10.3x if the average project return 10.0x 9.2x is similar and entry barriers 8.9x are inexistent, a 105% gap between the extremes in 7.8x 8.0x our PER09E multiples range seem exaggerated to us. 5.7x 6.0x 5.2x 4.0x Tecnisa Klabin Company MRV Average Rossi Gafisa Cyrela Source: Bulltick Exhibit 6: PE-to-growth multiples – 2009E 0.30x 0.26x 0.25x 0.25x 0.22x 0.20x 0.15x 0.14x 0.15x 0.10x 0.07x 0.06x 0.05x 0.05x 0.00x Tecnisa Klabin MRV Gafisa Company Rossi Average Cyrela Source: Bulltick 4

- 5. Company Outlooks Rossi Residencial: TP-YE08 R$65.00, 45.7% upside potential in USD As a consequence of one of the best cash flow outlooks going forward, we are placing Rossi among our top picks in the sector, being the company our preferred name among the most liquid stocks in the sector. We are raising our TP to R$65.00 from R$59.00 on the back of higher launching estimates, to which working capital needs are almost completely funded by construction financing. The stock’s recent 13% correction, which we perceive as linked to fears of an upcoming follow-on offer by Rossi after Cyrela’s equity issue announcement, was unjustified. However, should such a deal come up, investors should note the proceeds will probably be invested in new projects, thus, with expectation to create value. We currently see Rossi trading at a 10.3x PER09E vs. our average of 9.2x for the sector. On top of being one of the most liquid names in the sector, and having a proven track record as well as fair future cash flow outlook, we believe the stock deserves some premium to both Cyrela and Gafisa. Exhibit 7: Rossi’s Main Figures Rossi Res. (R$ MM) 2006 2007E 2008E 2009E 2010E 2011E 2012E Launchings 882 1,981 2,500 3,000 3,360 3,696 3,844 - Real Estate Sales 584 1,284 2,218 2,571 3,096 3,466 3,704 Net Revenues 411 701 1,380 1,998 2,565 3,075 3,474 Adj. EBITDA 61 137 297 464 626 753 851 Adj. Net income 54 137 233 325 424 520 598 Gross Margin 31.2% 35.3% 35.5% 35.6% 34.8% 34.3% 34.0% Adj. EBITDA Margin 12.4% 19.6% 21.5% 23.2% 24.4% 24.5% 24.5% Adj. Net Margin 10.6% 19.6% 16.9% 16.3% 16.5% 16.9% 17.2% PER 62.0x 24.3x 14.3x 10.3x 7.9x 6.4x 5.6x FV/EBITDA 51.3x 25.5x 13.6x 10.2x 8.2x 7.2x 6.5x Adjusted for IPO costs Source: Rossi Residencial and Bulltick MRV: TP-YE08 R$55.00, 51.1% upside potential in USD We are also placing MRV among our top picks in the sector on the back of an interesting growth-adjusted valuation and, in our view, an attractive entry point created recently by the 20% drop in stock price since early December. We disagree with the criticisms out on the street about the company’s aggressive growth plans. As MRV benefits from the use of special credit lines targeted to low-income developers by Caixa Economica, the company enjoys a comfortable cash flow position going forward. MRV shares currently trade at a 8.9x PER09E, a 7% discount over the first-tier group composed by Rossi, Cyrela and Gafisa. On a growth-adjusted basis, MRV trades at PE09- to-growth of 0.07x versus an average of 0.25x for Brazilian homebuilders. We reiterate our positive view on the company and on the quality of its management, which has potential to surprise the market going forward not only by over-delivering results but also due to its search for innovative credit solutions to its clients. For example, 5

- 6. MRV recently led the pack in signing a MOU with Caixa Economica in order to gain scale in low-income credit approval and grant financing for 12,000 units in 2008, a move quickly followed by its competitors. Main changes to our model were the inclusion of the revised launching estimates for 2008 and 2009 and modeling of the SFH financing. Besides, as this report was being written, we had to stop the press in order to account for the fact that the company beat its 2007 estimates. Our DCF-model points to a Dec 08 TP of R$55.00/share, implying a 51.1% potential upside in USD and therefore a BUY rating for the stock. Exhibit 8: MRV’s main figures MRV (R$ MM) 2006 2007E 2008E 2009E 2010E 2011E 2012E Launchings 337 1,200 2,100 2,520 2,898 3,130 3,318 - Real Estate Sales 206 717 1,707 2,298 2,705 3,001 3,220 Net Revenues 140 399 1,046 1,811 2,371 2,745 3,019 Adj. EBITDA 22 100 291 579 762 886 960 Adj. Net income 17 114 297 523 685 792 855 Gross Margin 35% 40% 43% 43% 42% 41% 40% Adj. EBITDA Margin 16% 25% 28% 32% 32% 32% 32% Adj. Net Margin 12% 29% 28% 29% 29% 29% 28% PER 274.2x 87.7x 15.7x 8.9x 6.8x 5.9x 5.5x FV/EBITDA 209.8x 102.3x 16.3x 8.2x 6.3x 5.5x 5.1x Adjusted for IPO costs Source: MRV and Bulltick Cyrela: TP-YE08 R$30.00, 14.9% upside potential in USD After incorporating the most recent launchings guidance and including the SFH leverage into our model, we are increasing our YE08 TP to R$29.00/share from R$26.00/share and downgrading Cyrela to NEUTRAL from BUY. At this point we prefer to take a more cautious stance concerning Cyrela, based