Recommandé

Contenu connexe

Tendances

Tendances (20)

Similaire à Profit and Loss, Balance Sheets and RATIO ANALYSIS

Similaire à Profit and Loss, Balance Sheets and RATIO ANALYSIS (20)

Plus de Patrick Rubix

Plus de Patrick Rubix (20)

Dernier

Dernier (20)

Profit and Loss, Balance Sheets and RATIO ANALYSIS

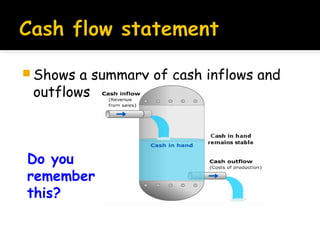

- 1. Shows a summary of cash inflows and outflows Do you remember this?

- 2. Year 11

- 3. Investors Workers Lenders of money e.g. banks Inland Revenue Users of Financial Info. Competitors – all limited companies must publish their accounts

- 5. Shows the flow of sales and costs over a period of time, usually a year, and the level of profits or losses made as a result of trading.

- 6. The trading account shows the difference between the cost of goods sold and the sales revenue. The difference is known as gross profit.

- 7. The profit and loss account begins with the gross profit from the trading account. Any other income is added to the gross profit. Then all other expenses (overheads) are subtracted, to give net Profit.

- 8. Sales Less cost of sales = Gross profit Less expenses = Net profit

- 9. Pete runs a takeaway pizza parlour in Mexborough. He has been trading for 12 months and is drawing up his profit and loss account. How will he work out how much money he has taken over the 12 months? Sales = price x number sold

- 10. Pete’s takings are as follows; 6,000 x pizzas at £7 each. 42,000 10,000 x chips at £1.50 each 15,000 8,000 x garlic bread at £4 each 32,000 What is his sales figure? £89,000

- 11. Next we need to work out how much it has cost him to buy his raw materials to make these goods. Cost of goods sold = opening stock + purchases – closing stock Has Pete any opening stock?

- 12. Pete’s purchases are as follows; Prepared dough 2,000 packets £6,000 at £3 each Frozen chips 280 boxes at £10 £2,800 each Toppings and tomato base £1200 £1,200 £ 600 Sundries £600 TOTAL = £10,600

- 13. What is Pete’s gross profit? Gross profit = sales – COGS 89,000 – 10,600 = £78,400.

- 14. What else will we have to take off Pete’s profit figure? Overheads / expenses – the general costs of running the business. For example.....

- 15. Pete’s expenses are as follows; Wages £10,000 Telephone £ 3,000 Rent £12,000 Utilities £ 5,000 Advertising £ 2,500 TOTAL EXPENSES ? Insurance £ 1,000 Vehicle £ 5,000 £38,500

- 16. So, what is Pete’s net profit? Net profit = GP – expenses NP = 78,400 – 38,500 = £39,900

- 17. Cost of goods sold is also stated as cost of sale Sales

- 18. Profit and Loss Account for Pete's Pizza Parlour 2010 Sales Cost of Goods Sold Gross Profit Less Expenses Wages Rent Advertising Insurance Vehicles Telephone Utilities Net Profit $ 10,000 12,000 2,500 1,000 5,000 3,000 5,000 $ 89,000 10,600 78,400 38,500 39,900

- 19. Sales (Turnover) Cost of Sales Gross Profit Less expenses Wages Insurance Rates Rent Telephone Advertising Depreciation IT Light and heat Net Profit Mr Reading's Burger Bar £OOO Opening Stock Purchases Less Closing Stock 40 120 160 30 £OOO 50 2 11 30 11 4 5 3 2 300 130 170 118 52

- 20. Mr Reading's Burger Bar Plc 2007 £OOO £OOO Sales (Turnover) 300 Cost of Sales Opening Stock 40 Purchases 120 160 Less Closing Stock 30 130 Gross Profit 170 Less expenses 118 Net Profit 52 Corporation Tax 12 Profit After Tax 40 Divends paid 15 Retained profit carried forward 25 £OOO 30 145 175 2008 £OOO 350 35 140 210 mbnj 135 75 17 58 20 28

- 22. The Balance Sheet shows the value of a business’s assets and liabilities at a particular time. This lets managers/owners know how much their business is worth. Before we can complete a balance sheet you must know some key terms.

- 23. Assets:- Are items of value which is owned by the business. Assets are broken down into two categories. Fixed Assets:- Are likely to be kept by the business for more than one year. EG. Premises, vehicles, equipment.

- 24. Current Assets:- Are assets that are held for a short period of time. E.G. Cash, Stock, Debtors (people who owe you money) Liabilities:- Are items owed by the business. Again liabilities are broken down into to kinds.

- 25. Long-Term Liabilities:- Anything that business has to pay back after one year. E.G Loans Current Liabilities:- Are amounts owed by the business which have to be paid within one year. E.G Overdraft, Creditors (people you owe money to).

