Low Rates and Housing

•

0 j'aime•348 vues

House prices in the UK rose 0.9% in July 2013, the sixth successive monthly increase and greatest increase since August 2010. This represents a 4.6% annual increase bringing the average UK house price to £169,624. The document examines three potential reasons for rising house prices: 1) increased consumer confidence in the economy, 2) low interest rates due to Bank of England monetary policy, and 3) the government's Help to Buy home buying scheme.

Recommandé

Recommandé

Contenu connexe

Similaire à Low Rates and Housing

Similaire à Low Rates and Housing (20)

Plus de tutor2u

Plus de tutor2u (20)

Dernier

Dernier (20)

Low Rates and Housing

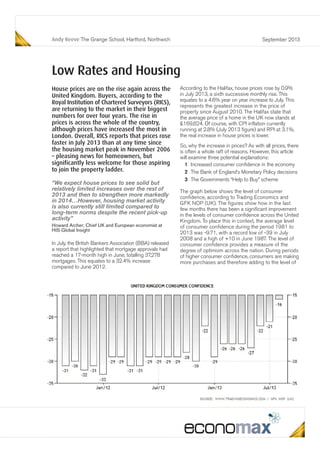

- 1. Andy Reeve The Grange School, Hartford, Northwich September 2013 According to the Halifax, house prices rose by 0.9% in July 2013, a sixth successive monthly rise. This equates to a 4.6% year on year increase to July. This represents the greatest increase in the price of property since August 2010. The Halifax state that the average price of a home in the UK now stands at £169,624. Of course, with CPI inflation currently running at 2.8% (July 2013 figure) and RPI at 3.1%, the real increase in house prices is lower. So, why the increase in prices? As with all prices, there is often a whole raft of reasons. However, this article will examine three potential explanations: 1 Increased consumer confidence in the economy 2 The Bank of England’s Monetary Policy decisions 3 The Governments “Help to Buy” scheme The graph below shows the level of consumer confidence, according to Trading Economics and GFK NOP (UK). The figures show how in the last few months there has been a significant improvement in the levels of consumer confidence across the United Kingdom. To place this in context, the average level of consumer confidence during the period 1981 to 2013 was -9.71, with a record low of -39 in July 2008 and a high of +10 in June 1987. The level of consumer confidence provides a measure of the degree of optimism across the nation. During periods of higher consumer confidence, consumers are making more purchases and therefore adding to the level of Low Rates and Housing “We expect house prices to see solid but relatively limited increases over the rest of 2013 and then to strengthen more markedly in 2014…However, housing market activity is also currently still limited compared to long-term norms despite the recent pick-up activity” Howard Archer; Chief UK and European economist at HIS Global Insight House prices are on the rise again across the United Kingdom. Buyers, according to the Royal Institution of Chartered Surveyors (RICS), are returning to the market in their biggest numbers for over four years. The rise in prices is across the whole of the country, although prices have increased the most in London. Overall, RICS reports that prices rose faster in July 2013 than at any time since the housing market peak in November 2006 – pleasing news for homeowners, but significantly less welcome for those aspiring to join the property ladder. In July, the British Bankers Association (BBA) released a report that highlighted that mortgage approvals had reached a 17-month high in June, totalling 37,278 mortgages. This equates to a 32.4% increase compared to June 2012.

- 2. Andy Reeve The Grange School, Hartford, Northwich economic activity. This heightened consumer confidence might explain the reason for house price rises. Equally, the increases in house prices might help to explain the increased levels of confidence – the Wealth Effect. The new governor of the Bank of England, Mark Carney announced a new form of monetary policy at the beginning of August. Carney provided a clear signal to the markets that the Bank of England will not increase the Base Rate from 0.5% until the official measure of unemployment falls from its current rate of 7.8% to 7%. In other words, the nation will need to generate an additional 750,000 jobs before the end of 2016 before the Bank considers an increase in rates. This form of “forward guidance” has not been adopted in the United Kingdom before. The Bank also stressed that it would keep the level of Quantitative Easing at £375 billion until the end of 2016 as well. Business leaders welcomed the decision, as it provides them with security and confidence. Equally, it means that mortgage payments will not rise in the foreseeable future and it is hoped that the news will lead to more lenders providing cheaper fixed rate mortgages. Finally, the Government’s “Help to Buy” scheme will provide an incentive for buyers to purchase property. The first phase of the scheme was introduced in April 2013 and allowed buyers of new-build properties to borrow 20% of the property’s value as an interest- free five year loan. The latest government figures show that 10,000 houses have been purchased using the scheme. The more significant second phase will begin in January 2014. This will offer £12 billion of government guarantees to back mortgages for buyers who lack large deposits. Vince Cable, the Business Secretary, spoke of his concern that the scheme might help to create a housing price bubble. Speaking on the BBC Andrew Marr show, Cable stated that “the proposal which hasn’t been implemented, which is providing a guarantee for a limited range of mortgages, could be a problem. It could inflate the market”. Although the “Help to Buy” scheme has been welcomed by British mortgage lenders and house builders, it has been criticised by the government’s watchdog – the Office for Budget Responsibility. http://uk.reuters.com/article/2013/07/28/uk-britain- economy-housing-cable-idUKBRE96R06I20130728 www.telegraph.co.uk/finance/personalfinance/house- prices/10163028/Is-there-a-house-price-bubble-on- the-horizon.html www.ft.com/cms/s/0/535f956c-000c-11e3-9c40- 00144feab7de.html#axzz2bmve24Mm www.bbc.co.uk/news/business-23668507 www.thisismoney.co.uk/money/news/article- 1607881/When-UK-rates-rise.html “The world must have gone mad for us to now be discussing endless taxpayer guarantees for mortgages” Graeme Leach, the chief economist at the Institute of Directors