on our estimates for the company’s cash flow for the coming years. Despite having a substantial amount of receivables, which could offset its funding needs, our analysis suggests that the company should direct most of the resources from recently announced debt and equity issues to comply with the working capital needs for the intended R$13.5 billion in launchings over 2008 and 2009. Besides the working capital management factor, the overhang created by the new equity issue announcement, the third since September 2005, reinforce our view. We see Cyrela shares, currently trading at 10.7x PER09E, at premium to both Rossi and Gafisa. However, at this point we believe Rossi deserves a premium over Cyrela as it is in better shape to face its working capital needs going forward. 6

- 7. Exhibit 9: Cyrela’s Main Figures Cyrela (R$MM) 2006 2007E 2008E 2009E 2010E 2011E 2012E Launchings 3,618 4,600 6,000 7,500 8,400 9,240 9,610 - Real Estate Sales 2,247 3,400 4,400 6,053 7,424 8,382 9,097 Net Revenues 1,064 1,561 2,040 3,727 5,430 6,905 8,146 Adj. EBITDA 196 403 539 1,075 1,582 1,998 2,351 Adj. Net Income 190 330 431 796 1,220 1,589 1,856 Gross Margin 39.4% 42.1% 42.8% 42.5% 41.8% 41.1% 40.8% Adj. EBITDA Margin 18.4% 25.8% 26.4% 28.8% 29.1% 28.9% 28.9% Adj. Net Margin 17.8% 21.1% 21.1% 21.4% 22.5% 23.0% 22.8% PER 44.8x 19.3x 19.7x 10.7x 7.0x 5.4x 4.6x FV/EBITDA 41.2x 21.0x 17.0x 9.5x 6.5x 5.3x 4.5x Adjusted for non-recurring gains Source: Cyrela and Bulltick Gafisa: TP-YE08 R$37.00, 16.5% upside potential in USD Our revised TP of R$37.00/share for Gafisa, up 12% from our previous TP of R$33.00/share, is a result of increased launchings guidance and fine tuning to our model. Nonetheless, we are downgrading Gafisa shares to NEUTRAL from BUY on the back of the same conservative stance we applied to Cyrela. Our analysis indicates Gafisa should need between R$350-R$450 million in additional funding, besides leveraging through SFH construction financing, to provide for its working capital needs. Additionally, we are still waiting to see concrete results arising from the company’s new business lines Fit and Bairro Novo, added to Alphaville’s acquisition. We currently see Gafisa stocks trading at a 10.6x PER09E, 15% above the average of the companies under our coverage. Exhibit 10: Gafisa’s Main Figures Gafisa (R$MM) 2006 2007E 2008E 2009E 2010E 2011E 2012E Launchings 1,005 1,900 3,000 3,360 3,695 3,846 3,999 - Real Estate Sales 995 1,625 2,627 3,086 3,505 3,729 3,908 Net Revenues 664 1,124 1,565 2,201 2,912 3,346 3,651 Adj. EBITDA 98 175 279 493 678 780 834 Adj. Net Income 76 122 225 368 495 575 613 Gross Margin 29.8% 30.4% 31.5% 32.3% 32.1% 31.7% 31.1% Adj. EBITDA Margin 14.8% 15.6% 17.8% 22.4% 23.3% 23.3% 22.8% Adj. Net Margin 11.4% 10.9% 14.4% 16.7% 17.0% 17.2% 16.8% PER 84.3x 42.2x 17.3x 10.6x 7.8x 6.7x 6.3x FV/EBITDA 57.3x 27.4x 15.6x 9.8x 7.4x 6.6x 6.3x Adjusted for IPO costs Source: Gafisa and Bulltick 7

- 8. Tecnisa: TP-YE08 R$20.00, 96.5% upside potential in USD Tecnisa stocks continue to be among the most discounted within our coverage universe. Against the market, the company was able to deliver 2007 launchings. This piece of news came out at the very end of the year and we believe it was overlooked by most of the market. The fact was also overshadowed by the pessimistic sentiment that has recently pushed market indices downward. As to the changes to our model, besides modeling of SFH construction financing, we incorporated the latest launchings guidance provided by the company. We also raised our discount rates to reflect the stock’s lower liquidity. Despite the higher discount rate, we still see the shares trading at a 52% discount to our Dec 08 target price of R$20.00/share. As described above, investing in Tecnisa is also attractive if we think in terms of P/ Adjusted Book Value ratio, trading at 1.77x vs. an average of 2.59x for the companies under our coverage. It is also important to mention that the company has a substantial amount of receivables which could help to cover the company’s capital needs. Therefore, we are maintaining our BUY rating for the stocks. Exhibit 11: Tecnisa’s Main Figures Tecnisa (R$ MM) 2006 2007E 2008E 2009E 2010E 2011E 2012E Launchings 369 1,364 1,778 2,235 2,504 2,601 2,705 - Real Estate Sales 333 706 1,387 1,877 2,270 2,476 2,618 Net Revenues 203 364 740 1,430 1,942 2,304 2,518 Adj. EBITDA 47 80 199 418 572 678 753 Adj. Net Income 36 88 146 265 380 491 546 Gross Margin 40.0% 38.6% 39.3% 39.0% 38.5% 38.2% 38.0% Adj. EBITDA Margin 23.1% 11.0% 26.9% 29.2% 29.4% 29.4% 29.9% Adj. Net Margin 17.6% 13.2% 19.8% 18.5% 19.6% 21.3% 21.7% PER 38.6x 15.8x 9.4x 5.2x 3.6x 2.8x 2.5x FV/EBITDA 32.4x 17.6x 8.6x 5.0x 3.8x 3.4x 3.2x Adjusted for IPO costs Source: Tecnisa and Bulltick Klabin Segall: TP-YE08 R$33.50, 148% upside potential in USD Among the less liquid names, Klabin