2. cant role in making wind energy-as a whole- more cost effective

and viable. A plethora of international programs, partnerships

and alliances along with innovative R&D activities in cooperation

with industry and and academy have helped make wind energy

more sustainable and reliable in terms of power generation and

operability. Looking forward, much of the world has ambitious

plans to expand wind energy development, mainly offshore, that

will require specific R&D and challenges to accomplish. Achieving

these ambitious goals will require strategic collaborations and R&D

funding plans, carefully directed to the topics and mechanisms

most likely to accelerate wind energy deployment.

Increasing the name-plate capacity of wind turbines and their

size, leasing greenfield areas and their deployment on land, and im-

plementing new technologies for reliable performance in offshore

conditions have introduced design, supply chain, procurement

and engineering challenges, networking barriers, and social and

environmental issues that today’s and future researchers should

investigate and solve for the pace of development to continue.

Academic education and training, play and have to play a vi-

tal role in the development and integration of the wind power

industry. Innovation and collaboration are high priorities for every

modern society, and are key factors in its vision to build more

reliable, technical feasible, economic viable and sustainable energy

solutions. Education itself, one of the powerful means to balance

intellectualism and craftsmanship, plays a critical role in the de-

velopment of new methods, tools and mechanisms in wind power

industry.

Previous surveys show that organizations that innovate and

work synergistically are more profitable and have greater business

competitive edge compared with these firms that prefer more

secrecy in their strategic objectives. When an organization or a

firm is working together with researchers from the Academy could:

• develop new ideas, products and services for the market

• get expert advice and access to the latest knowledge, technol-

ogy and equipment

• have access to skilled and work-ready researchers

• gain access to national and international knowledge networks

• lead to new funding schemes and modern research modeling-

surveying - infrastructure

From the other point of view, also the benefits for researchers

working with businesses means the opportunity to:

• contribute to knowledge sharing and value creaation

• produce high quality and relevant research that translates

directly into commercial outcomes

• develop new ideas, products and services for the market

• produce research leading to greater social, economic and en-

vironmental impact

• improve graduate outcomes and effective knowledge transfer

• build valuable contacts and networks

• build a reputation as a world-class research institution open

to business

However, currently (2015), most engineers in Europe’s wind

power industry do not have systematic education background

relating to wind energy. The rapid growth of the huge wind energy

market-especially offshore- drives more and more people to work

in this sector. According the report of the UK’s Royal Academy of

Engineering, research and development should be targeted to the

topics identified by the experts as research prioritizes. The overall

scope of future research is to facilitate the portfolio management

and project development of cost-effective and technical realizable

wind power plants that can be connected to the smart grid, with

the minimum environmental impact.

Research Priorities

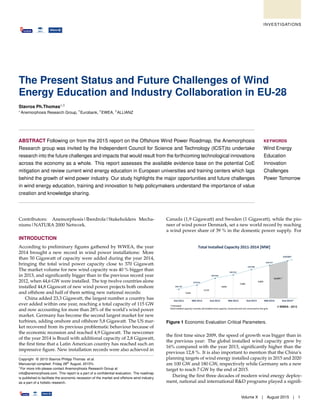

Europe is focusing heavily on offshore wind power development.

Three countries — Germany, Denmark and the United Kingdom,

are spearheading this drive. The European Wind Energy Associ-

ation (EWEA) road-map is projecting that offshore wind power

plants will increase the overall installed capacity to 40-50 GW in

2020 from 6.5 GW in 2013. Various options are being examined to

improve the technology for installing wind turbines. At present,

wind turbines are anchored to the seabed in water depths not

exceeding 30 meters. Research studies and simulation modeling

tests are being conducted on artificial platforms and wind turbines

on floating foundations anchored at depths of up to 60 meters.

To reduce investment costs, researchers are also looking into the

possibility of using existing offshore oil industry’s techniques and

lessons learned. More than 100 research priorities were proposed

from the industry’s experts and the topics of these proposed pri-

orities were divided according to short-tern (0–5 years), mid-term

(5–10 years), or long-term (10–20 years) time scale.

Figure 2 Wind Power Research Priorities.

