1. QE Intra-Day Movement

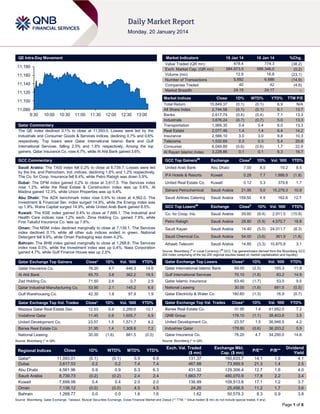

Market Indicators

11,180

11,160

11,140

11,120

Market Indices

11,100

11,080

9:30

19 Jan 14

478.4

584,973.5

12.9

5,692

40

24:15

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index declined 0.1% to close at 11,093.0. Losses were led by the

Industrials and Consumer Goods & Services indices, declining 0.7% and 0.6%

respectively. Top losers were Qatar International Islamic Bank and Gulf

International Services, falling 2.5% and 1.8% respectively. Among the top

gainers, Qatar Insurance Co. rose 4.7%, while Al Ahli Bank gained 3.6%.

16 Jan 14

774.3

586,346.0

16.8

6,688

42

24:17

%Chg.

(38.2)

(0.2)

(23.1)

(14.9)

(4.8)

–

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

15,849.37

2,744.58

2,617.74

3,676.24

1,969.30

2,077.46

2,566.10

1,532.69

6,049.89

3,228.86

(0.1)

(0.1)

(0.4)

(0.7)

0.4

1.4

3.0

0.3

(0.6)

0.1

(0.1)

(0.1)

(0.4)

(0.7)

0.4

1.4

3.0

0.3

(0.6)

0.1

6.9

6.1

7.1

5.0

6.0

6.4

9.8

5.4

1.7

6.3

N/A

13.7

13.3

13.3

13.3

14.2

10.3

20.8

22.9

16.7

GCC Commentary

GCC Top Gainers##

Exchange

Close#

1D%

Saudi Arabia: The TASI index fell 0.2% to close at 8,739.7. Losses were led

by the Ins. and Petrochem. Ind. indices, declining 1.6% and 1.2% respectively.

The Co. for Coop. Insurance fell 8.4%, while Petro Rabigh was down 5.9%.

United Arab Bank

Abu Dhabi

7.00

8.5

19.2

8.5

IFA Hotels & Resorts

Kuwait

0.28

7.7

1,888.9

(1.8)

Dubai: The DFM index gained 0.2% to close at 3,617.5. The Services index

rose 1.2%, while the Real Estate & Construction index was up 0.6%. Al

Madina gained 12.3%, while Union Properties was up 9.4%.

United Real Estate Co.

Kuwait

0.12

5.3

379.8

1.7

Sahara Petrochemical

Saudi Arabia

21.95

5.0

15,279.3

10.9

Abu Dhabi: The ADX benchmark index rose 0.9% to close at 4,562.0. The

Investment & Financial Ser. index surged 14.9%, while the Energy index was

up 1.9%. Waha Capital surged 14.9%, while United Arab Bank gained 8.5%.

Saudi Airlines Catering

Saudi Arabia

159.50

4.9

162.6

12.7

GCC Top Losers

Exchange

1D% Vol. ‘000

YTD%

Kuwait: The KSE index gained 0.4% to close at 7,699.1. The Industrial and

Health Care indices rose 1.2% each. Zima Holding Co. gained 7.9%, while

First Takaful Insurance Co. was up 7.8%.

Co. for Coop. Ins.

Saudi Arabia

29.60

(8.4)

2,911.5

(15.9)

Petro Rabigh

Saudi Arabia

28.80

(5.9)

4,570.7

18.8

Oman: The MSM index declined marginally to close at 7,139.1. The Services

index declined 0.1% while all other sub indices ended in green. National

Detergent fell 9.9%, while Oman Packaging was down 4.2%.

Saudi Kayan

Saudi Arabia

14.40

(5.0)

24,011.7

(8.3)

Saudi Chemical Co.

Saudi Arabia

54.00

(3.6)

361.9

(1.8)

Atheeb Telecom

Saudi Arabia

14.85

(3.3)

10,875.8

3.1

Bahrain: The BHB index gained marginally to close at 1,268.8. The Services

index rose 0.5%, while the Investment index was up 0.4%. Nass Corporation

gained 4.7%, while Gulf Finance House was up 2.5%.