- 26. If the value of assets are greater than liabilities, then the business is said to be wealthy. Business’s would like to see this increase every year. To calculate the Owner’s Wealth (Shareholders fund) we use this equation. Total Assets-Total liabilities=Owner’s Wealth

- 27. Fixed Assets Property Machinery Vehicles Current Assets Stock Debtors Cash Current Liabilities Creditors Unpaid Tax Net Current Assets (Working Capital) Net Assets Financed by: Shareholder's Funds Share Capital Retained Profit Long Term Liabilities Bank Loan Debentures Capital Employed These two These two figur es figures must must balance balance 14 1 5 12 3 20 15 80 40 30 150 5 155 80 50 20 5 155 What it’s What it’s doing with doing with its money its money Whereeits Wher its got it got it money money fr om from

- 29. Balance Sheet - Mr Reading's Burger Bar Ltd - 31st March 2005 The business has The business has bought some fixed boughtassets fixed assets some Fixed Assets Property 80 Machinery 40 Vehicles 30 150 Fixed Assets will last for Fixed Assets will last for MORE THAN ONE YEAR – MORE THAN ONE YEAR – they will have depreciated but they will have depreciated but we don’t need to worry about we don’t need to worry about this here….. this here…..

- 30. Current Assets last for a Current Assets last for a FEW MONTHS FEW MONTHS Current Assets Stock 5 Debtors 12 Cash 3 20 Liquidity Liquidity of assets of assets increases increases The most The most liquid – liquid – money the money the firm hasn’t firm hasn’t spent spent Raw Raw materials or materials or finished finished products it products it hasn’t sold hasn’t sold People who People who owe the owe the business business e.g. trade e.g. trade credit credit

- 31. Current Liabilities Creditors Unpaid Tax 14 1 15 The opposite The opposite to debtors – to debtors – the business the business owes them. owes them. This is money This is money owed to owed to suppliers They have They have to be paid to be paid within one within one year of year of the date the date of the of the Balance Balance Sheet Sheet

- 32. Fixed Assets Net Current Net Current Assets = Assets = Current Current Assets – Assets – Current Current 5 Liabilities 12 Liabilities 3 It’s also It’s also 20 called called working working capital – does capital – does 14 the business the business 1 15 have enough have enough capital to capital to 5 pay off its pay off its 155 short-term short-term Net Current Assets + Fixed Assets = Net debts? .. Net Current Assets + Fixed Assets = Net Assets Assets debts? This is the net worth of the business – everything This is the net worth of the business – everything its spent its cash on! its spent its cash on! Property Machinery Vehicles Current Assets Stock Debtors Cash Current Liabilities Creditors Unpaid Tax Net Current Assets (Working Cpaital) Net Assets - 80 40 30 150 +

- 33. Financed by: Shareholder's Funds Share Capital Retained Profit Long Term Liabilities Bank Loan Debentures Capital Employed 80 50 20 5 155 Capital Employed is what you get Capital Employed is what you get when you add shareholders funds when you add shareholders funds and long term liabilities. It must and long term liabilities. It must equal Net Assets! equal Net Assets! Money put into Money put into business from business from share issue share issue All the profit All the profit retained for retained for future future investment investment Money that is Money that is borrowed from borrowed from other people – other people – debts that debts that take over a take over a year to pay year to pay

- 35. For stakeholders it is very important to analyse the final published accounts of companies. They could tell us of the performance of the company and the financial strength of the company.

- 36. There are many ratios that can be calculated from a set of accounts. These ratios are used to compare performance and liquidity.

- 37. Gross Profit Margin %=Gross Profit X100 Sales Turnover This shows how much gross profit the company is making for every pound. An increase will mean that prices have increased or the cost of goods have been reduced.

- 38. N.P Margin= Net Profit X100 Sales Turnover This will be lower than the G.P margin because other expenses would have been deducted. The higher the result the better.

- 39. ROCE(%)= Net Profit X100 Capital Employed The higher the figure the more efficient the business is running. It means the business is making higher profits for each dollar invested in the business.

- 40. Liquidity Ratios calculate how quickly the business can pay back its short term debts. Current Ratio= Current Assets Current Liabilities

- 41. A safe current ratio should be between 1.5-2. Anything less than one means that the business will struggle to pay off its debt. This ratio is good but it forgets that not all current assets such as stock can be sold straight away.

- 42. Acid Test Ratio= Current Assets-Stock Current Liabilities Anything below 1 is a worry for the business as that means it currently can not pay off it’s debts. If it is too high it suggests the business has too much money not being used correctly.

- 43. Ratios are only good when you are comparing them to previous year or similar businesses together. It is important to remember that ratios: -Are based on past results -May be out of date (businesses change) -Different companies may value assets differently

- 44. In pairs can you go through the ratio case study of Frank Frankfurters Then Page You 105-124 need to work through this in your