Despite the fact that the European wind power industry has

been experiencing rapid growth in demand as a result of the con-

secutive incentive policy issued by the central governments there

2 | Stavros Philipp Thomas et al.

3. is a significant gap of the available engineers, scientists and re-

searchers. Education across the Academic institutions and training

centers carries several vital functions including: promotion of

public awareness, development of consumer confidence, training

technical support staff, training of engineers, and training of policy

analysts and development of policies that facilitate the industry as

a whole.

Currently, many engineers and project managers in Europe’s

wind power industry do not have systematic education back-

ground relating to wind energy. EWEA suggests that, every 10 MW

wind power could create 35-45 job opportunities. As of December

2014, installed capacity of wind power in the European Union

totaled 128,751 megawatts (MW). The European Wind Energy As-

sociation estimates that 230 gigawatts (GW) of wind capacity will

be installed in Europe by 2020, consisting of 190 GW onshore and

40 GW offshore.. This means that Europe’s annual new installed

capacity will reach 18,000 MW by 2020 and thus, the wind power

industry will create approximately 50,000 - 60,000 new jobs every

year from 2015 to 2020. For example, Enercon, one of the biggest

wind turbine manufacturer, has planned to recruit more than 1000

graduates from universities between 2015-2020 while Dong Energy,

the largest offshore redeveloper in the world is continuously hiring

wind power experts and graduates and running innovative con-

cepts (Engineer the Future). However, wind power industry faces

the problem of lacking skilled professionals with proper experi-

ences in wind energy. Academies and training centers can offer

systematic and structural knowledge to people to know how to

manage the wind power equipment and identify the associated

risks and uncertainties related to the transportation, installation,

operation and maintenance.

EDUCATION IN ACADEMIC INSTITUTIONS

As the global wind power industry grows in geographic distribu-

tion, project size and complexity, there is a corresponding need

for professionals to lead interdisciplinary wind power projects to

successful completion. The education of wind energy, one of the

most important energy resources, is still a newborn area in Eu-

rope’s education system. However, some universities and colleges

realized the importance of wind energy education for a sustainable

wind power industry and they already offer undergraduate, mas-

ter and doctor programmes. By 23 May 2015, there are almost 100

EU approved Master programs offering colleges and universities

(excluding the independent colleges).

Many of the Academic Institutions offer courses on sustainable

energy-which is a more generic study direction with partial wind

power studies. The courses in renewable energy, such as hydro

energy, thermal and wind are popular for a long time in Danish,

Swedish, Norwegian and int he Netherlands universities including

KTH Royal Institute of Technology at Stockholm, Sweden, Tech-

nical University of Denmark at Lyngby, Aalborg University in

Denamrk, Uppsala University, Chalmers University of Technology

at Gothenburg, Sweden, Delft University of Technology at Delft,

Netherlands, FH Aachen - University of Applied Sciences, the

Swiss Federal Institute of Technology in Zurich (ETHZ) and many

others.

It is also very critical to understand that there are many concerns

because of the shortage of engineers with wind energy education

background. This phenomenon operates as a bottleneck for the de-

velopment and integration of wind energy in Europe and because

of this matter more and more universities provide undergradu-

ate programmes in wind energy. Especially for the universities

locating in the regions which are rich in wind energy potential.

However, the majority of these programs are conducted in their

country of origin language and thus, international applicants could

not follow the study line in these institutions.

Tertiary Education Statistics and Facts

For students studying in European universities , there are two

types of master programmes. One is full-time, another is part-time.

Many graduates choose the latter one in spite of the fact that it

usually needs 3-4 years to finish. The Erasmus programme was

one of the most well-known European programmes and ran for

just over a quarter of a century; in 2014 it was superseded by the

Erasmus+ programme.

In the field of higher education, Erasmus+ gives students and

staff opportunities to develop their skills and boost their employ-

ment prospects. Students can study abroad for up to 12 months

(during each cycle of tertiary education). Around 2 million higher

education students are expected to take part in Erasmus+ dur-

ing the 2014–20 period, including 25 thousand students in joint

masters’ programmes.

