cushman & wakefield the economy cre and investment ideas -

ClearPath Investment Perspectives - Nov 17 2014

1. Brendan Connaughton

Chief Investment Officer

Phone: (415) 682-6894

brendan@clearpathcapital.com

ClearPath Investment Perspectives

November 17, 2014

ClearPath

US Economic Scenarios

Avg. Recovery

10%

Subpar

60%

Stagflation

30%

Severe

0%

Economic & Market 2014 Full Yr. Full Yr. 2013 Q1 Q2 Q3 Q4 2014 2015

Global GDP (Yr./Yr.%)

3.20%

3.15%

3.25%

3.50%

3.75%

3.60%

4.10%

Global CPI (Yr./Yr.%)

1.75%

1.75%

2.00%

2.00%

2.15%

1.90%

2.25%

US GDP (Yr./Yr.%)

1.9%

-2.90%

4.6%

3.50%

3.00%

2.65%

2.90%

US CPI % (Yr./Yr.%)

1.5%

2.00%

1.60%

1.73%

1.90%

1.80%

2.00%

Fed Funds

0.1%

0.1%

0.1%

0.1%

0.1%

0.1%

0.25%

10 yr. Treas.

2.35%

3.03%

2.53%

2.52%

3.00%

3.10%

3.55%

Consensus Forecasts

Capital Market Data (using ETF data as of 11/14/14)

Index Last 5 Last Tot. Rt. Tot. Rt. NTM NTM TTM

Days Month YTD TTM P/E Earnings Yield P/B DIV%

MSCI AW

0.05%

5.13%

3.47%

5.39%

14.63x

6.83%

2.17x

1.49%

S&P 500

0.44%

7.21%

12.35%

16.27%

15.88x

6.29%

2.78x

1.98%

DJIA

0.39%

7.61%

8.58%

13.66%

15.01x

6.66%

3.04x

2.12%

NASDAQ

1.23%

8.22%

13.43%

19.43%

19.57x

5.10%

3.29x

1.21%

Russell 2000

0.08%

6.33%

1.99%

6.99%

21.38x

4.67%

2.20x

1.31%

MSCI EAFE

0.88%

3.43%

- 2.55%

0.39%

14.03x

7.12%

1.62x

3.08%

MSCI EM

0.34%

0.39%

1.42%

2.67%

10.99x

9.09%

1.49x

2.76%

Last Last Last

Index Price 5 Days Month YTD

London Gold

$1,185.70

2.56%

- 4.82%

- 1.81%

West Tex Oil

$ 75.46

- 2.12%

- 7.92%

- 18.81%

DJUBS Com

$ 21.56

- 0.78%

- 2.51%

- 16.00%

US / EUR

$ 1.2452

- 0.25%

- 2.23%

- 10.07%

US / Yen

$ 116.68

0.00%

9.86%

10.99%

0.03%

0.06%

0.12%

0.51%

0.95%

1.60%

2.01%

2.32%

2.76%

3.04%

0.17%

0.28%

0.30%

0.90%

1.48%

2.06%

2.59%

3.12%

3.87%

4.17%

0.04%

0.14%

0.17%

0.57%

0.95%

1.34%

1.79%

2.24%

3.33%

3.60%

0.06%

0.22%

0.26%

0.88%

1.47%

2.06%

2.75%

3.44%

5.12%

5.54%

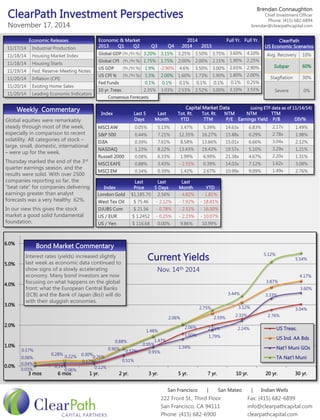

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

3 mos

6 mos

1 yr.

2 yr.

3 yr.

5 yr.

7 yr.

10 yr.

20 yr.

30 yr.

US Treas.

US Ind. AA Bds

Nat'l Muni GOs

TA Nat'l Muni

Current Yields

Nov. 14th 2014

Weekly Commentary

Global equities were remarkably steady through most of the week, especially in comparison to recent volatility. All categories of stock – large, small, domestic, international – were up for the week.

Thursday marked the end of the 3rd quarter earnings season, and the results were solid. With over 2500 companies reporting so far, the “beat rate” for companies delivering earnings greater than analyst forecasts was a very healthy 62%.

In our view this gives the stock market a good solid fundamental foundation.

Bond Market Commentary

Interest rates (yields) increased slightly last week as economic data continued to show signs of a slowly accelerating economy. Many bond investors are now focusing on what happens on the global front: what the European Central Banks (ECB) and the Bank of Japan (BoJ) will do with their sluggish economies.

