Financial institution 1st assignment

•Télécharger en tant que DOCX, PDF•

1 j'aime•1,814 vues

Top 10 Questions of FI Muhammad Danish | www.knowledgedep.blogspot.com

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (20)

Similaire à Financial institution 1st assignment

Similaire à Financial institution 1st assignment (20)

Plus de Danish Saqi

Plus de Danish Saqi (19)

Dernier

Dernier (20)

Financial institution 1st assignment

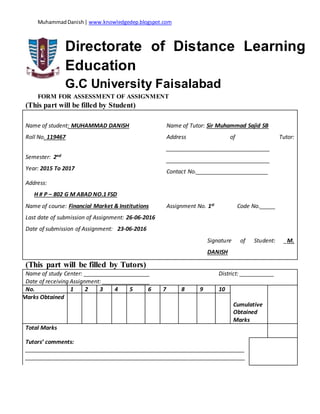

- 1. MuhammadDanish| www.knowledgedep.blogspot.com Directorate of Distance Learning Education G.C University Faisalabad FORM FOR ASSESSMENT OF ASSIGNMENT (This part will be filled by Student) Name of student: MUHAMMAD DANISH Name of Tutor: Sir Muhammad Sajid SB Roll No. 119467 Address of Tutor: _________________________________ _________________________________ Contact No._______________________ Semester: 2nd Year: 2015 To 2017 Address: H # P – 802 G M ABAD NO.1 FSD Name of course: Financial Market & Institutions Assignment No. 1st Code No._____ Last date of submission of Assignment: 26-06-2016 Date of submission of Assignment: 23-06-2016 Signature of Student: _M. DANISH (This part will be filled by Tutors) Name of study Center: _____________________ District: ___________ Date of receiving Assignment: _______________ No. 1 2 3 4 5 6 7 8 9 10 Cumulative Obtained Marks Marks Obtained Total Marks Tutors’ comments: ______________________________________________________________________ ______________________________________________________________________

- 2. MuhammadDanish| www.knowledgedep.blogspot.com Date of Assignment Return: _________ Signature of Tutor Q1: Why are financial markets important to the health of the economy? Explain financial system; write short notes on different components of the financial system? Answer: FinancialMarkets: A Financial market is a market in which people trade financial securities, commodities, and other fungible items of value at low transaction costs and at prices that reflect supply and demand. Securities include stocks and bonds, and commodities include precious metals or agricultural products. The importance of financial markets to the health of economy: Financial markets are extremely important to the general health of an economy. With effective markets for credit and capital, borrowing and investment will be limited and the whole macro – economy can suffer. Financial Crises A financial crisis is a situation in which the value of financial institutions or assets drops rapidly. A financial crisis is often associated with a panic or a run on the banks, in which investors sell off assets or withdraw money from savings accounts with the expectation that the value of those assets will drop if they remain at a financial institution. Debt Markets and Interest Rates A security is a claim on the issuer’s future income or assets. A bond is a debt security that promises to make payments periodically for a specified period of time.1 Debt markets, also often referred to generically as the bond market, are especially important to economic activity because they enable corporations and governments to borrow in order to finance their activities; the bond market is also where interest rates are determined. An interest rate is the cost of borrowing or the price paid for the rental of funds (usually expressed as a percentage of the rental of $100 per year). There are many

- 3. MuhammadDanish| www.knowledgedep.blogspot.com interest rates in the economy—mortgage interest rates, car loan rates, and interest rates on many different types of bonds. Mortgage markets: The mortgage market involves making long – term loans for buying property. Once a loan is made, it can be traded on the second-hand mortgage market. Like the stock exchange, the secondary mortgage market enables the original lenders, the banks, and building societies, to regain lost liquidity. The new owner of the mortgage debt is entitled to receive the mortgage repayments. Managing Risk in FinancialInstitutions In recent years, the economic environment has become an increasingly risky place. Interest rates have fluctuated wildly, stock markets have crashed both here and abroad, speculative crises have occurred in the foreign exchange markets, and failures of financial institutions have reached levels unprecedented since the Great Depression. To avoid wild swings in profitability (and even possibly failure) resulting from this environment, financial institutions must be concerned with how to cope with increased risk. Financialsystem: The processes and procedures used by an organization’s management to exercise financial control and accountability. These measures include recording, verification, and timely reporting of transactions that affect revenues, expenditures, assets, and liabilities. Basic components of financial system: There are five basic components of financial system: 1. Financialinstitutions: A financial institution (F1) is an establishment that focuses on dealing with financial transactions, such as investment, loans and deposit. Conventionally, financial institutions are composed of organizations such as banks, trust companies, insurance companies and investment dealers. 2. Financialmarkets: A financial market is the place where financial assets are creating. It can be broadly categorized into money markets and capital markets. Money