The EU-28 had just over 20 million tertiary education students

in 2014 (see Figure 3). Five EU Member States reported 2.0 million

tertiary education students or more in 2014, namely Germany, the

United Kingdom, France, Poland and Spain; tertiary education

student numbers in Italy were just below this level and together

these six countries accounted for two thirds of all EU-28 students

in tertiary education.

Approximately 4.8 million students graduated from tertiary

education establishments in the EU-28 in 2014. An analysis of the

number of graduates by field of education shows that 34.4 % had

studied social sciences, business and law; this share was higher

than the equivalent share (32.8 %) of tertiary education students

still in the process of studying within this field, suggesting that

less students had started this type of study in recent years, or

that either drop-out rates or average course lengths were higher

in other fields. A similar situation was observed for health and

welfare, which made up 15.5 % of graduates from 14.3 % of the

tertiary education student population, as well as the smaller field of

services studies. The reverse situation was observed for the other

fields of education, most notably for engineering, manufacturing

and construction-related studies, humanities and arts, and science,

mathematics and computing.

Across the EU-28, one third (32.8 %) of the students in tertiary

education were studying social sciences, business or law in 2012,

with more female (3.9 million) than male (2.8 million) students in

this field of education, as shown in Figure 4. The second largest

number of students by field of education was in engineering, man-

ufacturing and construction-related studies which accounted for

15.0 % of all students in tertiary education; three quarters of the

students in this field were male. The third largest field of study was

health and welfare, with 14.3 % of all tertiary education students;

close to three quarters of the students in this field were female.

Education in training centers

The shortage of professionals in wind power sector has led to a

rapid increase in demand for wind energy specialists. In Europe’s

wind power industry, most recently graduated engineers are not

well trained on wind energy technologies and application and

there is also a lack of experience in manage and operate wind

power projects. There is therefore an urgent need to develop,

implement and share new training courses that should provide en-

gineers, scientists, technical staff, policy makers, owners, operators

and planners constructive knowledge. Some training centers offer

Volume X August 2015 | This is a part of a confidential work | 3

4. Figure 3 Students in tertiary education, by field of education and sex, EU-28, 2015.

Figure 4 Graduates from tertiary education, by field of education, EU-28, 2015.

4 | Stavros Philipp Thomas et al.

5. professionals short-term mid-career training on the topics such

as wind resource assessment (RISO DTU) system design (Danish

Wind Power Academy), risks management (DNV GL) mainte-

nance, installation, etc. They offer on-the-job training as well as the

conventional face-to-face training in wind energy for people who

are not willing to quit job to study for several years as full-time

students.

Table bellow summarises opportunities to future wind energy

projects because of the knowledge and experience received in

training centers. Much of the opportunity to drive down costs is

perceived to be in the design and performance of wind turbines,

O&M strategies and manufacturing innovations anticipated to

help reduce the cost of wind energy.

STRUCTURAL RESEARCH NEEDS TO ACCELERATE

WIND ENERGY DEVELOPMENT

Research and development has a vital role to play if the potential of

wind energy is to be fully exploited. Policy metrics, a set of reliable

and cost effective regulations, efficient IEC standards should con-

tribute to faster deployment and integration. However, investment

in wind power R&D will not be delivered by market signals alone;

extensive support at the national and international levels is needed

to accelerate the development of wind energy technologies and

facilitate the implementation of innovative solutions.

At the I E A’s 35th meeting of experts regarding the Long term

R&D needs for the wind energy industry in Stockholm, Sweden

a wind power investor and developer mentioned: "There is a

consensus on the view that there still is a need for generic long-term

research. The main goal for research is to support the implementation

of national/international visions for wind energy in the near and far

future. It was the opinion that it is possible to reach this goal for the near

future with available knowledge and technology. However, large-scale

implementation of wind energy requires a continued cost reduction and

an improved acceptability and reliability. In order to achieve a 10 to 20%

part of the worldwide energy consumption provided by wind, major steps

have to be taken. The technology of turbines, of wind power stations, of

grid connection and grid control, the social acceptability and the economy

of wind power in a liberalized market, all have to be improved in order

to provide a reliable and sustainable contribution to the energy supply.

