Journal of Comparative Economics 38 (2010) 34–51

Contents lists available at ScienceDirect

Journal of Comparative Economics

j o u r n a l h o m e p a g e : w w w . e l s e v i e r . c o m / l o c a t e / j c e

Infrastructure development in China: The cases of electricity, highways,

and railways

Chong-En Bai a,b,*, Yingyi Qian a,c

a School of Economics and Management, Tsinghua University, Beijing 100084, China

b National Institute for Fiscal Studies, Tsinghua University, Beijing 100084, China

c University of California, Berkeley

a r t i c l e i n f o

Article history:

Received 21 October 2009

Available online 27 October 2009

JEL classification:

H44

L9

O14

R42

R48

Key words:

Infrastructure

Electricity

Highway

Railway

China

0147-5967/$ - see front matter � 2010 Published b

doi:10.1016/j.jce.2009.10.003

* Corresponding author. Address: School of Econo

E-mail addresses: [email protected] (

1 One commonly used approach is to estimate th

infrastructure (for example, Aschauer, 1989; Munnel

(for example, Hulten and Schwab, 1991; Tatom, 1991

Morrison and Schwartz (1996) and Lynde and Richmo

Li (2005) adopts a third approach and uses the chang

return to infrastructure investment. He finds significa

and Fan and Zhang (2004) and they both find positi

infrastructure increases property value (Haughwout, 2

Ying, 1988).

a b s t r a c t

Bai, Chong-En, and Qian, Yingyi—Infrastructure development in China: The cases of elec-

tricity, highways, and railways

This paper considers the development of the electricity, highway, and railway sectors in

China, with special emphasis on investment incentives. Statistical summary of the devel-

opment of these sectors is offered, followed by a detailed description of the institutional

background, including investment and pricing mechanisms. We also analyze investment

incentives based on the institutional background and present our estimates of the rates

of return to investment in these sectors. It is observed that some of the current practices

may serve as useful transitional arrangements even though they are not desirable in the

long run. Journal of Comparative Economics 38 (1) (2010) 34–51. School of Economics and

Management, Tsinghua University, Beijing 100084, China; National Institute for Fiscal

Studies, Tsinghua University, Beijing 100084, China; University of California, Berkeley.

� 2010 Published by Elsevier Inc. on behalf of Association for Comparative Economic

Studies.

1. Introduction

There is a large literature studying the importance of infrastructure to economic development.1 However, there is not

much systematic research on how infrastructure is developed. Many issues are worth consideration. One of these issues is

investment incentives. Infrastructure may yield significant social returns. However, this does not guarantee that investors of

infrastructure projects can get sufficient private return. How can one provide incentives for private investment? If there is

not sufficient private incentive to i ...

Journal of Comparative Economics 38 (2010) 34–51Contents lis.docx

1. Journal of Comparative Economics 38 (2010) 34–51

Contents lists available at ScienceDirect

Journal of Comparative Economics

j o u r n a l h o m e p a g e : w w w . e l s e v i e r . c o m / l o c

a t e / j c e

Infrastructure development in China: The cases of electricity,

highways,

and railways

Chong-En Bai a,b,*, Yingyi Qian a,c

a School of Economics and Management, Tsinghua University,

Beijing 100084, China

b National Institute for Fiscal Studies, Tsinghua University,

Beijing 100084, China

c University of California, Berkeley

a r t i c l e i n f o

Article history:

Received 21 October 2009

Available online 27 October 2009

JEL classification:

H44

L9

O14

R42

R48

Key words:

2. Infrastructure

Electricity

Highway

Railway

China

0147-5967/$ - see front matter � 2010 Published b

doi:10.1016/j.jce.2009.10.003

* Corresponding author. Address: School of Econo

E-mail addresses: [email protected] (

1 One commonly used approach is to estimate th

infrastructure (for example, Aschauer, 1989; Munnel

(for example, Hulten and Schwab, 1991; Tatom, 1991

Morrison and Schwartz (1996) and Lynde and Richmo

Li (2005) adopts a third approach and uses the chang

return to infrastructure investment. He finds significa

and Fan and Zhang (2004) and they both find positi

infrastructure increases property value (Haughwout, 2

Ying, 1988).

a b s t r a c t

Bai, Chong-En, and Qian, Yingyi—Infrastructure development

in China: The cases of elec-

tricity, highways, and railways

This paper considers the development of the electricity,

highway, and railway sectors in

China, with special emphasis on investment incentives.