- 4. MuhammadDanish| www.knowledgedep.blogspot.com market handles short – term financial assets (less than a year) whereas capital markets take care of those financial assets that have maturity period of more than a year. The key functions re: 1. Assist in creation and allocation of credit and liquidity. 2. Serve as intermediaries for mobilization of savings. 3. Help achieve balanced economic growth 4. Offer financial convenience. One more classification is possible: primary markets and secondary markets. Primary markets handle new issue of securities in contrast secondary markets take care of securities that are presently available in the stock markets. 3. Financialinstruments: This is an important component of financial system. The products, which trade in a financial market, are financial assets, securities or other type of financial instruments. There is a wide range of securities in the markets since the needs of investors and credit seekers are different. They indicate a claim on the settlement of principal down the road or payment of a regular amount by means of interest or dividend. Equity shares, debentures, bonds, etc. are some example. 4. Financialservices: Financial services consist of services provided by assets management and liability management companies. They help to get the necessary funds and make sure that they are efficiently deploying. They assist to determine the financing combination and extend their professional services up to the stage of servicing of lenders. They help with borrowing, selling and purchasing securities, lending and investing, making and allowing payments and settlements and taking care of risk exposures in financial markets. These range from the leasing companies, mutual fund house, merchant bankers, portfolio managers, bill discounting and acceptance houses. The financial services sector offers a merchant banking, depositoryservices, bookbuilding, etc. 5. Money:

- 5. MuhammadDanish| www.knowledgedep.blogspot.com The money is anything that accepted for payment of product and services or for the repayment of debt. It is a medium of exchange and acts as a store of value. Q2: What is money and its different functions? Briefly, explain how money evolved in Pakistan? Answer: Money: The money is anything that accepted for payment of products and services or for the repayment of debt. It is a medium of exchange and acts as a store of value. Functions of money: There are two types of functions of money. 1. Primary functions: Primary functions include the most important of money, which it must perform in every country, these are: a) Medium of exchange: Money, as a medium of exchange, means that it can be used to make payments of all transactions of goods and services. It is the most essential function of money. Money has the quality of general acceptability. So; all exchanges take place in terms of money. This function has removed the major difficulty of lack of double co – incidence of wants and inconveniences associated with the barter system. Use of money allow purchase and sale to be conducted independently of one another. This function of money facilitates trade and helps in conducting transactions in an economy. Money has no power to satisfy human wants, but it commands power to purchase those things, which have utility to satisfy human wants. b) Measure ofvalue (unit of value): Money as measure of value means that money works as common denomination, in which values of all goods and services are expressing.

- 6. MuhammadDanish| www.knowledgedep.blogspot.com By reducing the value of all goods and services to a single unit (i.e. price), it becomes very easy to find out the exchange ratios between them and comparing their prices. This function facilitates maintenance of business accounts, which would be otherwise impossible. Money helps in calculating relative prices of goods and services. Due to this reason, it is regarded as a unit of account’. For instance, ‘Rupee’ is the unit of account in India, ‘Pound’ in England and so on. 2. SecondaryFunctions: These refer to those functions of money, which are supplementary to the primary functions. These functions derive from primary functions and, therefore, they are known as ‘Derivative Functions’. The major secondary functions are: 1) Standard of deferred payments: Money as a standard of deferred payments means that money acts as a ‘Standard’ for payments, which are to be made in future. Every day, millions of transactions take place in which payments doses not made immediately. Money encourages such transactions and helps in capital formation and economic development of the economy. This function of money is significant because. Money as a standard of deferred payments has simplified the borrowing and lending operations. It has led to the creation of financial institutions. 2) Store of value (Assetfunction of money): Money as a store of value means that money can be used to transfer purchasing power from present to future. Money is a way to store wealth. Although wealth can be store in other forms also, but money is the most economical and convenient way. It provides security to individuals to meet contingencies, unpredictable emergencies and to pay future debts. Money as store of value has the following advantages: The money working in Pakistan The money is working in Pakistan with different shapes, which are following:

- 7. MuhammadDanish| www.knowledgedep.blogspot.com 1. Commodity money: It is the simplest kind of money, which is use in barter system where the valuable resources fulfill the functions of money. The value of this kind of money comes from the value of resource use for the purpose. It is only limited by the scarcity of the resources. Value of this kind of money involves the parties associated with the exchange process. 2. Fiat money: The word fiat means the” command of the sovereign”. Fiat currency is the kind of money, which does not have any intrinsic value, and it cannot converter into valuable resource. The value of fiat money determines by government order, which makes it a legal instrument for all transaction purposes. The fiat money need to be controller as it may affect entire economy of a country if it is misused. Ex: Paper money, coins. 3. Fiduciary money: Today’s monetary system is highly fiduciary. Whenever, any bank assures the customers to pay in different types of money and when the customer can sell the promise or transfer it to somebody else, it is called the fiduciary money, fiduciary money generally paid in gold, silver or paper money, there are cheques and bank notes, which are the examples of fiduciary money because both are some kind of token, which are used as money and carry the same value. 4. Commercialbank money: Commercial bank money or demand deposits are claims against financial institutions that can be used for the purchase of goods and services. A demand deposit account is an account from which funds can be withdrawn at any time by cheque or cash withdrawal without giving the bank of financial institution any prior notice. Banks have the legal obligation to return funds held in demand deposits immediately upon demand (or ‘at call’). Demand deposit withdrawals can be performed in person, via cheques or bank drafts, using automatic teller machines (ATMs), or through online banking. There are also various other types of money like the credit money, electronic money, coin and paper money, fractional money and Representative money as discussed below: a) Fractionalmoney:

- 8. MuhammadDanish| www.knowledgedep.blogspot.com It is a hybrid type of money, which is partly back by a commodity and has fiat money transaction purpose. If the commodity loses its value then fractional money converts into fiat money. b) Representative money: It represents a claim on commodity and it can be redeem for that commodity at a bank. A token or paper money can be exchange for a fixed quantity of commodity. Its value depends on the commodity it backs. c) Coins: Metals of particular weight are stamp into coins. There are various precious metals like gold, bronze, copper whose coins already have used in human history. The minting of coins is control by the state. d) Papermoney: Paper money don’t have any intrinsic value, as a fiat money. It is approved by government order to be treat as legal tender through which value exchange can happen. Government prints the paper according to the requirements, which is tightly control as it can affect the economy of the country. <=======================================>

- 9. MuhammadDanish| www.knowledgedep.blogspot.com Q3: What are different roles and functions of central bank to support financial system of any country? Answer: Central bank: It every country, there is one bank, which acts as the leader of the money market- supervising, controlling and regulating the activities of commercial banks and other financial institutions. It acts as a banker of issue and is in close touch with the government, as banker, agent and adviser to the latter. Such a bank is known as the Central Bank of the country. Roles & Functions of a central Bank 1. Bank of issue: Central bank has the exclusive monopoly of note issue and the currency notes issued by the central bank are declared unlimited legal tender throughout the county. This monopoly brings about: Uniformity of note issue which in turn facilitates trade and exchange within the country Enables the central bank to influence and control the credit creation of commercial banks Gives distinctive prestige to the currency notes Enables govt to appropriate partly or fully the profits of note issue. 2. Banker, Agent and Adviser to the Government: As banker and agent, RBI keeps the banking accounts of the central, state governments, makes, and receives payments on behalf of the government. It provides short – term advances to the govt. (ways and means advances) to tide over temporary shortage of funds. It advises the govt. on all monetary and banking matters. 3. Custodian of the cask reserves of commercialbank: All commercial banks keep part of their deposits as reserves with the central banks and hence the name Reserve bank of India. Centralized cash reserves serve as the basis of a larger and more elastic credit structure and

- 10. MuhammadDanish| www.knowledgedep.blogspot.com helps commercial banks to meet crises and emergencies. Centralized cash reserve aids the central bank to control credit creation and implement monetary policy. 4. Custodian of foreign balance of the country: RBI holds the foreign exchange assets of all commercial and non – commercial bank of the country. It is the responsibility of RBI to maintain the rate exchange and manage exchange control and other restrictions imposed by the state. It also maintains reserves with the IMF and obtains normal drawing and special drawing rights. 5. Lender of the lastresort: Central bank never refuses to accommodate any eligible commercial bank experiencing cash shortage. In the absence of a central bank, commercial banks will have to carry substantial cash reserves, which imply restricted lending and responsibility of meeting directly or indirectly all reasonable demands for accommodation by the commercial banks. 6. Central clearance,settlementtransfer: As the central bank keeps cash reserves of commercial banks, it is easier for member banks to settle their mutual claims in the books of the central bank. These are the clearing house operations of RBI wherein cheques are cleared, claims settled and funds transferred in the books of the member banks. However, this function can also be performed by any leading bank in a locality or area. 7. Controller of credit: Central bank controls the level of credit in the economy by either expanding or contracting bank deposits. In modern times, bank deposits have become the most important source of money in the county. As controller of credit, it seeks to influence and control the volume of bank credit and to stabilize business conditions in the country. 8. Open market operations: Deliberate and direct buying of securities and bills by the central bank in the money market, on its own initiative, is called open market operations. In periods of inflation, the central bank will sell in the market first calls bills in its possession to buyers like commercial banks and others. This reduces the cash reserves of the commercial banks, which in turn will reduce its capability to give loans and advances. Thereby, business activity in the