It is for this objective that there is a need for long- term R&D. Besides

that, there is also a need for a short-to mid-term research that mainly is

in the interest of utilities/manufacturing industries and to some extent to

society.

It is true, that during the last ten years, R&D has put emphasis

on developing larger and more reliable in terms of quality and

availability wind turbine systems utilising knowledge developed

from national and international R&D programs. Thus, continued

research is a fundamental component for the overall Cost of En-

ergy mitigation and technology improvement. Continued R&D

will support the design and implementation of new proposals

and mechanisms-tools as well as incremental improvements. Re-

searchers around the globe investigate the aspects and impacts

of extreme wind phenomena, aerodynamics, load effects, electri-

cal generation, supply chain and procurement excellence. This

research has resulted in larger and more sophisticated machines,

improved component performance, optimized supply chain and

accessibility structure and reduced O&M costs.

However, significant opportunities remain to reduce wind

power plant LCOE and increase further the deployment of wind

energy. Exploiting these opportunities will require multi-year

research programs and strong collaborations between research in-

stitutions and industry from many countries to study how a wind

power plant system performs as a whole, and to optimise the per-

formance and cost associated with the operation and maintenance.

In the first years of R&D, research academies and universities

produced more knowledge than the industry could handle. Re-

search was mainly aimed at applying existing knowledge to the

field of wind energy. Nowadays, automatic portfolio management

systems and offshore applications produce more uncertainties and

risks than the researchers can solve with current knowledge. Fu-

ture research should be conducted to address the specific problems

related to wind engineering technology.

TECHNOLOGY CHALLENGES

Nowadays, offshore wind turbines installed generally in the range

between 3 and 5 MW although prototypes of power up to 7 MW

and even higher are currently tested (Only a few months after its

sales launch at the EWEA Offshore trade show in Copenhagen,

the new Siemens offshore flagship wind turbine of the type SWT-

7.0-154 has now been installed as a prototype), indicating the man-

ufacturing trends concerning future wind turbines operating in

maritime environments. On top of that, wind farms’ total capacity

has increased as well. Before 2000, average wind farm size was

below 20 MW. Today, the experience has grown significantly so

that many countries are building large (average size of projects

exceeds 150 MW), utility-scale offshore wind farms or at least have

plans to do so.

Nevertheless, the vast majority of the existing large-scale com-

mercial projects still use shallow-water technology (located at less

than 30 m water depth) although the idea of going deeper is gradu-

ally moving closer towards implementation. Actually, the average

water depth remains below 20 m, (excluding the first full scale

floating wind turbine (Hywind) which was installed in 2009 off the

Norwegian coast at a water depth of 220 m. On the other hand, the

average distance from shore ten years ago was below 5 km, while

today is close to 30 km—confirming that offshore wind turbines

are installed increasingly away from the shores.

A. Production

Another important input parameter in the economic viability of

the project is the expected power production. As sufficient wind

speeds and capacity factor at the project site are the main drivers

of wind energy production and of wind park revenues, the un-

derstanding and forecast of wind become essential. Therefore, a

lot of effort must be put into assessing the wind energy resource

at the given project site with the highest prediction accuracy and

by taking into consideration the reliable numbers for the capacity

factors.

In general, actual capacity factors for onshore wind farms oscil-

late across time and regions, with an average value being between

20 and 30%. For instance, the average European value between

2003 and 2009 has been recorded at about 21%. The highest values

have been recorded for Greece and the UK (i.e. equal to 29.3%

and 26%, respectively) due to the existence of many low density

population areas which benefit of high wind speeds and enable

the siting of wind farms.

On the other hand, offshore sites may have the ability to demon-

strate quite higher capacity factors than onshore counterparts (as a

result of the higher mean power coefficient which is usually met

in offshore installations), typically ranging from 20% to 40%. One

may see that capacity factor values, in some cases, even reached

50%, however, this is not the rule since there are cases where the

recorded capacity factor may be quite low mainly as a result of the

Volume X August 2015 | This is a part of a confidential work | 5

6. I Table 1 Risk-consequence illustration for wind energy projects

Possible risk factors Consequence Proposed Solution

The resourcing constraints of manufacturers. The lack of experienced staff could risk the

quality of manufacture and testing.