Statistical summary of the devel-

opment of these sectors is offered, followed by a detailed

description of the institutional

background, including investment and pricing mechanisms. We

also analyze investment

incentives based on the institutional background and present our

estimates of the rates

3. of return to investment in these sectors. It is observed that some

of the current practices

may serve as useful transitional arrangements even though they

are not desirable in the

long run. Journal of Comparative Economics 38 (1) (2010) 34–

51. School of Economics and

Management, Tsinghua University, Beijing 100084, China;

National Institute for Fiscal

Studies, Tsinghua University, Beijing 100084, China;

University of California, Berkeley.

� 2010 Published by Elsevier Inc. on behalf of Association for

Comparative Economic

Studies.

1. Introduction

There is a large literature studying the importance of

infrastructure to economic development.1 However, there is not

much systematic research on how infrastructure is developed.

Many issues are worth consideration. One of these issues is

investment incentives. Infrastructure may yield significant

social returns. However, this does not guarantee that investors

of

infrastructure projects can get sufficient private return. How can

one provide incentives for private investment? If there is

not sufficient private incentive to invest in infrastructure, are

there enough incentives for politicians and bureaucrats to over-

come many difficulties to make public investment in

infrastructure? To address these issues, one has to understand

the insti-

y Elsevier Inc. on behalf of Association for Comparative

Economic Studies.

mics and Management, Tsinghua University, Beijing 100084,

China. Fax: +86 10 62785562.

C.-E. Bai), [email protected] (Y. Qian).

4. e production function with infrastructure as an input. Some find

significant returns to investment in

l, 1990; Rubin, 1991; Holtz-Eakin, 1994), while others do not

find significant returns to such investment

; Munnell, 1992; Kavanagh, 1997). Another approach is to

estimate the cost function. Using this approach,

nd (1992) both find evidence supporting a significant role of

public infrastructure in productivity growth.

es in interregional price gaps before and after the construction

of a railway in China to estimate the social

nt return to the investment. Other studies on the role of

infrastructure in China include Demurger (2001)

ve relationship between infrastructure and economic growth.

There are also findings that suggest that

002), reduces inventory costs (Shirley and Winston, 2004), and

cuts the cost of trucking firms (Keeler and

http://dx.doi.org/10.1016/j.jce.2009.10.003

mailto:[email protected]

mailto:[email protected]

http://www.sciencedirect.com/science/journal/01475967

http://www.elsevier.com/locate/jce

C.-E. Bai, Y. Qian / Journal of Comparative Economics 38

(2010) 34–51 35

tutions surrounding infrastructure. Who is allowed to invest in

infrastructure? What are the restrictions faced by the investors?

In the case infrastructure is built with private investment, how

is the price for the use of infrastructure is regulated? In the case

of public investment, what is the environment faced by the

politicians and bureaucrats? Without a clear understanding of

these

institutions, it is impossible to understand the development of

infrastructure.

5. Before we can get the full picture, it is useful to start with a few

cases. This paper attempts to contribute to this first step

by investigating the development of the electricity, highway,

and railway sectors in China. We will not consider urban infra-

structure because relevant information is more difficult to find

and there are also too many aspects of urban infrastructure

for us to cover in this paper. We will not consider the

communication sector because its development seems less

problematic

than other sectors of infrastructures and certain success has

been achieved in the sector in many developing countries.

Among the modes of transportation, we will not consider

waterways, ports, civil aviation, or pipelines. Instead, we focus

on the sectors of electricity, highways and railways because

they exhibit unique Chinese characteristics and they also offer

interesting contrast among them.

For each sector we consider, we first offer a statistical summary

of its development in China. We present the capacity and

the output of the sector. We not only offer a snapshot of the

current situation, we also provide relevant historical statistics.

The paper also provides a detailed institutional background for

the development of each sector. We particularly empha-

size institutions related to investment incentives. These include

investment policies and the pricing of the services. Again,

the history of the institutions is presented, and the current

situation is described in greater details.

Based on the institutional background, we analyze investment

incentives and existing problems in each sector. Some

practices are part of the solution to providing investment

incentives and at the same time sources of economic costs in

terms

of distortion of investment decision and high prices paid by

6. consumers, and social and political costs in terms of corruption

and income inequality. We discuss both the benefits and costs

of these practices.

Finally, we present of estimates of the rates of return to

investment for each sector. These estimates provide quantitative

indication about incentives for investment outside of

government budget.

This paper does not consider a few aspects related to investment

in these sectors. One is the cost of acquiring the land

needed for the development. Another is the cost of complying

with environmental regulations and other regulations. We

focus more on the benefits of investment to the investors rather

than the costs. The cost issues await future research.