- 11. MuhammadDanish| www.knowledgedep.blogspot.com country will be cut short. During recession, central banks buys bill from commercial bank and thereby increases their cash reserves. 9. Cashreserve ratio: According to the central bank, every scheduled bank has an obligation to maintain a certain portion of their demand and time deposits as a reserve with the central bank. This provision was fixed for three important reasons; To ensure the liquidity and solvency of individual commercial bank and of the banking system as a whole To provide the central bank with supply of deposits for local operations To influence and ultimately restrict commercial banks’ expansion of credit. Hence, CRR is an additional instrument of credit controlof the central bank 10.Selective creditcontrols: The quantitative controls like bank rate, OMO and CRR affect indiscriminately all sections of the economy which depend on bank credit. Besides, there are some groups of borrowers who are engaged in important spheres of economic activity and whom the central bank would like to insulate from these quantitative effects. hence, central banks have been adopting the tool of selective credit controls or qualitative controls whose special features are: They distinguish between essential and non – essential uses of bank credit Only non – essential uses are brought under the scope of central bank controls They affect not only the lenders but also the borrowers. 11.Working of bank rate policy: Hence, rise in bank rate increases interest rates, curtails bank credit, decreases demand for gods and services and finally reduces the price level. Further, the most powerful influence of bank rate is psychological – bankers and business men consider bank rate changes as authoritative pronouncements of the central bank concerning the credit situations. at a very important time. Radcliffe report states:” the rise in the bank rate is symbolical; it is evident that authorities have the determination to take unpleasant steps to check inflation”.

- 12. MuhammadDanish| www.knowledgedep.blogspot.com <=======================================> Q 4: Describe money market and briefly discus instruments of money markets with examples from Pakistanimarkets? Answer: Money market: The money market became a component of the financial markets for assets involved in short – term borrowing, lending, buying and selling with original maturities of one year or less. Trading in money markets is done over the counter and is wholesale. A segment of the financial market in which financial instruments with high liquidity and very short maturities are trade. Participants use the money market as a means for borrowing and lending loans in the short term, from several days to just under a year. Instruments of money markets: 1. Certificate of deposit: A certificate of deposit (CD) is a savings certificate entitling the bearer to receive interest. A CD bears a maturity date, a specified fixed interest rate and can be issue in any denomination. CDs are generally issue by commercial banks and are insure by the FDIC. 2. Repurchase agreements: A repurchase agreement (repo) is a form of short – term borrowing for dealers in government securities. The dealer sells the government securities to investors, usually on an overnight basis, and buys them back the following day. 3. Commercialpaper: Commercial paper is an unsecured, short - term debt instrument issued by a corporation, typically for the financing of accounts receivable, inventories and meeting short – term liabilities. Maturities on commercial papers rarely range any longer than 270 days. 4. Federalagencyshort – term securities:

- 13. MuhammadDanish| www.knowledgedep.blogspot.com In the Pakistan, short – term securities issued by government sponsored enterprises such as the farm credit system, the federal home loan banks and the federal national mortgage association. 5. Federalfunds: In the Pakistan, interest – bearing deposits held by banks and other depository institutions at the federal reserve; these are immediately available funds that institutions borrow or lend, usually on an overnight basis. They are lent for the federal funds rate. 6. Municipal notes: In the Pakistan, short – term notes issued by municipalities of tax receipts of other revenues. 7. Treasurybills: Short – term debt obligations of a national government that are issue to mature in three to twelve months. 8. Money funds: Pool short – maturity, high – quality investments that buy money market securities on behalf of retail or institutional investors. 9. Foreignexchange swaps: Exchanging a set of currencies in spot date and the reversal of the exchange of currencies at a predetermined time in the future 10.Asset– backedsecurities: An asset – backed security (ABS) is a security whose income payments and hence value is derived from and collateralized (or “backed”) by a specified pool of underlying assets. The pool of assets is typically a group of small and illiquid assets, which are unable to be sold individually <=======================================>

- 14. MuhammadDanish| www.knowledgedep.blogspot.com Q5: Briefly explain different types of stock. What are different intermediaries involved in stock markets? Answer: Types of stock: There are two types of stock: a) Common stock b) Preferred stock a) Common stock: A common stock is a security that represents ownership in a corporation. Holders of common stock exercise control by electing a board of directors and voting on corporate policy. Common stockholders are on the bottom of the priority ladder for ownership structure. b) Preferredstock: A preferred stock is a class of ownership in a corporation that has a higher claim on its assets and earnings than common stock. Preferred shares generally have a dividend that must be paid out before dividends to common shareholders, and the shares usually do not carry voting rights. Intermediaries involved in stock market 1. Insurance companies Insurance companies concentrate on fulfilling the insurance needs of the community, both for life and non-life and non-life insurance. These companies offer products that allow investors to select the kind of policies to suit their financial planning needs. These companies also offer policies for funding a child’s education and marriage, and providing a steady income for the aged through annuities and pensions. 2. Mutual funs Mutual funds (MFs) organizations satisfy the needs of individual’s investors through pooling resources from a large number with similar investments goals and risks appetite. The resource collected are invested in the capital and money