Third-party inspection services during manu-

facture and inspection will help meet specifi-

cations and deadlines.

Equipment survival in offshore environments. Equipment might have a reduced life span. Operation and Maintenance metrologies and

Strategic improvements .

Lack of experience of offshore structures

(fixed or floating) and foundations

There is a danger of over or under design,

leading to unplanned project costs or even

failure.

Staff training and critical thinking improvement

via experiences.

New designs are required, for example in-

creased turbine size or device prototype.

The lack of experienced staff could risk design

quality.

Testing of components, including turbine

blades and converters improvements through

research and testing.

combination of extended downtimes due to several system failures

and the tough conditions usually met in marine environments.

The traditional approach for gathering wind data is to construct

a meteorological mast equipped with anemometers. However, in

the offshore environment this practice is both difficult and expen-

sive to implement. Nowadays, a plethora of devices is available.

WINDCUBE and FLidar, the floating LiDAR technology are just

between the most famous innovative solutions to these problems.

FLiDAR can measure wind at turbine hub-height and provide

accurate and reliable data on wind speed, wind direction, and

turbulence. Additional sensors can be integrated onto the buoy to

achieve a full environmental assessment of the location.

Figure 5 Wind distribution assumption and turbine choice

B. AEP Uncertainty Estimation

Model uncertainty relates to the uncertainty of the parameters

estimated based on the wind study. Consequently, while wind

studies are often based on very complex models, there is a risk that

they contain estimation errors, such as measurement errors and/or

model errors. Measurement errors include that measured wind

characteristics may not be correct due to for example dysfunctional

measurement instruments or incorrect calibration of these. Model

errors for example relate to the risk that measured historical wind

conditions are not representative of the future wind conditions.

Furthermore, the wind study may be wrong with respect to

assessing the effect a turbine has on the turbine specific production

of the turbine behind it, which is called wake effects. The size of the

wake effects is affected by factors such as wind speed, wind density,

turbulence and distance between turbines, meaning that wake

effects may be larger when the wind is coming from a direction in

which turbines are located closer to each other. We consider model

uncertainty as a static uncertainty, which means that it is fixed over

time. This implies that if the wind study has underestimated the

true wind average speed or wake effects for the first operational

year, it will be underestimated in all years. Consequently, taking

wind study uncertainty into account, we reach static P75 and P90

measures that are fixed over the life of the project.

At figure 5, we illustrate how different P measures are affected

by how wind variability is taken into account (whether wind vari-

ability is averaged or not). The blue line illustrates production

uncertainty when all production uncertainty is considered on an

average basis, while the green line illustrates production uncer-

tainty when wind variability is based on short-term uncertainty.

Figure 6 AEP and Uncertainty. The graph is based on a 2.3MW

turbine

C. Technical Availability and Accessibility

The technical availability of a wind turbine depends, among others,

on: The technological status (experience gain effect throughout

the years) of the installation at the time it went online (increasing

experience in both production and operation issues in the offshore

sector suggests that the failure rate decreases and the reliability

increases respectively). The technical availability changes (aging

effect) during the installation’s operational life.

The accessibility difficulties (accessibility effect) of the wind

farm under investigation. This parameter is, as aforementioned,

of special interest for offshore wind parks, especially during win-

ter, due to bad weather conditions (high winds and huge waves

suspend the ship departure, thus preventing maintenance and

6 | Stavros Philipp Thomas et al.

7. repair of the existing wind turbines). Nowadays, contemporary

land-based wind turbines and wind farms reach availability levels

of 98% or even more (Kaldellis, 2002, 2004; Harman et al., 2008)

but, once these wind turbines are placed offshore the accessibility

may be significantly restricted, thus causing a considerable impact

to the availability of the wind farm and in turn to the energy and

economic performance of the whole project.

This is not always the case however; apart from the distance

from the shore, the accessibility to a wind farm’s installation site

depends also on several other parameters such as local climate

conditions and the type and availability of the maintenance strat-

egy adopted (the limited size of some wind farms does not always

justify the purchase of a purpose built vessel so there may be

significant delays if the vessel is, for example, away for another

assignment). Thus, there are cases where the impact may be more

or less significant than the expected one.

