Bba 203

•Télécharger en tant que DOCX, PDF•

0 j'aime•15 vues

Dear students get fully solved assignments Send your semester & Specialization name to our mail id : “ help.mbaassignments@gmail.com ” or Call us at : 08263069601

Recommandé

Contenu connexe

Tendances

Tendances (14)

Similaire à Bba 203

Similaire à Bba 203 (20)

Dernier

Dernier (20)

Bba 203

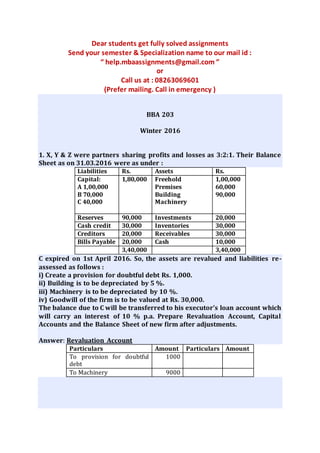

- 1. Dear students get fully solved assignments Send your semester & Specialization name to our mail id : “ help.mbaassignments@gmail.com ” or Call us at : 08263069601 (Prefer mailing. Call in emergency ) BBA 203 Winter 2016 1. X, Y & Z were partners sharing profits and losses as 3:2:1. Their Balance Sheet as on 31.03.2016 were as under : Liabilities Rs. Assets Rs. Capital: A 1,00,000 B 70,000 C 40,000 1,80,000 Freehold Premises Building Machinery 1,00,000 60,000 90,000 Reserves 90,000 Investments 20,000 Cash credit 30,000 Inventories 30,000 Creditors 20,000 Receivables 30,000 Bills Payable 20,000 Cash 10,000 3,40,000 3,40,000 C expired on 1st April 2016. So, the assets are revalued and liabilities re- assessed as follows : i) Create a provision for doubtful debt Rs. 1,000. ii) Building is to be depreciated by 5 %. iii) Machinery is to be depreciated by 10 %. iv) Goodwill of the firm is to be valued at Rs. 30,000. The balance due to C will be transferred to his executor’s loan account which will carry an interest of 10 % p.a. Prepare Revaluation Account, Capital Accounts and the Balance Sheet of new firm after adjustments. Answer: Revaluation Account Particulars Amount Particulars Amount To provision for doubtful debt 1000 To Machinery 9000

- 2. 2. Explain Bill of exchange and the procedure for recording bills in the books of drawer and accepter when the bill is : Accepted and discharged. i) Explain bill of exchange ii) Journal entries in the books of drawer iii) Journal entries in the books of acceptor Answer: A bill of exchange is documentary evidence in writing containing an unconditional order signed by the maker, directing a certain person to pay a certain sum of money only to, or the order of, a certain person or to the bearer of the instrument. In the Boo 3. What do you understand by goodwill? Explain the accounting treatment of goodwill at the time of admission. Give journal entry for the below problem: T and S are partners in a firm sharing profit in the ratio 5:3. They admitted G as a new partner for 1/4th share in the profit. G brings Rs.45,000 for her share ofgoodwill and Rs.1,20,000 forcapital. They have withdrawn the goodwill from the firm. Make journal entries in the books of the firm after the admission of G. The new profit sharing ratio will be 2:1:1. Meaning of goodwill with the formula Accounting treatment of goodwill at the time of admission Journal entry in the books of T,S and G (Unit 10) Answer: Goodwill generally means the reputation of the firm. When a business is doing its operations over a number of years, it may develop a good name and reputation among the customers or society. Inaccounting parlance, itcan be called as “Goodwill”. The goodwill of a firm may earn 4. Accounting refers to a systematic knowledge of accounting. It explains ‘why to do’ and ‘how to do’ of various aspects of accounting. Explain the objectives of accounting and explain the categories of users. Explanation of accounting objectives Explanation of categories of users (Unit 1) Answer: Accounting objectives Systematic recording of all business events or transactions and subsequent posting to ledger, to finally prepare financial statements - profit and loss account and balance sheet. Reporting the results to management, shareholders, creditors, bankers, investors, stock brokers, stock exchanges, employees, government etc.

- 3. Satisfying the statutory requirements, especially Registrar of Companies (ROC), Securities 5. Prepare Trading, Profit and Loss Account and Balance Sheet from the following particulars as on 31st March 2016. Trial Balance Particulars Dr. (Rs) Cr. (Rs) Capital / Drawings 1400 10000 Cash in hand 1500 - Bank overdraft @ 5% - 2000 Purchase and Sales 12000 15000 Returns 1000 2000 Establishments charges 2500 - Taxes and Insurance 500 - Provision for Doubtful Debts - 1000 Bad Debts 500 - Sundry Debtors and Creditors 5000 1850 Commission - 500 Investments 4000 - Stock on 1 April 2010 3000 - Furniture 600 - Bills Receivable & Bills payable 3000 2500 Collected Sales Tax - 150 Total 35000 35000 Further, you are required to take into consideration the following information: a) Salary Rs.100 and taxes Rs.400 are outstanding but insurance Rs.50 prepaid b) Commission amounting to Rs.100 has been received in advance for work to be done next year. c) Interest accrued on investments Rs.210 d) Provision for doubtful Debts is to be maintained at 20% e) Depreciation on furniture is to be charged at 10% p.a. f) Stock on 31st March 2016 was valued at Rs.4,500 g) A fire occurred on 25th March 2016 in the godown and stock of the value of Rs.1,000 was destroyed. It was fully insured and the insurance company admitted the claim in full. [Calculation of Trading and P/L a/c-5 Preparation of balance sheet-5] Answer: Trading and Profit and loss Account for the period ended 31st March 2016

- 4. Particulars Rs Rs Particulars Rs Rs To Opening Stock 3000 By Sales 15000 To Purchase 12000 Less: Sales Returns 1000 14000 6 From the ledger balances as on 31st March 2016 show treatments in Profit and Loss Account and in Balance Sheet. Debtors: 50,000; Bad Debts: 3,000; Discount Allowed : 2,000; Creditors: 30,000; Provision for Discount on Creditors : 400; Discount Received 300. Adjustments: i) Create a provision for Bad Debts @ 10 % on Debtors ii) Create a provision for Discount on Debtors @ 5 % iii) Additional discount given to Debtors Rs. 1,000 iv) Create a provision for discount on Creditors @ 2 %. From the ledger balances and adjustments as above, show treatments in : Profit and Loss Account and Balance Sheet. Answer: Profit and loss account for the year ended 31st March, 2016 Particulars Amount (Rs) Particulars Amount (Rs) Dear students get fully solved assignments Send your semester & Specialization name to our mail id : “ help.mbaassignments@gmail.com ” or Call us at : 08263069601 (Prefer mailing. Call in emergency )