- 15. MuhammadDanish| www.knowledgedep.blogspot.com market securities. The returns are distributed to investors optimizing the return for the investors. 3. Non-banking finance companies NBFCs are commonly known as finance companies and are corporate bodies, which concentrate mainly on lending activities in a well-defined area. 4. Investment brokers The main duty of investment brokers is to transact the security sales. There are discount brokers and full – service brokers. They provide an opportunity online for some individuals to promote their trades. Aside from that, they can also solicit valuable investment advice to some clients who may need it that time. 5. Investment bankers The main duty of this financial intermediary is to increase monetary amounts of companies through stocks and bonds. Since conducting stock offerings and issuing bonds is so expensive, investment bankers focuses on how they can help the firm to earn more capital. 6. Escrow companies This is the type of financial intermediary that is built for the very purpose. These companies’ acts like an unconcerned party that will hold instructions for execution as well as the grounds agreed for it. 7. Pensionfund A pension fund is any plan, funds, or scheme which provides retirement income. Pension funds are important to shareholders of listed and private companies. They are especially important to the stock market where large institutional investors dominate. 8. Collective investment scheme A collective investment scheme is a way of investing money alongside other investors in order to befit from the inherent advantages of working as part of a group. These advantages include an ability to hire a professional investment manage, which theoretically offer the prospects of better returns and / or risk management. Benefit from economies of scale – cost sharing among others diversifies more than would be feasible for most individual investors which, theoretically, reduce risk.

- 16. MuhammadDanish| www.knowledgedep.blogspot.com <=======================================> Q 6: Explain functions of stock market and procedure of trading stock in stock market also differentiates between KSF 100 – index and KSF 30 indexes. Answer: Stock market: The stock is the market shares of publicly held companies are issue and trade through exchange or over – the – counter market, the stock market also known as the equity market. Trading procedure on a stock market: The trading procedure involves the following steps: 1. Selectionofa broker: The buying and selling of securities can only be done through SEBI registered brokers who are members of the stock exchange. The broker can be an individual, partnership firm or corporate bodies. So, the first step is to select a broker who will buy/sell securities on behalf of the investor or speculator. 2. Opening demat accountwith depository: Demat (dematerialized) account refer to an account which a citizen must open with the depository participant (bank or stockbrokers) to trade in listed securities in electronic form. Second step in trading procedure is to open a demat account. The securities are held in the electronic form by a depository. Depository is an institution or an organization are which holds securities (e.g. shares, debentures, bonds, mutual (National securities depository Ltd.) and CDSL (central depository services Ltd.) there is no direct contact between depository and investor. Depository participant will maintain securities account balances of investor and intimate investor about the status of their holdings from time to time.

- 17. MuhammadDanish| www.knowledgedep.blogspot.com 3. Placing the order: After opening the demat account, the investor can place the order. The order can be placed to the broker either (DP) personally or through phone, email, etc. Investor must place the order very clearly specifying the range of price at which securities can be bought or sold. E.g. “buy 100 equity shares of reliance for not more than Rs 500 per share”. 4. Executing the order: As per the instructions of the investor, the broker executes the order i.e. the buys or sells the securities. Broker prepares a contract note for the order executed. The contract note contains the name and the price of securities, name of parties and brokerage (commission) charged by him. Contract nonet is signed by the broker. 5. Settlement: This means actual transfer of securities. This is the last stage in the trading of securities done by the broker on behalf of their clients. There can be two types of settlement. a) On the spot settlement: In means settlement is done immediately and on spot settlement follow. T + 2 rolling settlement. This means any trade – trade – taking place on Monday gets settled by Wednesday. b) Forwardsettlement: It means settlement will take place on some future date. It can be T+ 5 or T + 7, etc. All trading in stock exchanges takes place between 9.55 am and 3.3. Pm. Monday to Friday.

- 18. MuhammadDanish| www.knowledgedep.blogspot.com Difference betweenKSF 100 & KSF 30: KSE 100 The KSE 100 index was introduced in 1991 and comprises of 100 companies selected on the basis of sector representation and highest market capitalization, which captures over 80% of the total market capitalization of the companies listed on the Exchange. KSE 100 index is a stock index acting as a benchmark to compare prices on the Karachi Stock Exchange over a period. KSE 30 The Karachi Stock Exchange is maintaining two indices, which are in place i.e. KSE 100 and KSE all share index. Both the said indices are market capitalization based indices. The Karachi Stock Exchange has launched the KSE 30 index with base value of 10,000 points, formally implemented from Friday, September 1, 2006. KSE 30 index is based only on the free float of shares, rather than because of paid up capital. When a company announces a dividend, KSE 30 index is adjusted for dividends and right shares. <=======================================>