A case with low recorded availability is North Hoyle offshore

wind farm, which is located in the UK, at an average distance from

the shore equal to 8 km (see also Table 3 where recorded availability

data for several wind farms are presented). As it is mentioned in

(BERR, 2005), the availability of this wind farm during a one-year

period (2004–2005) was recorded equal to 84The most notable

sources of unplanned maintenance and downtime have occurred

due to termination of cable burial and rock dumping activities

as well as high-voltage cable and generator faults. It is worth

mentioning that the downtime recorded splits to 66% owed to

turbine failure, 12% to construction activities, 5% to scheduled

maintenance and 17% to site inaccessibility due to harsh weather

conditions.

Another example with even lower availability (67%) is the case

of Barrow offshore wind farm (see also Table 1), also located about

8 km far from shore, in the UK. The total average availability of

this project is quoted as 67% for one-year period between July 2006

and June 2007. This low availability is due to a number of wind

turbine faults, mainly generator bearings and rotor cable faults

combined with low access to the site because of high waves during

that time period.

EDUCATION AND R&D CHALLEGES

Currently, public and private universities are the fundamental

force of knowledge creation and value sharing in wind energy

education. The number of training centers is still small in South

Eastern countries compare to the Scandinavian countries but the

overall number is small in relation to the increasing demand of

wind power industry. The main weakness of university education

is that the programmes usually take longer time and lack of enough

flexibility while some others offer generic studies programs with

no strong directions in wind energy applications.

Undergraduate programmes need four years (English Lan-

guage lessons are offered by a very small number), Masters two

years and doctoral programme need at least three years. The re-

sults show that the industry may not afford to wait for years until

students get their degree and leave their campus. Consequently,

almost every company hires a number of recent graduated employ-

ees without proper education background or experience. These

new employees should also have the opportunity to take further

training in specific topics of wind energy to be able to meet the

challenges of every day tasks.

A lot of companies also expect their employees can get some

regular short-term courses every year but the limited number of

wind energy training centers in EU are in huge demand by the

wind power industry. According to the EWEA, the number of

jobs in the sector is expected to increase to 520,000 by the end

of the decade, a rise of 200% from the number of jobs currently

available in the market, and 24,000 more jobs than predicted in

a 2009 EWA report. Most of these jobs should require expertise

wind energy education background. It is a huge market drive for

training centers and Academies. Obviously the number of wind

energy training centers and courses offered is inadequate and they

should be further expanded and strengthened to meet the new

demands.

Engineering and technology are covered in most of EU-28 wind

energy education. There is little number of degrees about wind

power policies, planning, economics, industry structure, risks iden-

tification and management, environmental impact and protection,

supply chain and procurement excellence. Almost all of those

EU universities which offer wind energy education can deliver

wind energy courses only on wind engineering and science. Train-

ing centers only provide skill training courses for technicians and

engineers and thus, it is necessary to layer this gap as soon as

possible.

Almost all of the wind energy education and training in EU

requires participants attending to campus. It creates a dramatic

dilemma for people who might want to change their career path,

because they usually would like to know more on wind power

before making decision. They are considering to enter this new

area but not willing to change their jobs in a rush. In this case,

Distance Learning courses is an excellent tool for teaching persons

off campus however, this type of education courses should not

be considered among the most effective ways to get a systematic

wind energy education-knowledge.

CONCLUSIONS

There is a shortage of qualified professionals in EU wind power in-

dustry, such as policy analysts, procurement specialists, scientists,

researchers, and engineers.

The lack of new people with wind power knowledge is an issue

currently, and will be even more a problematic aspect so in the

future, as the proportion of development, operation, maintenance,

procurement, supply chain and risks management jobs will grow

in the wind industry. To circumvent these chaotic phenomenon,

this article recommends introducing industry experience into train-

ing and education, thus mitigating the theoretical knowledge and

optimizing the technical experience. Industry and academic insti-

tutions could jointly fund research projects, develop engagement

platforms, industrial scholarships opportunities and doctoral pro-

grams.