Segall is the most discounted stock under our coverage universe. The company had its ups and downs to manage and deliver expected launchings growth during 2007 and we believe current prices more than reflect those issues. Nevertheless, we expect a more smooth string of launchings going forward, increasing results visibility, which we expect to translate in some share price recovery. Currently trading at 5.7x PER09E, a 38% discount to the sector average, stocks are attractive not only on a PER basis. Investors looking for deep value, the shares are also trading at almost without any premium to adjusted book value multiple, and 43% discounted to the sector average. In addition, we expect to see some more of the innovative projects Klabin Segall became known for executing successfully. For example, during 2008 and 2009 the company plans to develop an integrated complex of commercial and middle income residential project in Santo André, besides applying its revitalization experience to launch a 2nd home project in Buzios, Rio de Janiero state coast. We also look forward to see the initial results on the “Olá” low income initiative. Model review focused on increased launchings after Setin’s acquisition, including the construction financing and fine tunning. Besides, we are also raising our discount rates to 8

- 9. reflect lower liquidity for the shares. All in all, we reach a Dec. 08 TP of R$33.50/share, implying a 156% in USD and reiterating our BUY rating for the shares. Exhibit 12: Klabin Segall’s Main Figures Klabin Segall (R$ MM) 2006 2007E 2008E 2009E 2010E 2011E 2012E Launchings 773 1,775 1,812 2,084 2,334 2,567 2,670 - Real Estate Sales 400 875 1,706 1,832 2,199 2,358 2,535 Net Revenues 138 292 705 1,188 1,785 2,032 2,319 Adj. EBITDA 59 62 168 307 482 557 634 Adj. Net income 25 39 71 137 267 331 389 Gross Margin 41.9% 36.1% 36.5% 36.4% 36.2% 36.4% 36.1% Adj. EBITDA Margin 27.4% 21.4% 23.8% 25.8% 27.0% 27.4% 27.3% Adj. Net Margin 17.8% 13.5% 10.0% 11.6% 14.9% 16.3% 16.8% PER 206.0x 19.9x 11.1x 5.7x 2.9x 2.4x 2.0x FV/EBITDA 14.0x 13.8x 8.1x 5.5x 3.5x 3.1x 2.7x Adjusted for IPO Costs Source: Klabin Segall and Bulltick Company: TP-YE08 R$54.00, 48.2% upside potential in USD As part of our revision of Company’s valuation model, besides including higher launching guidance for ’08 and ’09, we analyzed carefully its working capital management, not only including SFH leverage but also the construction and sales speed curves. Company trades at a 7.8x PER09E versus Tecnisa’s and Klabin Segall’s respective 5.2x and 5.7x multiples and the average of 9.2x for homebuilders under our coverage. On a Price-to-Adj Book Value basis, Company negotiates at 2.85x, slightly above the 2.59x average for companies under our coverage. Company shares are currently trading at premium to Tecnisa and Klabin Segall, where we see more upside on a relative basis. Thus, despite a favorable valuation vis-à-vis the more liquid names, at this point, we prefer to look for deep value and stick to Tecnisa and Klabin Segall. Our DCF TP for Company is R$55.00/share for YE08. After roughly 21% decline in share prices since early December, we are upgrading Company to BUY from NEUTRAL. Exhibit 13: Company’s Main Figures Company (R$ MM) 2006 2007E 2008E 2009E 2010E 2011E 2012E Launchings 353 1,033 1,500 1,875 2,100 2,184 2,271 - Real Estate Sales 258 695 1,149 1,446 1,839 2,035 2,178 Net Revenues 289 451 742 997 1,442 1,806 2,064 Adj. EBITDA 69 90 166 233 327 398 439 Adj. Net income 56 64 123 157 230 281 311 Gross Margin 34.2% 30.7% 33.3% 34.4% 33.6% 33.0% 32.2% Adj. EBITDA Margin 20.4% 19.8% 22.4% 23.4% 22.7% 22.0% 21.3% Adj. Net Margin 15.8% 14.2% 16.6% 15.8% 15.9% 15.6% 15.1% PER 21.9x 19.0x 9.9x 7.8x 5.3x 4.3x 3.9x FV/EBITDA 17.8x 15.6x 9.8x 8.2x 6.1x 5.3x 4.9x Adjusted for IPO costs Source: Company and Bulltick 9

- 10. Detailed Financial Statements Rossi Residencial Income Statement (R$ MM) 2006 2007E 2008E 2009E 2010E 2011E 2012E Launchings 882 1,981 2,500 3,000 3,360 3,696 3,844 - Real Estate Sales 584 1,284 2,218 2,571 3,096 3,466 3,704 Gross Revenues 425 720 1,432 2,074 2,662 3,191 3,605 Net Revenues 411 701 1,380 1,998 2,565 3,075 3,474 - COGS (283) (454) (890) (1,286) (1,671) (2,021) (2,294) Gross Profit 128 247 490 712 894 1,054 1,180 - Sales Expeditures (46) (59) (117) (160) (180) (215) (243) - G&A Expenditures (38) (59) (85) (107) (111) (115) (120) - Other Operational 6 7 8 16 21 28 32 EBIT 50 136 296 462 624 751 848 Financial Results 47 24 (39) (104) (153) (173) (184) Non-Operational Results (52) (3,447) - - - - - EBT 46 157 256 357 471 577 664 Income Tax (2) (20) (23) (32) (47) (58) (66) Minority Interest - - - - - - - Net income 44 137 233 325 424 520 598 Depreciation 0.9 1.3 1.5 1.8 2.1 2.6 3.2 EBITDA 51 137 297 464 626 753 851 Adjustments 10 - - - - - - Adjusted EBITDA 61 137 297 464 626 753 851 Gross Margin 