- 19. MuhammadDanish| www.knowledgedep.blogspot.com Q7: Explain in detail bonds, bonds market and different types of bonds; also write a note on Pakistaninvestment bonds (PIB). Answer: Bonds: Bonds are a debt investment in which an investor loans money to an entity (typically cooperate or government) which borrows the funds a defined period of time at a variable or fixed interest rate. Bonds markets: The bond market (also debt market or credit market) is a financial market where participants can issue new debt, known as the primary market, or buy and sell debt securities, known as the secondary market. This is usually in the form of bonds, butit may include notes, bills, and so on. Types of bonds: 1. Treasurybonds: Treasuries are issued by the federal government to finance its gadget deficits. Because they’re backed by Uncle Sam’s awesome taxing authority, they’re considered credit – risk free. The downside: their yields are always going to be lowest (except for tax – free munis). But in economic downturns they perform better than higher – yielding bonds, and the interest is exempt from state income taxes. 2. Agency bonds: These bonds are issued by federal agencies, they’re different from the mortgage – backed securities issued by those same agencies, and by Freddie Mac (FRF) (the Federal home loan mortgage cop.) agency yields are higher than treasury yields because they are not full – faith - and – credit obligations of the U.S. government, but the credit risk is considered minimal. Interest on the bonds is taxable at both the federal and state levels, however.

- 20. MuhammadDanish| www.knowledgedep.blogspot.com 3. Investment – grade corporate bonds: Investment – grade corporate is issued by companies or financing vehicles with relatively strong balance sheets. The carry ratings of at least triple – B from standard & poor’s, Moody’s investors service or both. (The scale is triple – A as the highest, followed by double – A, single – A, then triple – B, and so on.) for investment – grade bonds, the risk of default is considered pretty remote. Still, their yields are higher than either Treasury or agency bonds, though like most agencies they are fully taxable. In economic downturns, these bonds tend to underperform Treasuries and agencies. 4. High – yield bonds These bonds are issue by companies or financing vehicles with relatively weak balance sheets. They carry ratings below triple – B. default is a distinct possibility. As a result, high – yield bond prices are more closely tie to the health of corporate balance sheets. They track stock prices more closely than investment – grade bond prices. “High – yield doesn’t provide the same asset – allocation benefits you get by mixing high – grade bonds and stock, “observes Charles Schwab chief investment officer Steve ward. 5. Foreignbonds: These securities are something else altogether. Some are dollar – denominated, but the average foreign bond fund has about a third of its assets in foreign – currency – denominated debt, according to Lipper. With foreign – currency – denominated bond, the issuer promises to make fixed interest payments – and to return the principal – in another currency. The size of those payments when they are converted into dollars depends on exchange rates. 6. Mortgage – backedbonds Mortgage – backed, which have a face value of $25,000 compared to &1,000 or &5,000 for other types of bonds, involve “prepayment risk.” Because their value drops when the rate of mortgage prepayments rises, they don’tbenefit from declining interest rates like most other bonds do. 7. Municipal bonds: Municipal bonds are issued by governments or their agencies, and they come in both the investment – grade and high – yield varieties. The interest is tax – free, but that doesn’t mean everyone can benefit from them. Taxable yields are higher than muni yield to compensate investors for the

- 21. MuhammadDanish| www.knowledgedep.blogspot.com taxes, so depending on your bracket; you might still come out ahead with taxable bonds. Pakistan investment bonds: Pakistan investment bonds are issued by SBP on the behalf of federal government. These are long – term securities and benchmark for long tenure debt. These are risk free debts. Interbank/ NBFIs transfer of PIBs is permissible. PIBs issued in five tenures: 3 years, 5 years, 10-year, 15 years, 20years, 30 years maturity. SBP, SECP & ministry of finance announce the coupon retest and the target consulting each other and profit is paid semiannually. SBP is acting as an agent on behalf of the government for raising short term and long – term funds from the market. Primary dealer maintains a subsidiary general ledger account (SGLA) with SBP for the settlement pure – pose. The PIBs are sold by SBP to ten approved primary dealers through multiple prices sealed bids auction. The commission is paid to primary dealers on sale proceeds of Pakistan investment bonds (PIBs) @ 0.5% on amount of bid accepted or 3.5% of the target amount whichever is less. The commission is paid to primary dealers by debiting the government non – food account and credit the amount to the respective bank’s account. <=======================================>

- 22. MuhammadDanish| www.knowledgedep.blogspot.com Q8: What are different determinants of interest rates and its impact on valuation of securities? Answer: Determinants of interest rates: 1) Inflation rate: The result is that consumers have more money to spend, causing the economy to grow and inflation to increase. The opposite holds true for rising interest rates. As interest rates are increased, consumers tend to have less money to spend. With less spending, the economy slows and inflation decreases. 2) The real interestrates: The real interest rate is the rate of interest an investor, saver or lender receives (or expects to receive) after allowing for inflation. It can be described more formally by the fisher equation, which states that the real interest rate is approximately the nominal interest rate minus the inflation rate. Example: One-year T – bill rate in 2015 was 4.53% and inflation for the year was 2.80%. if investors expected the same inflation rate, the according to the fisher effect the real interest rate for 2015; 4.53% - 2.80% = 1.73% If one – year T – bill rate was 1.89% while the inflation rate was 3.30%. the real rate; 1.89% - 3.30% = -1.41% 3) Default (credit) risk: A credit risk is the risk of default on a debt that may arise from a borrower failing to make required payments. In the first resort, the risk is that of the lender and includes lost principal and interest, disruption to cash flow, and increased collection costs. Bond rating agencies. Example: 10 – year Treasury interest rate was 4.70%. Danish rated corporate debt interest was 5.58% and Ijaz rated corporatedebt interest rate was 6.70%. Average DRP: DRP Danish = 5.58% - 4.70% = 0.88%