##

#

Close

Vol. ‘000

YTD%

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Insurance Co.

Close*

1D%

Vol. ‘000

YTD%

Close*

1D%

Vol. ‘000

YTD%

76.20

Qatar Exchange Top Gainers

4.7

446.3

14.6

Qatar International Islamic Bank

69.00

(2.5)

165.3

11.8

362.2

19.5

Gulf International Services

70.10

(1.8)

83.2

14.9

Qatar Exchange Top Losers

Al Ahli Bank

65.70

3.6

Zad Holding Co.

71.50

2.6

0.7

2.9

Qatar Islamic Insurance

63.40

(1.7)

53.5

9.5

Qatar Industrial Manufacturing Co.

53.90

2.1

145.2

6.5

National Leasing

30.00

(1.6)

881.5

(0.5)

Gulf Warehousing Co.

42.30

1.8

97.9

1.9

Qatar Electricity & Water Co.

180.60

(1.3)

16.9

(0.7)

Qatar Exchange Top Val. Trades

Close*

1D%

Val. ‘000

YTD%

31.95

1.4

41,682.0

7.2

178.10

(1.1)

38,403.6

3.5

23.57

1.5

36,946.5

4.2

178.80

(0.6)

36,203.2

5.9

76.20

4.7

34,290.0

14.6

Close*

1D%

Vol. ‘000

YTD%

Mazaya Qatar Real Estate Dev.

12.53

0.4

2,289.6

12.1

Vodafone Qatar

11.45

0.9

1,655.7

6.9

QNB Group

United Development Co.

23.57

1.5

1,571.7

4.2

United Development Co.

Barwa Real Estate Co.

31.95

1.4

1,309.8

7.2

Industries Qatar

National Leasing

30.00

(1.6)

881.5

(0.5)

Qatar Exchange Top Vol. Trades

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

Qatar Insurance Co.

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Regional Indices

Barwa Real Estate Co.

Close

1D%

WTD%

MTD%

YTD%

11,093.01

3,617.53

4,561.96

8,739.73

7,699.06

7,139.12

1,268.77

(0.1)

0.2

0.9

(0.2)

0.4

(0.0)

0.0

(0.1)

0.2

0.9

(0.2)

0.4

(0.0)

0.0

6.9

7.4

6.3

2.4

2.0

4.5

1.6

6.9

7.4

6.3

2.4

2.0

4.5

1.6

Exch. Val. Traded

($ mn)

131.37

467.98

431.32

1,663.77

136.99

24.26

1.62

Exchange Mkt.

Cap. ($ mn)

160,633.7

73,999.9

129,306.4

480,070.9

109,513.8

25,456.5

50,579.3

P/E**

P/B**

14.1

21.3

12.7

17.8

17.1

11.2

8.3

1.9

1.4

1.6

2.2

1.2

1.7

0.9

Dividend

Yield

4.1

2.5

4.0

3.4

3.7

3.6

3.8

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

Page 1 of 6

2. Qatar Market Commentary

The QE index declined 0.1% to close at 11,093.0. The Industrials

and Consumer Goods & Services indices led the losses. The

index declined on the back of selling pressure from Qatari

shareholders despite buying support from non-Qatari

shareholders.

Qatar International Islamic Bank and Gulf International Services

were the top losers, falling 2.5% and 1.8% respectively. Among

the top gainers, Qatar Insurance Co. rose 4.7%, while Al Ahli

Bank gained 3.6%.

Overall Activity

Buy %*

Sell %*

Net (QR)

Qatari

64.61%

67.95%

(16,035,929.30)

Non-Qatari

35.40%

32.04%

16,035,929.30

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Sunday fell by 23.1% to 12.9mn

from 16.8mn on Thursday. However, as compared to the 30-day

moving average of 11.3mn, volume for the day was 14.1%

higher. Mazaya Qatar Real Estate Dev. and Vodafone Qatar

were the most active stocks, contributing 17.7% and 12.8% to

the total volume respectively.