In addition, a muti-directional and polysynthetic framework

is needed to coordinate the synergies between industry and

academia, to harmonize vocational education and training, estab-

lish an effective Intellectual Property Rights Strategy and increase

open innovation. By taking these strategic steps and establish-

ing that the European wind energy industry has access to a well

trained, critical thinking and creative workforce, wind energy will

be able to continue to play a fundamental role in the transition to

a renewable and sustainable energy system and last but not least,

boost economic growth and create hundreds of thousands of jobs.

Volume X August 2015 | This is a part of a confidential work | 7

8. I Table 2 Risk-consequence illustration for wind energy projects

Possible risk factors Consequence Proposed Solution

The resourcing constraints of manufacturers. The lack of experienced staff could risk the

quality of manufacture and testing.

Third-party inspection services during manu-

facture and inspection will help meet specifi-

cations and deadlines.

Equipment survival in offshore environments. Equipment might have a reduced life span. Operation and Maintenance metrologies and

Strategic improvements .

Lack of experience of offshore structures

(fixed or floating) and foundations

There is a danger of over or under design,

leading to unplanned project costs or even

failure.

Staff training and critical thinking improvement

via experiences.

New designs are required, for example in-

creased turbine size or device prototype.

The lack of experienced staff could risk design

quality.

Testing of components, including turbine

blades and converters improvements through

research and testing.

I Table 3 Roadmap Strategic Approach

Key Themes Issues Addressed Wind Vision Study Scenario Roadmap Action Areas*

Collaboration to reduce wind

costs through wind technology

capital and operating cost reduc-

tions, increased energy capture,

improved reliability, and develop-

ment of planning and operating

practices for cost effective wind

integration.

Continuing declines in wind

power costs and improved reliabil-

ity are needed to improve market

competition with other electricity

sources.

Levelized cost of electricity reduc-

tion trajectory of 24% by 2020,

33% by 2030, and 37% by 2050

for land-based wind power tech-

nology and 22% by 2020, 43% by

2030, and 51% by 2050 for off-

shore wind power technology to

substantially reduce or eliminate

the near- and mid-term incremen-

tal costs of the Study Scenario.

• Wind Power Resources and Site

Characterization • Wind Plant

Technology Advancement • Sup-

ply Chain, Manufacturing, and

Logistics • Wind Power Perfor-

mance, Reliability, and Safety •

Wind Electricity Delivery and In-

tegration • Wind Siting and Per-

mitting • Collaboration, Education,

and Outreach • Workforce Devel-

opment • Policy Analysis

Collaboration to increase market

access to U.S. wind resources

through improved power system

flexibility and transmission expan-

sion, technology development,

streamlined siting and permitting

processes, and environmental

and competing use research and

impact mitigation.

Continued reduction of deploy-

ment barriers as well as en-

hanced mitigation strategies to re-

sponsibly improve market access

to remote, low wind speed, off-

shore, and environmentally sensi-

tive locations.

Capture the enduring value of

wind power by analyzing job

growth opportunities, evaluating

existing and proposed policies,

and disseminating credible infor-

mation.

• Supply Chain, Manufacturing,

and Logistics • Collaboration, Ed-

ucation, and Outreach • Work-

force Development • Policy Anal-

ysis

Levelized cost of electricity reduc-

tion trajectory of 24% by 2020,

33% by 2030, and 37% by 2050

for land-based wind power tech-

nology and 22% by 2020, 43% by

2030, and 51% by 2050 for off-

shore wind power technology to

substantially reduce or eliminate

the near- and mid-term incremen-

tal costs of the Study Scenario

Wind deployment sufficient to en-

able national wind electricity gen-

eration shares of 1020% by 2030,

and 35% by 2050.

A sustainable and competitive re-

gional and local wind industry

supporting substantial domestic

employment. Public benefits from

reduced emissions and consumer

energy cost savings.

Wind Power Resources and Site

Characterization • Wind Plant

Technology Advancement • Sup-

ply Chain, Manufacturing, and Lo-

gistics • Wind Electricity Delivery

and Integration • Wind Siting and

Permitting • Collaboration, Educa-

tion, and Outreach • Policy Analy-

sis

8 | Stavros Philipp Thomas et al.