BANK OF AMERICA MERRILL LYNCH MONGOLIAN MINING CORPORATION SENIOR NOTE USD 60...

OTMT Trading Idea

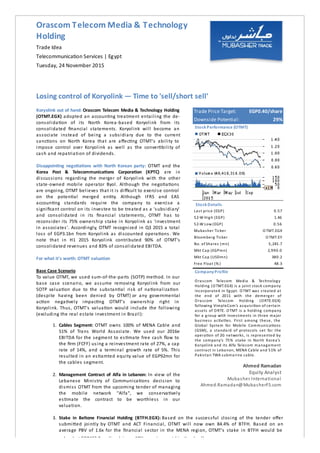

1. Trade Price Target: EGP0.40/share

Downside Potential: 29%

Stock Performance (OTMT)

Stock Details

Last price (EGP) 0.57

52-W High (EGP) 1.46

52-W Low (EGP) 0.56

Mubasher Ticker OTMT.EGX

Bloomberg Ticker OTMT:EY

No. of Shares (mn) 5,245.7

Mkt Cap (EGPmn) 2,990.0

Mkt Cap (USDmn) 380.2

Free Float (% ) 48.3

Company Profile

Orascom Telecom Media & Technology

Holding (OTMT.EGX) is a joint stock company

incorporated in Egypt. OTMT was created at

the end of 2011 with the demerger of

Orascom Telecom Holding (ORTE.EGX)

following VimpleCom’s acquisi on of certain

assets of ORTE. OTMT is a holding company

for a group with investments in three major

business ac vi es. First among these, the

Global System for Mobile Communica ons

(GSM), a standard of protocols set for the

opera on of 2G networks, is represented by

the company’s 75% stake in North Korea’s

Koryolink and its Alfa Telecom management

contract in Lebanon, MENA Cable and 51% of

Pakistan TWA submarine cable.

Ahmed Ramadan

Equity Analyst

Mubasher International

Ahmed.Ramadan@MubasherFS.com

Koryolink out of hand: Orascom Telecom Media & Technology Holding

(OTMT.EGX) adopted an accoun ng treatment entailing the de-

consolida on of its North Korea-based Koryolink from its

consolidated financial statements. Koryolink will become an

associate instead of being a subsidiary due to the current

sanc ons on North Korea that are affec ng OTMT's ability to

impose control over Koryolink as well as the conver bility of

cash and repatriation of dividends.

Disappoin ng nego a ons with North Korean party: OTMT and the

Korea Post & Telecommunica ons Corpora on (KPTC) are in

discussions regarding the merger of Koryolink with the other

state-owned mobile operator Byol. Although the nego a ons

are ongoing, OTMT believes that it is difficult to exercise control

on the poten al merged en ty. Although IFRS and EAS

accoun ng standards require the company to exercise a

significant control on its investee to be treated as a 'subsidiary'

and consolidated in its financial statements, OTMT has to

reconsider its 75% ownership stake in Koryolink as 'investment

in associates'. Accordingly, OTMT recognized in Q3 2015 a total

loss of EGP3.1bn from Koryolink as discounted opera ons. We

note that in H1 2015 Koryolink contributed 90% of OTMT's

consolidated revenues and 83% of consolidated EBITDA.

For what it's worth: OTMT valuation

Base Case Scenario

To value OTMT, we used sum-of-the-parts (SOTP) method. In our

base case scenario, we assume removing Koryolink from our

SOTP valua on due to the substan al risk of na onaliza on

(despite having been denied by OTMT) or any governmental

ac on nega vely impac ng OTMT's ownership right in

Koryolink. Thus, OTMT's valua on would include the following

(excluding the real estate investment in Brazil):

1. Cables Segment: OTMT owns 100% of MENA Cable and

51% of Trans World Associate. We used our 2016e

EBITDA for the segment to es mate free cash flow to

the firm (FCFF) using a reinvestment rate of 27%, a cap

rate of 14%, and a terminal growth rate of 5%. This

resulted in an es amted equity value of EGP92mn for

the cables segment.

2. Management Contract of Alfa in Lebanon: In view of the

Lebanese Ministry of Communica ons decision to

dismiss OTMT from the upcoming tender of managing

the mobile network "Alfa", we conserva vely

es mate the contract to be worthless in our

valuation.

3. Stake in Beltone Financial Holding (BTFH.EGX): Based on the successful closing of the tender offer

submi ed jointly by OTMT and ACT Financial, OTMT will now own 84.4% of BTFH. Based on an

average PBV of 1.6x for the financial sector in the MENA region, OTMT's stake in BTFH would be

valued at EGP463.2mn (implying a 19% premium paid in the deal).

Orascom Telecom Media & Technology

Holding

Trade Idea

Telecommunication Services | Egypt

Tuesday, 24 November 2015

Losing control of Koryolink — Time to 'sell/short sell'

2. valued at EGP463.2mn (implying a 19% premium paid in the deal).

4. Adjusted Net Cash/(Debt): We factored the adjusted net cash/ (debt) balance of EGP1.26bn a er

considering the expected cash outflow needed for BTFH deal of EGP549.4mn.

Based on our SOTP valua on in this scenario, we valued OTMT at EGP0.35/share, implying a downside

potential of 39%.

Best Case Scenario

In this scenario, we think the best case for OTMT would be to value its investment in Koryolink at its fair value

calculated by an independent financial advisor (IFA), which is EGP614mn. Using the same above valua on

assump ons for the other segments, we valued OTMT at EGP0.46/share, implying a downside poten al of

19%.

Sell OTMT now pending visibility on its future — Se ng a weighted average PT of EGP0.40/share (a 29% downside

poten al): Applying equal weights to both 'base' and 'best' scenarios, we reached a weighted value of

EGP0.40/share, implying a downside poten al of 29%. Thus, we believe it would be best to either sell OTMT's

local shares with a trading price target (PT) of EGP0.40/share (or short sell its GDRs with a trading PT of

USD0.26/GDR).

4. redistributed, reproduced, stored in a retrieval system, or transmi ed, on any form or by any means, electronic, mechanical,

photocopying, recording, or otherwise, without the prior wri en permission of MFS. MubasherTrade is a trademark of

Mubasher Financial Services BSC. Mubasher Financial Services BSC (c) is an Investment Business Firm Category 1, licensed and

regulated by the Central Bank of Bahrain.