Earnings

Earnings Releases

Company

Revenue

(mn) 4Q2013

% Change

YoY

Operating Profit

(mn) 4Q2013

% Change

YoY

Net Profit (mn)

4Q2013

% Change

YoY

SR

–

–

52.8

10.1%

48.3

11.0%

Saudi Arabia

SR

–

–

360.7

38.0%

196.8

24.8%

Saudi Arabia

SR

–

–

122.9

-3.1%

127.2

22.5%

Saudi Arabia

SR

–

–

55.2

26.3%

50.4

18.3%

Saudi Arabia

SR

–

–

51.6

-27.1%

62.7

-7.1%

Saudi Arabia

SR

–

–

1.9

9.8%

-0.2

-66.7%

Saudi Arabia

SR

–

–

21.4

-7.8%

20.4

-18.4%

Saudi Arabia

SR

–

–

10,300.0

0.5%

6,160.0

5.7%

Saudi Arabia

SR

–

–

154.6

NA

3.4

NA

Saudi Arabia

SR

–

–

458.2

4.8%

373.3

1.2%

Saudi Arabia

SR

–

–

0.0

22.9%

0.0

3.5%

Saudi Arabia

SR

–

–

30.0

1.2%

34.4

4.2%

Saudi Arabia

SR

42.9

108.6%

–

–

17.5

64.1%

Saudi Arabia

SR

–

–

29.0

-51.8%

20.4

-65.4%

Saudi Arabia

SR

–

–

-0.6

NA

-0.8

NA

Saudi Arabia

SR

53.8

99.1%

–

–

13.2

320.8%

Saudi Arabia

SR

50.7

45.3%

–

–

0.5

-0.6%

Saudi Arabia

SR

6.3

NA

–

–

0.4

NA

Saudi Arabia

SR

–

–

260.1

NA

219.9

5014.0%

Saudi Arabia

SR

–

–

-5.7

-46.7%

37.9

NA

Saudi Arabia

SR

–

–

39.4

-24.2%

38.1

-16.3%

Saudi Arabia

SR

255.3

180.8%

–

–

4.4

164.6%

Saudi Arabia

SR

–

–

26.2

147.2%

19.8

52.3%

Saudi Arabia

SR

16.4

1.2%

–

–

0.5

25.0%

Saudi Arabia

SR

5.5

NA

–

–

0.8

NA

Saudi Arabia

SR

50.8

97.1%

–

–

0.7

-9.6%

Saudi Arabia

SR

–

–

4.8

NA

4.6

Market

Currency

City Cement Co. (CCC)

Saudi International

Petrochemical Co.

(Sipchem)

Saudi Airlines Catering Co.

Mouwasat Medical Services

Company (Mouasat)

Alabdullatif Industrial

Investment co. (Al Abdullatif)

National Gypsum Company

(National Gypsum)

National Medical Care

Company (Care)

Saudi Basic Industries Corp

(SABIC)

Saudi Kayan Petrochemical

Company (Saudi Kayan)

Almarai Company

National Agriculture

Development Co. (Nadec)

Saudi Public Transport Co.

(SAPTCO)

Saudi Re for Cooperative

Reinsurance Company

(Saudi-Re)

Najran Cement Co.

Saudi Arabia Refineries Co.

(SARCO)

Saudi United Cooperative

Insurance Co. (Walaa)

Arabian Shield Cooperative

Insurance Co. (Arabian

Shield)

Alinma Tokio Marine Co.

(Alinma Tokio M)

Emaar The Economic City

(Emaar)

Arabian Pipes Co.

(Anabeeb)

Tabuk Cement Co.

Trade Union Cooperative

Insurance Co. (Trade Union)

Al-Babtain Power &

Telecommunication Co. (AlBabtain)

Ace Arabia Cooperative

Insurance Co. (ACE)

Saudi Enaya Cooperative

Insurance Co.

Buruj Cooperative Insurance

Saudi Arabia

Saudi Advanced Industries

NA

Page 2 of 6

3. Al Alamiya for Cooperative

Insurance Co.

United Int. Transportation

Co. (Budget-Saudi)

Taiba Holding Co. (Taiba)

Ash-Sharqiyah Development

Co. (Sharqiya Dev Co)

Northern Region Cement

Co. (Northern Cement)

Herfy Food Services Co.