222 Front St., Third Floor

San Francisco, CA 94111

Phone: (415) 682-6900

Fax: (415) 682-6899

info@clearpathcapital.com

clearpathcapital.com

San Francisco | San Mateo | Indian Wells

Economic Releases

11/17/14

Industrial Production

11/18/14

Housing Market Index

11/18/14

Housing Starts

11/19/14

Fed. Reserve Meeting Notes

11/20/14

Inflation (CPI)

11/20/14

Existing Home Sales

11/20/14

Leading Economic Indicators

2. Brendan Connaughton

Chief Investment Officer

Phone: (415) 682-6894

brendan@clearpathcapital.com

222 Front St., Third Floor

San Francisco, CA 94111

Phone: (415) 682-6900

Fax: (415) 682-6899

info@clearpathcapital.com

clearpathcapital.com

San Francisco | San Mateo | Indian Wells

Economic Commentary

Data released last week showed that US Retail Sales rose 0.3% in October – a tiny bit stronger than the consensus forecast had anticipated. As expected, the recent

decline in the price of gasoline weighed on sales at service stations, which

fell 1.5% in October, but drove sales in other areas.

The falling price of gasoline is an incredibly powerful element. If gasoline prices remain at these lower levels for the next 12 months, the gain for the average US household would be an increase of $700 worth of purchasing power over the coming year.

ClearPath Investment Perspectives

November 17, 2014

Retail Sales

Where the Stock Market is… and how we got here…

S&P 500 Index: daily close from 10/9/2007 to Present

3. Brendan Connaughton

Chief Investment Officer

Phone: (415) 682-6894

brendan@clearpathcapital.com

222 Front St., Third Floor

San Francisco, CA 94111

Phone: (415) 682-6900

Fax: (415) 682-6899

info@clearpathcapital.com

clearpathcapital.com

San Francisco | San Mateo | Indian Wells

ClearPath Investment Perspectives

November 17, 2014

Odds and Ends…

Company Commentary

We recently held an exclusive client event at the Telsa Factory in Fremont. Because of some of our relationships, we are able to have our clients get a private tour of the factory and test drive cars on the Telsa test track. In that vein, I have reviewed the stock for some of the attendees.

Telsa Corp. designs, manufactures and sells high-performance electric cars. We are long-term bullish on Telsa – it’s a great way to invest in Elon Musk, Telsa’s visionary and innovative founder. The company’s Q3 earnings were solid, but the stock is still under its 50-day moving average. The stock has a great potential to run up to the $300 range.

Market Commentary

The market action between Sept. 18 to Oct. 15 was historic in nature. We saw dramatic sell-off in all “risk” assets, and the subsequent run is in “safe” assets.

What has been very encouraging for us is the coordination – or lack of correlations – of the two major groups. The action in the stock and bond markets has been very orderly over the last month. This gives us confidence that nothing is “broken.” The pullback we experienced was natural and, frankly, good for the long-term growth of the markets.

Market Commentary

One of the biggest surprises for almost all investors this year was the fall in interest rates. Using the US 10- yr. as a proxy for the overall bond market, the return thus far this year has been about 5.75%. This is in a year in which just about everyone thought you would lose money in bonds this year.

Jan. Feb. Mar. Apr. May Jun. Jul. Aug. Sep. Oct. Nov.

1700

1750

1800

1850

1900

1950

2000

2050

1%

2%

3%

3½%

-8%

+11%

US 10-yr. Treasury %

S&P 500 Index

2014 thru 11/14…

Important to remember that as interest rates go down – bond prices go up. The move inversely to each other.

Bollinger Bands- A band plotted 2 standard deviations away from the 50-day moving average,

200-day moving avg.

50-day moving avg.

4. Brendan Connaughton

Chief Investment Officer

Phone: (415) 682-6894

brendan@clearpathcapital.com

This publication is produced by ClearPath Capital Partners. The information & opinions herein are for general information use only. ClearPath does not guarantee the accuracy or completeness, nor does ClearPath assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Information & opinions are subject to change without notice, are for general information only & are not intended as an offer or solicitation with respect to the purchase or sales of any security or as personalized investment advice. No assurance can be given that any forecast or target can be achieved. Forecasts are based on assumptions, estimates, opinions & hypothetical models which may prove to be incorrect. Past performance is not indicative of future returns & does not guarantee of future results. Research obtained by unaffiliated 3rd party sources deemed reliable by ClearPath, however, ClearPath does not guarantee accuracy & completeness, & makes no warranties with respect to this data.

ClearPath Investment Perspectives

November 17, 2014

The Retail Sales… and the US Consumer…

An easy way to view or understand the

US economy is to break it down into

what moves or drives economic growth. In general terms, there are three main drivers to the US economy: government spending, corporate spending and consumer spending. The unscientific way to view this breakdown is one-third corporate/government spending and two-thirds US consumer spending. Of course it’s not just this simple, but this is a good way to start an analysis.

With that in mind, the US Consumer is an incredibly resilient economic entity. Moreover, much of what we spend as consumers is on things we must have: toothpaste, gas, groceries, etc. Consumer spending on the margin (that 5-10% of extra spending) makes the real difference for our economy and in overall economic growth.

Retail sales numbers were solid in October. Lower gasoline prices should translate into stronger spending in the future. The US Consumer – the most powerful economic force in the world – will continue to help drive our economy forward over the next 12 months or more.