VIP Call Girl in Mira Road 💧 9920725232 ( Call Me ) Get A New Crush Everyday ...

Calm in Emerging Markets but Underlying Vulnerabilities Remain

1. Page 1 of 2

Economic Commentary

QNB Economics

economics@qnb.com.qa

April 27, 2014

Calm in Emerging Markets but Underlying Vulnerabilities Remain

Capital flows to emerging markets (EMs)

recovered in February and March 2014 leading

to calmer financial markets. However, the

fundamental weaknesses in specific EM

economies have not been fully addressed,

leaving them exposed to further rounds of

capital outflows, weaker currencies and falling

asset prices. Some EMs are likely to fare better

than others, depending on their underlying

fundamentals and the policy measures they

have taken so far to address their imbalances.

EMs received large amounts of capital inflows

during the period of Quantitative Easing (QE)

following the 2008 global financial crisis. Near-

zero interest rates in advanced economies

drove capital towards higher-yielding EMs.

However, since the announcement in May

2013 by the US Federal Reserve (Fed) of the

gradual reduction of its asset-purchasing

program—the so-called QE tapering—EMs

suffered bouts of capital outflows as yields in

advanced economies rose, leading to weaker

EM currencies, rising yields and falling equity

prices (see our commentary from February,

Emerging Markets Continue to Suffer from QE

Tapering).

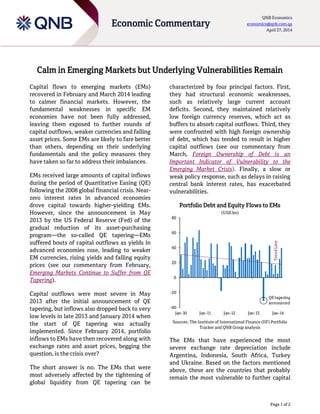

Capital outflows were most severe in May

2013 after the initial announcement of QE

tapering, but inflows also dropped back to very

low levels in late 2013 and January 2014 when

the start of QE tapering was actually

implemented. Since February 2014, portfolio

inflows to EMs have then recovered along with

exchange rates and asset prices, begging the

question, is the crisis over?

The short answer is no. The EMs that were

most adversely affected by the tightening of

global liquidity from QE tapering can be

characterized by four principal factors. First,

they had structural economic weaknesses,

such as relatively large current account

deficits. Second, they maintained relatively

low foreign currency reserves, which act as

buffers to absorb capital outflows. Third, they

were confronted with high foreign ownership

of debt, which has tended to result in higher

capital outflows (see our commentary from

March, Foreign Ownership of Debt is an

Important Indicator of Vulnerability to the

Emerging Market Crisis). Finally, a slow or

weak policy response, such as delays in raising

central bank interest rates, has exacerbated

vulnerabilities.

Portfolio Debt and Equity Flows to EMs

(USD bn)

Sources: The Institute of International Finance (IIF) Portfolio

Tracker and QNB Group analysis

The EMs that have experienced the most

severe exchange rate depreciation include

Argentina, Indonesia, South Africa, Turkey

and Ukraine. Based on the factors mentioned

above, these are the countries that probably

remain the most vulnerable to further capital

-40

-20

0

20

40

60

80

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

TrendLine

QEtapering

announced

2. Page 2 of 2

Economic Commentary

QNB Economics

economics@qnb.com.qa

April 27, 2014

flight. Each had a high current account deficit

in 2013 (3.3% of GDP in Indonesia, 5.8% in

South Africa, 7.9% in Turkey and 9.2% in

Ukraine), with the exception of Argentina

where foreign exchange restrictions kept the

current account deficit near balance. They also

had relatively low foreign exchange reserves

at end-2013 (all below 14% of GDP compared

to an average of 21% in the 16 vulnerable EMs

we analyzed), limiting their capacity to defend

their exchange rates against capital outflows.

Furthermore, foreign ownership of debt is high

(30.0% of total sovereign debt in Argentina,

55.5% in Indonesia, 35.8% in South Africa,

42.7% in Turkey and 46.4% in Ukraine).

Central banks in Argentina, Indonesia, Turkey

and Ukraine have responded. The Argentinian

central bank was forced to raise interest rates

dramatically (up 17 percentage points since

May 2013) as FX reserves evaporated, forcing

a devaluation of the Argentinian Peso in

January 2014. In Indonesia, the policy rate has

been increased by 150 basis points and

Turkey’s repo rate has been increased by 450

basis points. The central bank in South Africa

is pursuing an inflation-targeting mandate and

the official interest rate has only been

increased by 50 basis points so far. Ukraine’s

central bank increased its policy rate by 300

basis points on April 15 to support the

currency, which has weakened by over 30%

since the end of February as its political crisis

intensified.

On the other hand, some EMs have avoided the

worst of the crisis. Brazil has hiked rates 3.5%

since May 2013, helping to support the

currency despite a large current account deficit

(3.6% of GDP) and moderate FX reserves

(17.1% of GDP) at end-2013. In India, skillful

central bank policies helped limit the

weakness of the Indian Rupee through policies

to curb imports and encourage exports. Low

levels of foreign ownership of debt (only 6.3%

of sovereign debt is foreign-owned at end-

2013) also helped insulate the Indian Rupee.

Poland’s exchange rate has been surprisingly

resilient to the crisis, partly due to a relatively

small current account deficit (1.8% of GDP),

moderate international reserves (18.9% of

GDP) and a high share of debt held by

foreigners (49.5% of sovereign debt).

In summary, the fundamental vulnerabilities

amongst selected EMs remain. QE tapering is

expected to continue until late 2014 and is

likely to put further pressure on capital flows

to vulnerable EMs. Additional exchange rate

weakness, higher interest rates, weak growth

and financial market instability can therefore

be expected. Based on the metrics that we

have analyzed, the most vulnerable EMs

appear to be Argentina, Indonesia, South

Africa, Turkey and Ukraine. However, there is

a second tier of EMs that have so far avoided

the worst of the crisis but remain exposed,

including Brazil, India and Poland. Further EM

instability is likely in the months ahead.

Contacts

Joannes Mongardini

Head of Economics

Tel. (+974) 4453-4412

Rory Fyfe

Senior Economist

Tel. (+974) 4453-4643

Ehsan Khoman

Economist

Tel. (+974) 4453-4423

Hamda Al-Thani

Economist

Tel. (+974) 4453-4646

Ziad Daoud

Economist

Tel. (+974) 4453-4642

Disclaimer and Copyright Notice: QNB Group accepts no liability whatsoever for any direct or indirect losses arising from use of this report.

Where an opinion is expressed, unless otherwise provided, it is that of the analyst or author only. Any investment decision should depend

on the individual circumstances of the investor and be based on specifically engaged investment advice. The report is distributed on a

complimentary basis. It may not be reproduced in whole or in part without permission from QNB Group.