Saudi Re for Cooperative

Reinsurance Co. (Saudi-Re)

Gulf Int. Chemicals*

Saudi Arabia

SR

38.5

-4.5%

–

–

0.4

Saudi Arabia

SR

–

–

18.4

864.4%

37.5

5.3%

Saudi Arabia

SR

–

–

55.7

15.3%

64.5

52.1%

Saudi Arabia

SR

–

–

-2.2

16.9%

-0.9

-45.0%

Saudi Arabia

SR

–

–

59.6

187.6%

51.6

187.5%

Saudi Arabia

SR

–

–

50.8

2.6%

51.3

5.1%

Saudi Arabia

SR

42.9

108.6%

–

–

17.5

64.1%

-2.5%

Oman

OMR

3.6

9.7%

–

–

0.3

18.9%

National Finance*

Oman

OMR

–

–

10.6

14.0%

4.8

16.5%

The Financial Corporation#

Oman

OMR

–

–

1.0

3979.7%

1.2

NA

Source: Company data, DFM, ADX, MSM (*FY2013 results) (#9M2013 results)

News

Qatar

QIBK 4Q2013 net profit broadly in line with our expectations

– QIBK posted a net profit (to equity) of QR360.3mn in 4Q2013

vs. our estimate of QR365.3mn (BBG consensus, ex-QNBFS:

QR340mn). Net income increased by 4.4% QoQ. Profitability

was driven by net financing income (+6.4% QoQ). However,

income from investing activities (QR180.6mn) declined by

20.3% QoQ. Cash dividend increased to QR4/share. QIBK

upped its DPS to QR4.00 from QR3.75 in 2012. This translates

into a yield of 5.4%. For 2014, we expect a DPS of QR4.25.

2013 analysis: QIBK’s loan book expanded by 9.3% YoY to

QR47.1bn in 2013. Equity of unrestricted investment account

holders (URIA) also increased by 11.2% YoY to QR37.9bn.

Furthermore, customers deposits in current accounts increased

by 37.3% YoY to QR12.5bn. Hence, the loan-to-deposit ratio

declined to 93.6% vs. 100.0% at the end of 2012. In terms of the

investment book, total investments increased by 11.2% YoY.

Growth was driven by fixed income securities while equity

investments declined YoY. We maintain our estimates for 2014;

retain our Market Perform rating and target price of QR73.27.

We expect QIBK to post EPS of QR5.91 and QR6.24 for 2014

and 2015, respectively. Furthermore, we maintain QIBK’s target

price at QR73.27 and Market Perform rating. Valuation appears

fair. QIBK is trading at a P/E and a P/B of 12.3x and 1.4x on our

2014 estimates, respectively. QIBK has underperformed the

sector index. In 2013, the stock was down 3.22% (total return)

vs. the QE All Share Banks & Financial Services Index, which

was up 25.36%. (QNBFS Research, QE)

GWCS’ 4Q2013 bottom-line up by 18.2% QoQ – Gulf

Warehousing reported a net profit of QR26.83mn vs.

QR22.71mn in 3Q2013. The firm booked other income of

QR1mn in 4Q2013 vs. QR0.08mn in 2012, which was the

primary difference vs. our bottom-line estimate of QR25.3mn.

For the full year (2013), profit to equity holders stood at

QR101.6mn vs. QR84.9mn in 2012, up 19.7% YoY. The

company announced a cash DPS of QR1.50 vs. a 20% stock

dividend in 2012. For FY2013, overall revenue increased to

QR527.3mn in 2013 vs. QR479.7mn in 2012, a growth of 9.9%

YoY. In our view, the growth primarily came from LVQ Phase 3

coming online in 2013. Direct costs increased 4.0% YoY.

Furthermore, G&A expenses increased by 3.7% YoY. On the

Imdad front, GWCS booked a provision of QR6.3mn (51% share

leads to a hit of QR3.2mn). We maintain our estimates with a

price target of QR45.75; however, given the stock’s

appreciation, we change our rating to Market Perform. We

expect better operating performance in 2014 & 2015 on the back

of LVQ Phase 3 & 4. Our overall thesis on the company remains

unchanged; GWCS is the market leader and the only recognized

player in the Qatari logistics market. The company benefits from

the Qatar growth story and has embarked on aggressive debtfinanced expansions that will almost double its bottom-line and

ROE over the next four years. GWCS trades at a premium to its

regional and global peers. In 2013, the stock was up 23.88%

(total return) vs. the QE All Share Transportation Index, which

was also up 38.65%. (QNBFS Research, QE)