31.2% 35.3% 35.5% 35.6% 34.8% 34.3% 34.0% Adjusted EBITDA Margin 14.9% 19.6% 21.5% 23.2% 24.4% 24.5% 24.5% Adjusted Net Margin 13.1% 19.6% 16.9% 16.3% 16.5% 16.9% 17.2% Free Cash Flow 2006 2007E 2008E 2009E 2010E 2011E 2012E EBITDA 51 137 297 464 626 753 851 Taxes on EBIT (2) (18) (27) (42) (62) (75) (85) Change in Net Working Assets (408) (234) (917) (876) (870) (929) (489) CAPEX (2) (1) (2) (2) (3) (3) (4) FCFF (361) (115) (648) (456) (309) (254) 274 Change in Debt (14) 422 463 625 359 249 102 Emission 755 - - - - - - Financial Results 47 24 (39) (104) (153) (173) (184) Tax difference 0 (2) 4 9 15 17 18 FCFE 428 329 (221) 74 (88) (161) 210 Balance Sheet 2006 2007E 2008E 2009E 2010E 2011E 2012E Assets Cash and Equivalents 327 377 311 246 164 164 164 Accounts Receivable 392 353 1,107 1,550 2,001 2,601 2,855 Inventories 552 901 1,006 1,400 1,787 2,087 2,296 Other 220 537 468 644 632 433 560 Total Assets 1,490 2,168 2,892 3,840 4,583 5,285 5,875 Liabilities Short Term Debt 89 135 135 135 135 135 135 Clients Advance Payments 2 - - - - - - Long Term Debt 37 414 877 1,502 1,861 2,110 2,212 Other 283 445 531 610 677 739 779 Equity 1,080 1,174 1,349 1,593 1,911 2,301 2,749 Total Liabilities 1,490 2,168 2,892 3,840 4,583 5,285 5,875 Source: Rossi Residencial and Bulltick 10

- 11. MRV Income Statement (R$ MM) 2006 2007E 2008E 2009E 2010E 2011E 2012E Launchings 337 1,200 2,100 2,520 2,898 3,130 3,318 - Real Estate Sales 206 717 1,707 2,298 2,705 3,001 3,220 Gross Revenues 160 430 1,085 1,879 2,460 2,849 3,134 Net Revenues 140 399 1,046 1,811 2,371 2,745 3,019 - COGS (91) (240) (595) (1,036) (1,386) (1,619) (1,805) Gross Profit 50 159 450 775 984 1,126 1,214 - Sales Expeditures (11) (29) (98) (132) (156) (173) (185) - G&A Expenditures (24) (108) (62) (66) (69) (71) (72) - Other Operational 9 26 32 42 52 58 60 EBIT 24 48 322 619 812 941 1,017 Financial Results (3) 32 28 (3) (6) (9) (11) Non-Operational Results 0 0 - - - - - EBT 20 81 350 616 805 932 1,005 Income Tax (3) (28) (52) (92) (121) (140) (151) Minority Interest - (0) - - - - - Net income 17 53 297 523 685 792 855 Depreciation 0.2 0.8 1.4 2.0 2.3 2.6 2.9 EBITDA 22 39 291 579 762 886 960 Adjustments - 61 - - - - - Adjusted EBITDA 22 100 291 579 762 886 960 Gross Margin 35.3% 39.9% 43.1% 42.8% 41.5% 41.0% 40.2% Adjusted EBITDA Margin 16.0% 25.0% 27.9% 32.0% 32.1% 32.3% 31.8% Adjusted Net Margin 12.1% 28.5% 28.4% 28.9% 28.9% 28.8% 28.3% Free Cash Flow 2006 2007E 2008E 2009E 2010E 2011E 2012E EBITDA 22 39 291 579 762 886 960 Taxes on EBIT (4) (29) (48) (93) (122) (141) (153) Change in Net Working Assets (69) (553) (573) (436) (325) (198) (98) CAPEX (2) (5) (7) (4) (4) (5) (5) FCFF (52) (535) (337) 47 311 542 704 Change in Debt 63 (14) 149 25 39 30 25 Emission - 1,231 - - - - - Financial Results (12) (18) (12) (61) (79) (85) (94) Tax difference 1 1 (4) 0 1 1 2 FCFE (1) 666 (204) 11 272 489 637 Balance Sheet 2006 2007E 2008E 2009E 2010E 2011E 2012E Assets Cash and Equivalents 9 702 132 132 132 132 132 Accounts Receivable 129 493 1,003 1,197 1,413 1,509 1,543 Inventories 235 644 957 1,314 1,539 1,700 1,820 Other 7 107 580 656 948 1,418 2,015 Total Assets 380 1,945 2,672 3,299 4,032 4,758 5,509 Liabilities Short Term Debt 48 16 16 16 16 16 16 Clients Advance Payments 28 35 27 10 12 - - Long Term Debt 17 36 185 209 248 278 304 Other 197 479 842 1,069 1,246 1,361 1,446 Equity 91 1,380 1,603 1,996 2,509 3,103 3,744 Total Liabilities 380 1,945 2,672 3,299 4,032 4,758 5,509 Source: MRV and Bulltick 11

- 12. Cyrela Income Statement (R$ MM) 2006 2007E 2008E 2009E 2010E 2011E 2012E Launchings 3,618 4,600 6,000 7,500 8,400 9,240 9,610 - Real Estate Sales 2,247 3,400 4,400 6,053 7,424 8,382 9,097 Gross Revenues 1,104 1,625 2,117 3,868 5,635 7,167 8,455 Net Revenues 1,064 1,561 2,040 3,727 5,430 6,905 8,146 - C OGS (645) (904) (1,166) (2,142) (3,162) (4,069) (4,826) Gross Profit 419 657 873 1,584 2,268 2,836 3,320 - Sales Expeditures (131) (170) (204) (373) (543) (691) (815) - G&A Expenditures (73) (103) (125) (131) (136) (142) (147) - Management Fees (2) (2) (2) (2) (3) (3) (3) - Other Operational (18) 6 - - - - - EBIT 196 388 542 1,078 1,585 2,001 2,355 Financial Results 49 46 39 (51) (15) 44 33 - Financial Expenses (84) (102) (138) (186) (187) (194) (211) - Financial Revenues 133 149 177 135 172 237 244 Non-Operational Results - 0.1 - - - - - Equity Pick-Up - 110 - - - - - EBT 244 545 582 1,027 1,571 2,045 2,387 Income Tax (58) (57) (87) (123) (188) (245) (286) Employee Interest (5) (9) (5) (5) (5) (6) (6) Minority Interest (24) (39) (58) (103) (157) (204) (239) Net income 190 440 431 796 1,220 1,589 1,856 Depreciation 3.6 1.6 1.7 1.9 2.0 2.2 2.4 Amortization 1.5 - - - - - - Employee Interest (5) (9) (5) (5) (5) (6) (6) EBITDA 196 403 539 1,075 1,582 1,998 2,351 Adjustments 20.8 - - - - - - Adjusted EBITDA 217 403 539 1,075 1,582 1,998 2,351 Gross Margin 