Recommandé

Contenu connexe

En vedette

En vedette (15)

Dernier

Dernier (20)

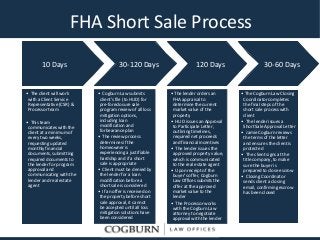

FHA Short Sale Process flowchart

- 1. FHA Short Sale Process • The client will work with a Client Service Representative (CSR) & Processor team • This team communicates with the client at a minimum of every two weeks, requesting updated monthly financial documents, submitting required documents to the lender for program approval and communicating with the lender and real estate agent • The Cogburn Law Closing Coordinator completes the final steps of the short sale process with client • The lender issues a Short Sale Approval Letter • Jamie Cogburn reviews the terms of the letter and ensures the client is protected • The client signs at the title company, to make sure the buyer is prepared to close escrow • Closing Coordinator sends client a closing email, confirming escrow has been closed 30-120 Days10 Days 120 Days 30-60 Days • Cogburn Law submits client’s file (to HUD) for pre-foreclosure sale program review of all loss mitigation options, including loan modification and forbearance plan • The review process determines if the homeowner is experiencing a justifiable hardship and if a short sale is appropriate • Client must be denied by the lender for a loan modification before a short sale is considered • If an offer is received on the property before short sale approval, it cannot be accepted until all loss mitigation solutions have been considered • The lender orders an FHA appraisal to determine the current market value of the property • HUD issues an Approval to Participate Letter, outlining timelines, required net proceeds and financial incentives • The lender issues the approved property value, which is communicated to the real estate agent • Upon receipt of the buyer’s offer, Cogburn Law Offices submits the offer at the approved market value to the lender • The Processor works with the Cogburn Law attorney to negotiate approval with the lender