IQCD announces shutdown schedule of its production

facilities in 1Q2014 – Industries Qatar (IQCD) has confirmed its

planned shutdown timetable for 1Q2014 for all its Qatar-based

production facilities. The planned shutdown schedule, with prior

year comparatives, is as follows: Ethylene: 35 days (1Q2013: 0

days); LDPE: 34 days (1Q2013: 11 days); LLDPE: 11days

(1Q2013: 0 days); Methanol: 10 days (1Q2013: 0 days); MTBE:

8 days (1Q2013: 0 days); Ammonia: 40 days (1Q2013: 1 day);

Urea: 40 days (1Q2013: 7 days); and Steel ( DR, EF/CC & RM):

22 days (1Q2013: 40 days). This shut-down schedule is

indicative of current plans only, and actual down-time may vary

from the latest plan. The announced shutdowns are somewhat

different from previously detailed maintenance-related

shutdowns stated in IQCD’s 5-year business plan. We do not

expect material changes to our estimates as a result of these

announced shutdowns. (QNBFS Research, QE)

E&Y: Qatar hospitality market posts dip in room yield –

According to a report by E&Y, the hospitality market in Qatar

saw a 4% YoY decrease in room yield during JanuaryNovember 2013, while it maintained a 65% occupancy rate for

the first 11 months of 2013 and 2012. The decline in revenue

per available room (RevPAR) is largely due to a 3.4% dip in the

average room rate from QR951 during January-November 2012

to QR919 for January-November 2013. The report for November

said the hospitality market in Doha saw a dip of 3% YoY in its

occupancy rates. However, the sector saw a 16.1% decrease in

RevPAR to QR916 in November 2013, falling from QR1,052 in

November 2012. (Peninsula Qatar)

Commercial Bank opens two branches – The Commercial

Bank of Qatar has opened two new branches at the St Regis

Hotel and the Al Gassar Resort in Doha. With these two, the

bank has a network of 30 branches and is supported by 151

ATMs, in addition to internet banking and mobile banking

services. (Gulf-Times.com)

Kahramaa to launch new water plants – Qatar General

Electricity & Water Corporation (Kahramaa) is to launch new

water plants in Duhail, Umm Qarn, Mesaimeer, south Doha and

Muathier, as part of a major project aimed at raising its strategic

reserves. The Duhail plant will be the largest in Qatar with a total

capacity of 142mn gallons, holding one-third of water reserves in

Qatar. This plant will serve areas including Lusail, Al Kheesa

and Rowdath Al Hammam. The Umm Qarn plant costing

Page 3 of 6

4. QR973mn has five reservoirs with a capacity of 71mn gallons

and will serve Umm Qarn, Semaisma and surrounding areas.

Meanwhile, Kahramaa is preparing to launch another large

water reservoir project to support the newly developed areas in

the country. (Peninsula Qatar)

MMUP to allot 7,782 plots to eligible citizens – The Ministry

of Municipality & Urban Planning (MMUP) has announced that it

will allot 7,782 plots of land all over the country to eligible

citizens this year. Currently, the titles of the plots are being

changed so they could be allotted. Areas where these plots are

located are being provided with basic services, including roads.

The ministry also has plans to allot 1,800 more plots for

residential purposes in the near future. (Peninsula Qatar)

QATI’s AGM, EGM to be held on February 16 – Qatar

Insurance Company (QATI) has announced that its AGM and

EGM will be held on February 16, 2014. The agenda of the AGM

covers the board’s proposal for distribution of profits such as

cash dividends of 25% from the par value of the share, i.e.

QR2.5 for each share, and a bonus share issued 25% of the

capital, i.e. one share for each four shares. The EGM’s agenda

includes approving the increase in the company's capital from

QR1,284,323,040 to QR1,605,403,800 by distributing bonus

shares. (QE)

Total looks to expand activities in Qatar – French oil

company Total’s President Yves-Louis Darricarrère said the

company is committed to further developing its activities in Qatar

over the long-term. He added that the company’s oil & gas

production in Qatar averaged at 140,000 barrels of oil equivalent

per day in 2013. (Gulf-Times.com)

QISI’s AGM scheduled on March 12 – Qatar Islamic Insurance

Company (QISI) has announced that its AGM will be held on

March 12, 2014 or on March 17, 2014 in case the desired

quorum for the meeting is not achieved. (QE)

QEWS’ BoD to meet on February 5 – Qatar Electricity & Water

Company’s (QEWS) board of directors will meet on February 5,

2014 to discuss the company’s financial results ending on

December 31, 2013. (QE)

AKHI’s BoD to meet on February 19; AGM on March 23 – Al

Khaleej Takaful Group’s (AKHI) board will meet on February 19,

2014 to discuss the company’s financial results ending on

December 31, 2013 as well as to discuss the proposal of profit

distribution for FY2013. Further, the AGM will be held on March

23, 2014 and an alternate meeting will be on March 26, 2014.