- 23. MuhammadDanish| www.knowledgedep.blogspot.com DRP Ijaz = 6.70% - 4.70% = 2% 4) Liquidity risk: Liquidity risk is the risk that a company or bank may be unable to meet short term financial demands. This usually occurs due to the inability to convert a security or hard asset to cash without a loss of capital and/or income in the process. 5) Specialprevisions and covenants: Such as taxability, convertibility and culpability affect the interest rates. As special provisions that provide benefits to the security holder increases, interest rate decreases. 6) Term to maturity: Term structure of interest rates (yield curve) maturity premium (MP) is the difference between the long and short – term securities of the same characteristics except maturity. Yield curve: relationship btw YTM and time to maturity. Yield may rise with maturity (up – ward sloping yield curve: the most common yield curve) Yields may fall with maturity (Inverted or downward sloping yield curve) Flat yield curve: Yields are unaffected by the time to maturity Ij = (IP, RIR, DRPj, LRPj, SCPj, MPj) <=======================================>

- 24. MuhammadDanish| www.knowledgedep.blogspot.com Q9: Explain foreign exchange marketand its participants? Answer: Foreignexchange market: The foreign exchange market (forex, FX, or currency market) is a global decentralized market for the trading of currencies. This includes all aspects of buying, selling and exchanging currencies at current or determined prices. In terms of volume of trading, it is by far the largest market in the world. Types of participants: 1) The interbank or wholesalemarket: Major Forex Trading in the wholesale forex market is undertaken by banks – popularly known as interbank market. In this market, banks and non – bank financial institutions transact with each other. They undertake trading on behalf of customers, but majority of trading is undertaken for their own account by proprietary desks. 2) Foreignexchange dealers and brokers: Dealers: banks and some non – blank financial institutions act as foreign exchange dealer. These dealers quote both “bid” and “ask” for a particular currency pair (for spot, forward and swap contracts) and take opposite side to either buyer or sellers of currency. They make profit from the spreads between buying and selling prices i.e. Bid and ask rate. Brokers are agents, which merely match buyers and sellers and get a brokerage fee. Brokers: brokers on the other hand, help clients to get a better rate on the currency trade by making available different quotes offered by dealers. Traders can compare rats accordingly take a decision. Brokers charge a commission for providing these services. 3) Hedger, speculators and arbitrageurs: Traders buying and selling foreign exchange can take the role of hedgers, or speculators or arbitrageurs. Hedgers are traders who undertake forex trading because they have assists or liability in foreign currency. For example, when an importer requiring foreign

- 25. MuhammadDanish| www.knowledgedep.blogspot.com currency, sells domestic currency to buy foreign currency, he is termed as a hedger. The importer has a foreign currency liability. Similarly, an exporter sells foreign currency and buys domestic currency is hedger. Speculators are traders who essentially buy and sell foreign currency to make profit from the expected futures movement of the currency. These traders do not have any genuine requirement for trading foreign currency. They do not hold any cashposition in the currency. Arbitrageurs buy and sell the same currency at two different markets whenever there is prices discrepancy. The principal of “law of one price” governs the arbitrage principle. Arbitrageurs ensure that market prices move to rational or normal levels. With the proliferation on internet, cross currency, cross currency arbitrage possibility has increased significantly. 4) Central banks and treasuries: All most all central bank and treasuries participate in the forex market. Central banks play very important role in foreign exchange market. However, these banks do not undertake significant volume of trading. Each central bank has official/unofficial target of the forex rate of its home currency. If the actual price deviates from the target rate, the central banks intervene in the market to set a time. 5) Retailmarket: In the retail market, individuals (tourists, foreign students, patients traveling to other countries for medical treatment) small companies, small exporters and importers operate. Money transfer companies/remittance companies (for example like western union) are also major players in the retail market. Retail traders buy/sell currency for their genuine business/personal requirements. For example, an exporter enters into forward contract to convert foreign currency to domestic currency. A tourist buys foreign currency in the spot market before undertaking the journey. A UK patient visiting India to undertake an operation that would have costhim a fortune at UK <=======================================>