39.4% 42.1% 42.8% 42.5% 41.8% 41.1% 40.8% Ajudsted EBITDA Margin 20.4% 25.8% 26.4% 28.8% 29.1% 28.9% 28.9% Adjusted Net Margin 19.8% 21.1% 21.1% 21.4% 22.5% 23.0% 22.8% Free Cash Flow 2006 2007E 2008E 2009E 2010E 2011E 2012E EBITDA 196 403 539 1,075 1,582 1,998 2,351 Minority Adjustment (62) (118) (176) (339) (400) (391) (232) Taxes on EBIT (47) (40) (81) (129) (190) (240) (283) C hange in Net Working Assets (735) (1,223) (1,191) (2,388) (3,251) (4,298) (1,198) C APEX (39) (269) (3) (3) (3) (3) (4) FCFF (686) (1,247) (912) (1,784) (2,263) (2,936) 635 C hange in Debt (79) 509 810 604 101 219 179 Emission - - - - - - - Financial Results 49 46 39 (51) (15) 44 33 Tax difference (11) (17) (6) 6 2 (5) (4) FCFE (727) (709) (68) (1,225) (2,174) (2,678) 843 Balance Sheet 2006 2007E 2008E 2009E 2010E 2011E 2012E Assets C ash and Equivalents 561 671 785 399 363 363 363 Accounts Receivable 865 1,104 1,586 2,668 3,856 6,157 7,040 C lient Financing - 522 689 1,061 2,303 3,644 3,492 Inventories 976 1,696 2,306 3,447 4,432 5,262 5,830 Other 640 142 213 (96) (1,880) (4,321) (3,611) Total Assets 3,042 4,134 5,578 7,478 9,073 11,105 13,115 Liabilities Short Term Debt 57 86 86 86 86 86 86 Real Estate Acquisition Payables 351 758 891 1,067 1,195 1,314 1,367 C lients Advance Payments 84 35 7 - - - - Long Term Debt 67 548 1,358 1,962 2,064 2,283 2,462 Other 535 713 919 1,450 1,901 2,401 2,787 Equity 1,949 1,993 2,317 2,914 3,829 5,021 6,413 Total Liabilities 3,042 4,134 5,578 7,478 9,073 11,105 13,115 Source: Cyrela and Bulltick 12

- 13. Gafisa Income Statement (R$ MM) 2006 2007E 2008E 2009E 2010E 2011E 2012E Launchings 1,005 1,900 3,000 3,360 3,695 3,846 3,999 - Real Estate Sales 995 1,625 2,627 3,086 3,505 3,729 3,908 Gross Revenues 744 1,192 1,665 2,342 3,098 3,560 3,884 Net Revenues 664 1,124 1,565 2,201 2,912 3,346 3,651 - C OGS (466) (782) (1,071) (1,491) (1,978) (2,286) (2,517) Gross Profit 198 342 494 710 934 1,061 1,134 - Sales Expeditures (52) (71) (110) (110) (146) (167) (183) - G&A Expenditures (52) (103) (117) (122) (127) (132) (137) - Other Operational (30) (38) - - - - - EBIT 64 130 267 479 661 762 815 Financial Results (12) (18) (12) (61) (79) (85) (94) - Financial Expenses (65) (62) (31) (74) (92) (97) (106) - Financial Revenues 53 44 19 14 13 13 12 Non-Operational Results - - - - - - - EBT 52 112 255 418 582 677 721 Income Tax (6) (14) (31) (50) (87) (102) (108) Minority Interest - (6) - - - - - Net income 46 92 225 368 495 575 613 Depreciation 4.3 14.7 12.0 14.6 16.9 18.1 18.8 EBITDA 68 145 279 493 678 780 834 Adjustments 30 30.2 - - - - - Adjusted EBITDA 98 175 279 493 678 780 834 Gross Margin 29.8% 30.4% 31.5% 32.3% 32.1% 31.7% 31.1% Adjusted EBITDA Margin 14.8% 15.6% 17.8% 22.4% 23.3% 23.3% 22.8% Adjusted Net Margin 11.4% 10.9% 14.4% 16.7% 17.0% 17.2% 16.8% Free Cash Flow 2006 2007E 2008E 2009E 2010E 2011E 2012E EBITDA 68 145 279 493 678 780 834 Taxes on EBIT (8) (9) (33) (59) (102) (117) (125) C hange in Net Working Assets (397) (759) (880) (1,106) (341) (376) (301) C APEX (6) (36) (18) (22) (20) (20) (21) FCFF (343) (659) (652) (694) 216 267 387 C hange in Debt (21) 89 214 482 158 129 100 Emission - 623 - - - - - Financial Results (12) (18) (12) (61) (79) (85) (94) Tax difference 2 (5) 3 9 14 15 17 FCFE (374) 30 (447) (264) 309 327 410 Balance Sheet 2006 2007E 2008E 2009E 2010E 2011E 2012E Assets C ash and Equivalents 266 310 130 130 130 130 130 Accounts Receivable 560 924 1,489 2,222 2,621 2,890 3,011 Inventories 441 921 1,375 1,803 1,805 2,008 2,129 Other 227 337 158 (56) 240 494 797 Total Assets 1,494 2,492 3,153 4,099 4,795 5,523 6,067 Liabilities Short Term Debt 28 34 34 34 34 34 34 Real Estate Acquisition Payables 22 25 58 94 126 146 155 C lients Advance Payments 76 17 - - 9 83 - Long Term Debt 267 351 564 1,046 1,204 1,333 1,433 Other 286 553 816 969 1,095 1,168 1,226 Equity 814 1,512 1,680 1,956 2,327 2,759 3,219 Total Liabilities 1,494 2,492 3,153 4,099 4,795 5,523 6,067 Source: Gafisa and Bulltick 13

- 14. Tecnisa Income Statement (R$ MM) 2006 2007E 2008E 2009E 2010E 2011E 2012E Total Launchings 369 1,364 1,778 2,235 2,504 2,601 2,705 Launchings - Tecnisa Stake 285 1,000 1,600 1,900 2,128 2,341 2,434 Total Real Estate Sales 333 706 1,387 1,877 2,270 2,476 2,618 Gross Revenues 211 379 768 1,484 2,016 2,391 2,613 Net Revenues 203 364 740 1,430 1,942 2,304 2,518 - COGS (122) (224) (449) (872) (1,194) (1,425) (1,560) Gross Profit 81 141 291 558 748 879 958 - Sales Expeditures (11) (20) (37) (79) (107) (127) (126) - G&A Expenditures (21) (38) (43) (45) (47) (49) (51) - Management Fees (2) (4) (12) (17) (22) (26) (29) - Other Operational (0) (37) - - - - - EBIT 47 41 199 418 571 677 752 Financial Results 2 17 (12) (47) (55) (58) (64) - Financial Expenses (16) (17) (25) (59) (70) (80) (89) - Financial Revenues 18 34 13 12 15 23 25 Non-Operational Results 1 729 - - - - - EBT 49 59 187 