(QE)

IATA-accredited agencies grow to 143 in Qatar – According

to the data by the International Air Transport Association (IATA),

the total number of IATA-accredited travel agencies in the

country jumped to 143 in 2013, from merely 17 in 2007. The

figures show that the number of IATA-accredited travel agencies

in Qatar has witnessed a consistent double-digit growth over the

last six years, with 126 companies being accredited by IATA

between 2008 and 2013. This growth is powered by Qatar’s

emergence as a new aviation hub in the region backed by a

booming tourism industry. (Peninsula Qatar)

International

Weidmann: No reason for irrational inflationary fears –

Germany's Bundesbank President Jens Weidmann said there

was no reason for "irrational inflationary fears" and dismissed

suggestions of a danger of the Eurozone falling into deflation,

echoing the European Central Bank's outlook. Jens Weidmann

also urged France to live up to its function as a role model and

show its peers how to restore economic competitiveness, saying

it was decisive for the recovery of the whole the Eurozone.

(Reuters)

China's economic growth eases to 7.7% in 4Q2013 – China's

annual growth eased to 7.7% in 4Q2013 as investment and

demand flagged late in the year. That leaves growth in the

Chinese economy at 7.7% for all of 2013, unchanged from

revised levels in 2012. The fourth-quarter growth rate compared

with 7.6% forecast by analysts in a Reuters poll but eased from

7.8% in the previous three months. On a quarterly basis, GDP

rose 1.8% from July-September, slower than expectations for

2.0% and a reading of 2.2% in April-June. (Reuters)

China’s 2013 new home sales to exceed $1tn – China’s new

home sales last year likely exceeded $1tn for the first time as

property prices in cities the government considers first tier

surged in the absence of more nationwide property curbs. China

Real Estate Information Corp. (CRIC) has forecasted that

National Bureau of Statistics numbers to be released will show

2013 sales topped $1tn. The value was $975bn in the first 11

months. Earlier, the Bureau said new-home prices in December

climbed 20% in Guangzhou and Shenzhen from a year earlier,

and jumped 18% in Shanghai and 16% in Beijing. (Bloomberg)

Regional

Thomson Reuters: Mideast M&A activities reach $43.4bn in

2013 – According to the Thomson Reuters’ investment banking

analysis for 2013, investment banking fees in the Middle East

reached $722.2mn during 2013. The value of announced M&A

transactions involving any Middle Eastern company reached

$43.4bn during 2013, 7% higher than the $40.7bn witnessed

during 2012, and marking the best full year’s total since 2010.

(Peninsula Qatar)

al Naimi: US shale helps keep oil markets stable – Saudi Oil

Minister Ali al Naimi said the Kingdom welcomes the surge in

US shale oil production for its stabilizing effect on crude prices.

(Qatar Tribune)

Al Rajhi declares SR1,500mn dividends for 2H2013; to raise

its capital by bonus shares – Al Rajhi Bank’s board of

directors has recommended the distribution of dividends worth

SR1,500mn (SR1 per share) for 2H2013, representing 10% of

the face value. Those shareholders who are registered in the

Securities Depository Center on the day of the AGM will be

eligible for these dividends. Meanwhile, Al Rajhi’s board has

also recommended for an increase in the bank’s capital through

bonus shares. The bank’s capital is to be raised by 8% from

SR15,000mn to SR16,250mn. With this, the number of shares

would go up from 1,500mn to 1,625mn shares. The increase will

be done through capitalization of SR1,250mn from account.

(Tadawul)

Budget Saudi to increase its capital through bonus shares –

The United International Transportation Company’s (Budget

Saudi) board has recommended for an increase in company’s

capital through bonus shares issued to its shareholders. The

company’s capital is to be raised by 33.3% from SR305mn to

SR406.7mn. With this, the number of shares would go up from

30.5mn to 40.7mn shares. The increase will be done through

capitalization of SR101.7mn from retained earnings account.