- 26. MuhammadDanish| www.knowledgedep.blogspot.com Q10: Explain determinants of exchange rate and financial instruments of foreign exchange market? Answer: Determinants of exchange rate: 1. Inflation rates Changes in market inflation cause changes in currency exchange rates. A country with a lower inflation rate than another is will see an appreciation in the value of its currency. The prices of goods and services increase at a slower rate where the inflation is low. A country with a consistently lower inflation rate exhibits a rising currency value while a country with higher inflation typically sees depreciation in its currency and is usually accompanied by higher interest rates. 2. Interest rates Changes in interest affect currency value and dollar exchange rate. Forex rates, interest rates, and inflation are all correlated. Increases in interest rates cause a country’s currency to appreciate because higher interest rates provide higher rates to lenders, thereby attracting more foreign capital, which causes a rise in exchange rates. 3. Country’s current account/balance ofpayments A country’s current account reflects balance of trade and earnings on foreign investment. It consists of total number of transactions including its exports, imports, debt, etc. a deficit in current account due to spending more of its currency on importing products than it is earning through sale of exports causes depreciation. Balance of payments fluctuates exchange rate of its domestic currency. 4. Government debt Government debt is public debt or national debt owned by the central government. A country with government debt is less likely to acquire foreign capital, leading to inflation. Foreign investors will sell their bonds in the open market if the market predicts government debt within a certain country. As a result, a decrease in the value of its exchange rate will follow.

- 27. MuhammadDanish| www.knowledgedep.blogspot.com 5. Terms of trade Related to current account and balance of payments, the terms of trade are the ratio of export prices to import prices. A country’s terms of trade improve if its exports prices rise at a greater rate than its imports prices. This results in higher revenue, which causes a higher demand for the country’s currency and an increase in its currency’s value. This results in an appreciation of exchange rate. 6. Politicalstability & performance A country’s political state and economic performance can affect its currency strength. A country with less risk for political turmoil is more attractive to foreign investors, as a result, drawing investment away from other countries with more political and economic stability. Increase in foreign capital, in turn, leads to an appreciation in the value of its domestic currency. A country with sound financial and trade policy does not give any room for uncertainty in value of its currency. But, a county prone to political confusions may see depreciation in exchange rates 7. Recession When a country experiences a recession, its interest rates are likely to fall, decreasing its chances to acquire foreign capital. As a result, its currency weakens in comparison to that of other countries, therefore lowering the exchange rate. 8. Speculation If a county’s currency value is expected to rise, investors will demand more of that currency in order to make a profit in the near future. As a result, the value of the currency will rise due to the increase in demand. With this increase in currency value comes a rise in the exchange rate as well. Financialinstruments of foreignexchange market? There are six instruments of foreign exchange market? 1) Exchange – traded fund

- 28. MuhammadDanish| www.knowledgedep.blogspot.com If referred to as ETF’s. These are open – ended investment companies that have the characteristic of being traded at any time throughout the day. These will oftentimes attempt duplicating stock market indices such as the S&P 500. The ETF’s gain strength as the United States dollar (USD) weakens against a different currency and therefore replicate currency market investment. Certain funds can track the price fluctuations of the various world currencies as they compare to the USD, and will oftentimes increase in value to counter the direction that the USD moves in. this crease increased interest in the USD for investors and speculators. 2) Forward: The agreement established between two parties wherein they purchase, sell, or trade an asset at a pre – agreed upon price is called a forward or a forward contract. Normally, there is no exchange of money until a pre – established future date has been arrived at. Forwards are normally performed as a hedging instrument used to either deter or alleviate risk in the investment activity. 3) Future: A forward transaction that contains standard contract sizes and maturity dates are considered futures. Futures are traded on exchanges that have been created for that purpose exclusively. Just like with commodity markets, a future in the forex market normally designates a contract length of 3 months in duration. Interest amounts are also included in a futures contract. 4) Option Commonly shortened to FX option from foreign exchange option. Options are derivatives (financial instruments whose values fluctuate based on underlying variable) wherein the owner has the right to, but is not necessarily obligated to, exchange on currency for another at a pre – agreed upon rate and a specified date. When you talk about options in any form (stock market, forex, or any other market), the forex market is the deepest and largest, as well as the liquid market of any options in the world 5) Spot:

- 29. MuhammadDanish| www.knowledgedep.blogspot.com Where futures normally employ a 3 – month timeframe, spot transactions encompass a 48 – hour delivery transaction period. There are four characteristics that all spottransactions have in common, namely: a) A direct exchange between two currencies b) Involves only cash, never contracts c) No interest is included in the agreed upon transaction d) Shortest of all transaction timeframes 6) Swaps Currency swaps are the most common type of forward transactions. A swap is a trade between two parties wherein they exchange currencies for a pre – determined length of time. The transaction then is reversed at a pre – agreed upon future date. Currency swaps can be negotiated to mature up to 30 years in the future, and involve the swapping of the principle amount. Interest rates are no “netted” since they are denominated in different currencies. <=======================================>