370 516 620 688 Income Tax (9) (9) (22) (44) (52) (62) (69) Employee Interest - - - - - - - Minority Interest (2) (19) (61) (85) (66) (73) Net income 36 48 146 265 380 491 546 Depreciation 0.4 (1.2) 0.4 0.4 0.4 0.4 0.5 Amortization - - - - - - - Employee Interest - - - - - - - EBITDA 47 40 199 418 572 678 753 Adjustments - 40 - - - - - Adjusted EBITDA 47 80 199 418 572 678 753 Gross Margin 40.0% 38.6% 39.3% 39.0% 38.5% 38.2% 38.0% Adjusted EBITDA Margin 23.1% 21.9% 26.9% 29.2% 29.4% 29.4% 29.9% Adjusted Net Margin 17.6% 24.0% 19.8% 18.5% 19.6% 21.3% 21.7% Free Cash Flow 2006 2007E 2008E 2009E 2010E 2011E 2012E EBITDA 47 40 199 418 572 678 753 Minority Adjustment (10) (16) (21) (70) (94) (73) (82) Taxes on EBIT (8) (3) (24) (50) (57) (68) (75) Change in Net Working Assets (88) (567) (678) (1,035) (885) (835) (310) CAPEX (2) (1) (1) (1) (1) (1) (1) FCFF (62) (552) (525) (738) (465) (299) 285 Change in Debt 92 (18) 298 360 95 114 92 Emission - 591 - - - - - Financial Results 2 17 (12) (47) (55) (58) (64) Tax difference (0) (6) 1 6 6 6 6 FCFE 31 32 (237) (419) (420) (237) 319 Balance Sheet 2006 2007E 2008E 2009E 2010E 2011E 2012E Assets Cash and Equivalents 20 120 100 100 100 100 100 Accounts Receivable 174 299 597 1,267 1,820 2,327 2,547 Client Financing - 11 15 26 121 269 260 Inventories 232 659 1,116 1,550 1,841 2,063 2,184 Other 83 94 (52) (430) (858) (1,140) (910) Total Assets 509 1,184 1,777 2,512 3,024 3,619 4,180 Liabilities Short Term Debt 118 41 41 41 41 41 41 Real Estate Acquisition Payables 116 156 239 284 318 350 364 Clients Advance Payments 28 8 2 - - - - Long Term Debt 41 100 398 759 854 968 1,060 Other 61 107 216 349 446 526 572 Equity 145 772 882 1,080 1,365 1,734 2,143 Total Liabilities 509 1,184 1,777 2,512 3,024 3,619 4,180 Source: Tecnisa and Bulltick 14

- 15. Klabin Segall Income Statement (R$ MM) 2006 2007E 2008E 2009E 2010E 2011E 2012E Launchings 773 1,775 1,812 2,084 2,334 2,567 2,670 - Real Estate Sales 400 875 1,706 1,832 2,199 2,358 2,535 Gross Revenues 144 306 738 1,244 1,869 2,127 2,428 Net Revenues 138 292 705 1,188 1,785 2,032 2,319 - COGS (80) (187) (448) (755) (1,138) (1,292) (1,481) Gross Profit 58 106 258 433 646 740 838 - Sales Expeditures (8) (26) (53) (89) (134) (152) (174) - G&A Expenditures (12) (24) (49) (51) (53) (55) (57) - Other Operational (4) (2) - - - - - EBIT 34 58 163 305 479 554 631 Financial Results 5 9 (35) (76) (89) (77) (74) - Financial Expenses (8) (15) (46) (81) (94) (81) (78) - Financial Revenues 12 25 10 5 5 5 5 Non-Operational Results (20) 67 - - - - - EBT 19 67 128 229 390 477 557 Income Tax (8) (13) (26) (46) (78) (95) (111) Employee Interest - - - - - - - Minority Interest (7) (15) (32) (46) (45) (50) (56) Net income 4 39 71 137 267 331 389 Depreciation 3.4 4.8 4.7 1.9 2.3 2.8 3.4 Amortization - - - - - - - EBITDA 38 62 168 307 482 557 634 Adjustments 21 - - - - - - Adjusted EBITDA 59 62 168 307 482 557 634 Gross Margin 41.9% 36.1% 36.5% 36.4% 36.2% 36.4% 36.1% Adjusted EBITDA Margin 42.4% 21.4% 23.8% 25.8% 27.0% 27.4% 27.3% Adjusted Net Margin 17.8% 13.5% 10.0% 11.6% 14.9% 16.3% 16.8% Free Cash Flow 2006 2007E 2008E 2009E 2010E 2011E 2012E EBITDA 38 62 168 307 482 557 634 Minority Adjustment (9) (16) (40) (57) (57) (63) (70) Taxes on EBIT (7) (12) (34) (61) (96) (111) (127) Change in Net Working Assets (90) (471) (333) (669) (483) (237) (204) CAPEX (4) (6) (5) (3) (3) (4) (5) FCFF (73) (442) (243) (482) (157) 142 228 Change in Debt 9 294 308 334 6 2 26 Emission 361 - - - - - - Financial Results 5 9 (35) (76) (89) (77) (74) Tax difference (0) (1) 8 16 18 16 15 FCFE 302 (140) 38 (208) (222) 84 196 Balance Sheet 2006 2007E 2008E 2009E 2010E 2011E 2012E Assets Cash and Equivalents 281 243 49 49 49 49 49 Accounts Receivable 104 209 465 808 1,052 1,161 1,289 Client Financing - - - - - - - Inventories 190 645 753 1,169 1,479 1,659 1,773 Other 38 (18) 230 63 (138) (71) 90 Total Assets 613 1,079 1,496 2,089 2,442 2,797 3,200 Liabilities Short Term Debt 16 12 12 12 12 12 12 Real Estate Acquisition Payables 101 189 193 222 249 273 284 Clients Advance Payments 1 1 0 - - - - Long Term Debt 12 309 617 952 958 960 986 Other 64 160 213 340 459 539 613 Equity 419 408 461 564 764 1,013 1,305 Total Liabilities 613 1,079 1,496 2,089 2,442 2,797 3,200 Source: Klabin Segall and Bulltick 15