(Tadawul)

ACE gets SAMA’s temporary approval for its insurance

products – Ace Arabia Cooperative Insurance Company (ACE)

has obtained the Saudi Arabian Monetary Agency’s (SAMA)

temporary approval to use its insurance products for six months.

(Tadawul)

Page 4 of 6

5. Nakheel's profit up 27.2% in 2013 – Dubai-based Nakheel has

reported a rise of 27.2% in its net profit to AED2.57bn in 2013.

Revenues grew 20.5% to AED9.4bn in 2013. Meanwhile,

Nakheel’s Chairman Ali Rashid Lootah said the company plans

to launch new projects worth between AED6bn and AED8bn in

2014. Lootah said Nakheel would consider an IPO of shares

after the company settled its debts. (Qatar Tribune)

DLD expects major property growth in Dubai in 2014 –

Property buying activity in Dubai is expected to witness

significant growth in 2014 after registering around 50% jump in

the number of transactions and values in 2013. According to the

data released by the Dubai Land Department (DLD), Dubai’s

ideal environment and safe haven status attracted a large

number of property investors in 2013 as transactions rose by

more than 52% to 63,652 in contrast to 41,767 transactions in

2012. The transaction value also surged by 53% to AED236bn

last year, compared with AED154bn in 2012. Values of property

transactions increased to AED128bn in 2H2013, as against

AED108bn recorded in 1H2013. (GulfBase.com)

Nakheel to build 9 hotels by 2016; plans giant mall off Deira

coast – Nakheel has nine hotel projects under development by

2016 to benefit from the country’s growth as a regional tourist

destination. Nakheel’s Chairman Ali Rashed Lootah said that the

company may unveil plans to build four new hotels on Deira

Island along with its existing one, adding to four other

developments across the rest of Dubai. He said that these

hotels will be part of new projects that Nakheel will unveil in

2014 with a sales value of AED6-8bn, which include homes,

retail and leisure destinations. In addition, Nakheel plans to take

on mega projects, including a 1.5 to 2mn square foot shopping

mall off the Deira coastline and close to the earlier announced

night market. The mall’s dimensions place it among the top

three malls in terms of gross leasable area, just behind the

Dubai Mall and the Mall of the Emirates. (Bloomberg)

DEWA makes progress on AED360mn water pipeline

projects – The Dubai Electricity & Water Authority (DEWA) is

moving forward with its developmental projects to enhance the

power & water infrastructure capacity in Dubai. DEWA has

announced that its AED360mn water pipeline project is

progressing as per schedule. The project envisages supplying,

implementing and extending a water transmission network by 67

kilometers in several areas of Dubai including the Dubai-Al Ain

road, Dubai Bypass Road, Camel Racetrack, and Al Doha

Street. (GulfBase.com)

Empower acquires Palm Utilities at AED1.8bn – Empower

has acquired Palm Utilities, another district cooling service

provider in the UAE, at a value of AED1.8bn. This deal

increases Empower’s market share from 35% to 70%. The

acquisition will be funded through a combination of internal

accruals, equity and debt financing. (Bloomberg)

ACWA Power Barka to expand water desalination capacity –

ACWA Power Barka has concluded the commissioning activities

for its SWRO Desalination Expansion Project and expects to

launch its commercial operations in February 2014. This

expansion will see a further 10 million imperial gallons a day of

water added to its capacity. (MSM)

SMN Power appoints new CEO – SMN Power Holding has

appointed Gillian-Alexandre Huart as the company’s new Chief

Executive Officer effective from January 16, 2014.

(GulfBase.com)

SHC declares 15% dividend for FY2013 – Sahara Hospitality

Company’s (SHC) board of directors has recommended a

dividend of 15% (OMR0.15 per equity share) for FY2013.

(GulfBase.com)

BAC to attract Asian airlines after upgrade – Bahrain Airports

Company (BAC) is in talks with Asian airlines as it seeks to

attract more flight services to its hub that is undergoing an

upgrade worth $980mn. After the upgrade, BAC’s capacity

would double to 13.5mn passengers over five years. BAC’s

CEO Mohamed Yousif Al-Binfalahs said that company is

targeting many carriers from China, India, Indonesia, the

Philippines, Malaysia and Singapore with attractive incentives.

