Major healthcare delivery trends 2015

•

1 j'aime•985 vues

The document discusses several secular trends in healthcare, including the shift towards value-based reimbursement models, increasing consumerism, and rapid advancements in technology and use of big data. Major trends include growing consolidation across healthcare sectors, 50% of Medicare payments transitioning to value-based models by 2018, a large increase in high deductible health plans, and billions in investments in digital health, technology, and analytics.

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (20)

Similaire à Major healthcare delivery trends 2015

Similaire à Major healthcare delivery trends 2015 (20)

Plus de Usama Malik

Dernier

Dernier (20)

Major healthcare delivery trends 2015

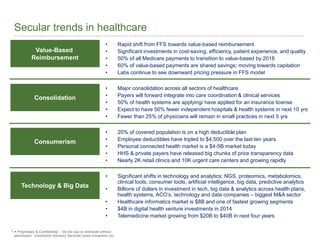

- 1. 1 Proprietary & Confidential – Do not use or distribute without permission - InnoAction Advisory Services (www.innoaction.co) Secular trends in healthcare Consolidation Consumerism Value-Based Reimbursement Technology & Big Data • Rapid shift from FFS towards value-based reimbursement • Significant investments in cost-saving, efficiency, patient experience, and quality • 50% of all Medicare payments to transition to value-based by 2018 • 60% of value-based payments are shared savings; moving towards capitation • Labs continue to see downward pricing pressure in FFS model • Major consolidation across all sectors of healthcare • Payers will forward integrate into care coordination & clinical services • 50% of health systems are applying/ have applied for an insurance license • Expect to have 50% fewer independent hospitals & health systems in next 10 yrs • Fewer than 25% of physicians will remain in small practices in next 5 yrs • 20% of covered population is on a high deductible plan • Employee deductibles have tripled to $4,500 over the last ten years • Personal connected health market is a $4-5B market today • HHS & private payers have released big chunks of price transparency data • Nearly 2K retail clinics and 10K urgent care centers and growing rapidly • Significant shifts in technology and analytics: NGS, proteomics, metabolomics, clinical tools, consumer tools, artificial intelligence, big data, predictive analytics • Billions of dollars in investment in tech, big data & analytics across health plans, health systems, ACO’s, technology and data companies – biggest M&A sector • Healthcare informatics market is $8B and one of fastest growing segments • $4B in digital health venture investments in 2014 • Telemedicine market growing from $20B to $40B in next four years

- 2. 2 Proprietary & Confidential – Do not use or distribute without permission - InnoAction Advisory Services (www.innoaction.co) Payer $700B** market growing at 3-4% Top 5 payers control >50% of market Rapid growth in lives from 50M uninsured Some form of VBR* for 135M lives and growing Rapidly moving toward “defined contribution” Notable technology/ analytics/ data investments Increased investments in public & private ACO’s Creating “narrow” & “ultra-narrow” networks More scrutiny around new drugs/ devices/ tests Source: Levin Associates, McKinsey (*): VBR = Value Based Health (**): Gross revenue – 85% is pass-through medical costs

- 3. 3 Proprietary & Confidential – Do not use or distribute without permission - InnoAction Advisory Services (www.innoaction.co) Hospitals $1T market growing to $1.6T by 2022 Outpatient accounted for 43% vs. 24% in ‘91 $200B of reimbursement cuts to fund expansion Value & quality focus shifting business models Hosp. acquired conditions & readmits penalized Significant horizontal & vertical integration Stronger cost controls & more centralization Viability hinges on 15-30% cost cutting ahead >50% own health plans or expected to by ‘18 Source: Levin Associates, Leerink

- 4. 4 Proprietary & Confidential – Do not use or distribute without permission - InnoAction Advisory Services (www.innoaction.co) ACO 750 ACO’s w/ 25M lives since 2011 75-100M lives covered by end of decade Reimbursed via shared savings & capitation 50% of ACO’s view labs as crucial value drivers Pop. health is key focus but limited capabilities $411M in net savings in ’14 by Medicare ACO’s Savings/ ACO doubled to $6M/ ACO since ‘11 Major consolidation expected ahead Cost cutting will remain a priority Source: Levin Associates, Goldman Sachs

- 5. 5 Proprietary & Confidential – Do not use or distribute without permission - InnoAction Advisory Services (www.innoaction.co) Types of Medicare ACO’s Medicare Shared Savings Program ACO’s • If the ACOs reach certain quality measures, they share in a portion of Medicare’s savings (enrollment now closed) Pioneer ACO’s • For organizations who already have experience coordinating patient care across several types of providers Advance Payment ACO’s • Organizations that would like to create an ACO but do not have the capital can receive upfront financial support in the form of an advance on their shared savings Source: G2 Intelligence

- 6. 6 Proprietary & Confidential – Do not use or distribute without permission - InnoAction Advisory Services (www.innoaction.co) Consumer Seniors drive >75% of costs (60M > 65 by ’20) Top 1% -> 22% of costs; top 5% -> 50% of costs Chronic disease -> 85% of costs; 7/10 deaths 20% of covered folks on high deductible plans OOP expense >$300B; Wellness industry >$6B Telemedicine $20B; Personal wellness tech $5B 95% of consumers search for health online 12M getting home health; 7.5M in mobile clinics >2K retail clinics & >10K urgent care centers Source: PWC, Deloitte

- 7. 7 Proprietary & Confidential – Do not use or distribute without permission - InnoAction Advisory Services (www.innoaction.co) Technology US HIT is $22B; health data/ analytics is $8B 25-30% of $3T spend can be avoided with tech Telehealth to grow from $20B to $40B by ‘20 Global mHealth at $23B by 2017 (Monitoring $15B; Dx $3.4B; Treatment $2.3B; DocSupport $1.1B) $4B in digital health venture investments in ’14 Global precision medicine at $40B (biomarkers, genomics, proteomics, metabolomics, CDx, big data) Global POC market -> $17B in ‘15 to $20B by ‘18 Wearable tech at $10B by ‘20 Pop. health & quality improvement top priorities Source: G2 Intelligence, Rock Health