- 16. Company Income Statement (R$ MM) 2006 2007E 2008E 2009E 2010E 2011E 2012E Launchings 353 1,033 1,500 1,875 2,100 2,184 2,271 - Real Estate Sales 258 695 1,149 1,446 1,839 2,035 2,178 Gross Revenues 300 484 770 1,035 1,497 1,874 2,142 Net Revenues 289 451 742 997 1,442 1,806 2,064 - COGS (190) (313) (495) (654) (957) (1,210) (1,398) Gross Profit 99 138 247 343 485 596 665 - SG&A expenditures (26) (43) (82) (110) (159) (199) (227) - Other Operational (12) (6) - - - - - EBIT 61 89 165 233 327 398 438 Financial Results (2) (16) (20) (48) (57) (67) (72) - Financial Expenses (17) (35) (32) (59) (67) (77) (83) - Financial Revenues 15 19 12 11 11 10 10 Non-Operational Results (0) 767 - - - - - EBT 55 74 145 185 270 331 366 Income Tax (7) (9) (22) (28) (41) (50) (55) Employee Interest (2) - - - - - - Minority Interest (0) - - - - - - Net income 45 64 123 157 230 281 311 Depreciation 0.4 0.4 0.4 0.4 0.4 0.4 0.4 EBITDA 59 90 166 233 327 398 439 Adjustments 10 - - - - - - Adjusted EBITDA 69 90 166 233 327 398 439 Gross Margin 34.2% 30.7% 33.3% 34.4% 33.6% 33.0% 32.2% Adjusted EBITDA Margin 24.0% 19.8% 22.4% 23.4% 22.7% 22.0% 21.3% Adjusted Net Margin 19.3% 14.2% 16.6% 15.8% 15.9% 15.6% 15.1% Free Cash Flow 2006 2007E 2008E 2009E 2010E 2011E 2012E EBITDA 59 90 166 233 327 398 439 Taxes on EBIT (8) (11) (25) (35) (49) (60) (66) Change in Net Working Assets (175) (225) (541) (841) (535) (619) (367) CAPEX (1) (0) (0) (0) (0) (0) (0) FCFF (125) (147) (400) (643) (257) (281) 6 Change in Debt 73 155 222 304 74 103 60 Emission - - - - - - - Financial Results (2) (16) (20) (48) (57) (67) (72) Tax difference 1 2 3 7 8 10 11 FCFE (54) (6) (196) (379) (231) (234) 4 Balance Sheet 2006 2007E 2008E 2009E 2010E 2011E 2012E Assets Cash and Equivalents 119 109 109 109 109 109 109 Accounts Receivable 297 371 819 1,379 1,687 2,111 2,351 Inventories 133 306 457 799 1,070 1,290 1,436 Other 59 89 (100) (489) (742) (1,022) (1,080) Total Assets 607 875 1,285 1,798 2,124 2,489 2,816 Liabilities Short Term Debt 50 61 61 61 61 61 61 Suppliers 12 15 22 27 30 32 33 Real Estate Acquisition Payables 35 52 76 95 106 110 115 Clients Advance Payments 2 0 0 - - - - Long Term Debt 80 225 447 751 825 929 988 Other 137 188 252 318 384 428 457 Equity 291 335 428 546 718 929 1,162 Total Liabilities 607 875 1,285 1,798 2,124 2,489 2,816 Source: Company and Bulltick 16

- 17. APPENDIX B IMPORTANT DISCLOSURES Bulltick Brasil Consultoria e Assessoria Empresarial Ltda. is an affiliate of Bulltick LLC (The Firm). Bulltick LLC may do business with the companies covered in this report, as a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report only as a single factor in making their investment decision. A. CONFLICTS OF INTEREST From the companies covered in this report, Bulltick Brasil Consultoria e Assessoria Empresarial Ltda, or its affiliates, currently has, or has had within the past 12 months, Tecnisa and MRV as client and/or received compensation for products and services provided to this company. From the companies covered in this report, Bulltick Brasil Consultoria e Assessoria Empresarial Ltda, or its affiliates, managed or co-managed a public offering of securities for Tecnisa and MRV in the past 12 months, received compensation for investment banking services from Tecnisa and MRV in the past 12 months. Neither Bulltick Brasil Consultoria e Assessoria Empresarial Ltda nor any of its affiliates own equity securities of any of the subject companies. Analyst compensation is determined by Bulltick Brasil Consultoria e Assessoria Empresarial Ltda management and is not linked to specific transactions or recommendations. B. ANALYST CERTIFICATION I, Rafael Pinho, author of this report, hereby certify that all of the views expressed in this report accurately reflect my personal views about any and all of the subject issuer(s) or securities, no part of my compensation was, is , or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. I have not received any compensation from any of the subject companies in the past 12 months. I also certify that neither I nor any member of my household serves as a director, officer, or advisory board member of any of the subject companies in this report. C. INVESTMENT RATING Investment ratings are determined by the ranges described below: BUY: Total return of securities expected to be above 18% (in dollar terms) in the following 12 months NEUTRAL: Total return of securities expected to be below 18% (in dollar terms) and above 8% (in dollar terms) in the following 12 months. SELL: Total return of securities expected to be below 8% (in dollar terms) in the following 12 months. Price Target: The valuation method used to determine the price targets in this report were based on the discounted cash flow methodology. D. RISK RATINGS Risks for the achievement of the target prices defined in this report include major change in our base case macro- economic scenario, increase in interest rates and in the Brazil risk, reduction in the expectations for demand for real estate in Brazil and impact on already listed stocks of new IPOs in Brazil´s real estate sector. Based on last 6 months volatility of subject companies, and comparing them to the volatility of the Bovespa Index (Ibovespa) in the same period, we define each subject company´s relative volatility in the following way: Company High, Cyrela High, Gafisa High, Klabin Segall High, Rossi Residencial High and Tecnisa High 17