The state-owned company expects to boost passenger numbers

6% in 2014 from 7.4mn in 2013. (Bloomberg)

Saudi-Bahrain rail link faces further delay – Bahrain’s

delayed causeway link with Saudi Arabia, a part of the $15.5bn

GCC Railway Project, may not be completed on time. The

ministries of transport and finance in both Bahrain and Saudi

Arabia are studying the best way to finance and technically

develop the causeway that is part of the 2,177-kilometer (1,353

mile) GCC Railway Project due for completion in 2018. The rail

link between Bahrain and Saudi Arabia will be built parallel to

the existing King Fahd Causeway, which currently brings in five

million visitors to Bahrain annually. (Bloomberg)

IIB acquires $250mn US property – Bahrain-based Islamic

bank, the International Investment Bank (IIB) has acquired a

$250mn, 2,400-unit multi-family residential portfolio primarily

located in Dallas (Texas, US), along with Atlas Residential

Management. The Class A portfolio was acquired from Dallasbased Pillar Income Asset Management. Existing senior debt for

the portfolio, which is insured by the US Department of Housing

& Urban Development, was assumed during the transaction,

with Macquarie Bank providing $71mn in mezzanine financing.

(Bloomberg)

Etihad Airways launches Etihad Regional – Etihad Airways

has launched a new brand, “Etihad Regional”, for travelers in

Europe, in Zurich, Switzerland. Earlier, Etihad had announced

that it was acquiring 33.3% equity in Swiss-based Darwin

Airlines, which will operate Etihad Regional. Their code share

with Etihad Airways started on January 17. Etihad Regional will

offer year-round flights to 15 destinations in Europe using a fleet

of 10 Saab 2000 turboprop aircraft. (Bloomberg)

CBO issues CDs worth OMR377mn – The Central Bank of

Oman (CBO) has issued certificates of deposit (CDs) worth

OMR377mn. The average interest rate of these certificates was

0.13%, while the maximum accepted interest rate was 0.13%.

The tenor of these certificates is 28 days, which will mature on

February 12, 2013. (GulfBase.com)

Page 5 of 6

6. Rebased Performance

Daily Index Performance

170.0

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

138.8

0.4%

0.5%

0.2%

126.0

0.0%

0.0%

S&P Pan Arab

Dec-13

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Euro

Source: Bloomberg

Close ($)

1D%

WTD%

YTD%

Global Indices Performance

Close

1D%

WTD%

YTD%

1,254.05

0.0

0.0

4.0

DJ Industrial

16,458.56

0.0

0.0

(0.7)

20.33

0.0

0.0

4.4

S&P 500

1,838.70

0.0

0.0

(0.5)

106.48

0.0

0.0

(3.9)

NASDAQ 100

4,197.58

0.0

0.0

0.5

4.39

0.0

0.0

1.1

STOXX 600

335.82

0.0

0.0

2.3

137.50

0.0

0.0

8.9

DAX

9,742.96

0.0

0.0

2.0

150.50

0.0

0.0

10.3

FTSE 100

6,829.30

0.0

0.0

1.2

1.35

0.0

0.0

(1.5)

CAC 40

104.32

0.0

0.0

(0.9)

Nikkei

GBP

1.64

0.0

0.0

(0.8)

MSCI EM

CHF

1.10

0.0

0.0

(1.9)

SHANGHAI SE Composite

AUD

0.88

0.0

0.0

(1.5)

USD Index

81.23

0.0

0.0

RUB

33.56

0.0

0.0

BRL

0.43

0.0

0.0

0.6

Yen

Dubai

May-13

Oman

Oct-12

Abu Dhabi

QE Index

Mar-12

Bahrain

Aug-11

Kuwait

Jan-11

(0.0%)

(0.1%)

Qatar

(0.5%)

(0.2%)

Saudi Arabia

Jun-10

0.9%

1.0%

159.4

4,327.50

0.0

0.0

0.7

15,734.46

0.0

0.0

(3.4)

972.27

0.0

0.0

(3.0)

2,004.95

0.0

0.0

(5.2)

HANG SENG

23,133.35

0.0

0.0

(0.7)

1.5

BSE SENSEX

21,063.62

0.0

0.0

(0.5)

2.1

Bovespa

49,181.86

0.0

0.0

(4.5)

1,395.79

0.0

0.0

(3.3)

Source: Bloomberg

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6