- 18. OTHER DISCLOSURES Bulltick Brasil Consultoria e Assessoria Empresarial Ltda and its subsidiaries, affiliates, shareholders, directors, officers, employees, and licensors (“The Bulltick Parties”) will not be liable (individually, jointly, or severally) to you or any other person as a result of your access, reception or use of the information contained in this document for indirect, consequential, special, incidental, punitive, or exemplary damages, including, without limitation, lost profits, lost savings and lost revenues (collectively, the “Excluded Damages”), whether or not characterized in negligence, tort, contract, or other theory of liability. The information contained in this document has been obtained from sources believed to be reliable, although its accuracy and completeness cannot be guaranteed. All opinions, projections, and estimates constitute the judgment of the author as of the date of the report and these, plus any other information contained in the report, are subject to change without notice. Prices and availability of financial instruments also are subject to change without notice. Bulltick Brasil Consultoria e Assessoria Empresarial Ltda and its affiliated companies have not taken any steps to insure that the securities referred to in this report are suitable for any particular investor. The Report is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. Securities mentioned in the report are subject to investment risks, including the possible loss of the principal amount invested. Any decision to purchase securities mentioned in the Report must take into account existing public information on such a security or any registered prospectus. The financial instruments mentioned in this document may not be eligible for sale in some countries. The Report is not to be construed as providing investment services in any jurisdiction where the provision of such services would be illegal. Bulltick Brasil Consultoria e Assessoria Empresarial Ltda, its affiliated companies, and/or its officers, directors, or shareholders, may from time to time have long or short positions in the financial instruments of the companies mentioned in this document, engage in securities transactions in a manner inconsistent with this report, buy or sell from customers on a principal basis, or serve in an advisory capacity. Investing in non-US securities, including ADRs, may entail certain risks. The securities of non-US issuers may not be registered with, and may not be subject to the reporting requirements of the US Securities and Exchange Commission. There may be limited information available on foreign securities. Foreign companies are generally not subject to uniform audit and reporting standards, practices and requirements comparable to those in the US Securities of some foreign companies may be less liquid and their prices more volatile than securities of comparable US companies. In addition, exchange rate movements may have an adverse effect on the value of an investment in a foreign stock and its corresponding dividend payment for US investors. The information contained in the report is privileged and confidential and intended solely for the recipients who have been specifically authorized to receive it and it may not be further distributed. Bulltick Brasil Consultoria e Assessoria Empresarial Ltda and its affiliates accept no liability whatsoever for the actions of third parties. Should you receive this message by mistake you are hereby notified that any disclosure reproduction, distribution, or use of this message is strictly prohibited. The Report may provide the addresses of, or contain hyperlinks to, websites. Except to the extent to which the Report refers to the website material of the Bulltick Brasil Consultoria e Assessoria Empresarial Ltda or any of its affiliates, the Firm has not reviewed the linked site. Equally, except to the extent to which the Report refers to website material of Bulltick Brasil Consultoria e Assessoria Empresarial Ltda or any of its affiliates, the Firm takes no responsibility for, and makes no representation or warranties whatsoever as to, the data and information contained therein. Such address or hyperlink (including addresses or hyperlinks to website material of Bulltick Brasil Consultoria e Assessoria Empresarial Ltda or any of its affiliates) is provided solely for your convenience and information and the content of the linked site does not in any way form part of this document. Accessing such website or following such link through the Report or the website of Bulltick Brasil Consultoria e Assessoria Empresarial Ltda or any of its affiliates shall be at your own risk and Bulltick Brasil Consultoria e Assessoria Empresarial Ltda or any of its affiliates shall have no liability arising out of, or in connection with, and such referenced website. 18