2. The electricity sector

2.1. Statistical summary

The development of the electricity sector has basically kept in

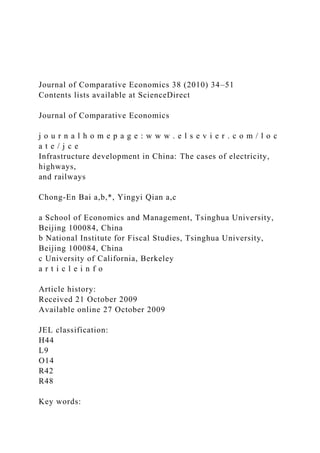

pace with the growth of real GDP (Fig. 1 and Table 1). From

1978 to 2007, the annual growth rates of installed capacity and

the amount of electricity generated were 9.1% and 9.2%

respectively. In the same period, the annual growth rate of real

GDP was 9.8%. In 2007, the total amount of electricity gen-

erated was 3256 billion kW-h, representing a 14.44% increase

over the previous year. Around 83% of the output was from

thermal power, 15% hydro power, and 2% nuclear power. The

total installed capacity was 713.3 GW.

On the demand side, household consumption accounts for 11%

of the total. Industry consumes 76.6% of the total, services

9.8%, and agriculture 2.6%, with industrial consumption,

especially that by the heavy industry, growing the fastest.

7. Given the price structure, the demand and supply of electricity

is basically in balance. According to the annual report of

the 2007 State Electricity Regulatory Commission, the

maximum shortfall of capacity during peak load in 2007 was

only

10 GW, a mere 1.4% of total installed capacity.

(Logarithm with 1978 Values Nornalized to Zero)

0

0.5

1

1.5

2

2.5

3

19

78

19

80

19

82

19

84

19

86

11. The first is the pre-reform period before 1978. At that time, the

degree of government control was even higher in the elec-

tricity sector than in most of the other sectors. The sector was

characterized by two features. One is that there was no sep-

aration of government functions, such as formulating and

enforcing regulations on entry, pricing, and system security,

from

business activities, such as electricity generation, transmission,

and distribution. Both functions were played by one govern-

ment agency, the Ministry of Electricity Industry and local

bureaus under the ministry, although the name of the agency

changed several times. The second is that all activities were

under rigid state plan.

Starting from a very low base, the electricity sector experienced

a period of rapid growth. At the end of 1949, the

total installed capacity in the whole country was only 1850

MW, generating 4.3 billion kW-h of electricity annually, with

annual per capita output of less than 8 kW-h. By the end of

1978, the total installed capacity had increased to

57,120 MW, with annual total output of 256.6 billion kW-h and

per capita output of 266 kW-h. The annual growth rates

of total installed capacity and electricity generation were 12.6%

and 15.1% respectively. Despite of the high growth rates,

electricity shortage was always a severe problem. Misallocation

as a result of rigid planning was partly responsible for

the shortage.

The second period is between 1978 and 2002. In this period,

state plan was loosened and government functions and

business activities began to be separated in this sector.

However, competition was limited and the bureaus of electricity

industry and later the electric power corporations played an

overwhelmingly dominant role in the sector. There were

three milestones in the reform process. The first was a 1985

12. electricity policy document approved by the state council

(SCC, 1985). This document allowed investment in electricity

generation from outside of the state budget, including

C.-E. Bai, Y. Qian / Journal of Comparative Economics 38

(2010) 34–51 37

foreign investment. At the same time, it also allowed the

electricity generated by plants built with non-state-budgetary

funds to enter the market. As a result, two tracks with different

prices emerged in the electricity sector, one within the

state plan and the other outside. The second milestone was the

1987 state council policy of separating government func-

tions from business activities in the electricity sector. In each

province, an electric power corporation was set up parallel

to the government bureau of electricity industry. The 1985

policy of encouraging diverse sources of investment in the

electricity sector was reaffirmed. Because the provincial

enterprises were rather independent of one another, the market

was segmented. The third milestone was establishment of the

National Electric Power Corporation in 1997 and the sub-

sequent abolishment of the Ministry of Electricity Industry in

1998. After the abolishment of the Ministry of Electricity

Industry, the government functions in this sector became part of

the portfolio of the ministerial level State Economic

and Trade Commission.

The growth rates of the sector varied during this long period. In

the period of 1979–1984, the annual growth rates of total

installed capacity and electricity generation were 4.9% and

6.0% respectively. In the period of 1984–1997, however, the

cor-

responding rates were 9.2 and 8.8 respectively. In 1997, the

sector experienced surplus of supply, and the government then

decided not to approve any new investment in electricity

13. generation for the next 3 years. This turned out to be short

sighted.

By 2003, 22 provinces experienced severe shortage of

electricity supply and electricity had to be rationed again.

The third period started from 2002. The state council issued the

System Reform Plan for the Electricity Sector in February,

2002 (SCC, 2002), which shapes the current practices.

2.3. Current practices

2.3.1. Disaggregation

The 2002 plan consists of three main components. The first is to

separate electricity generation from its transmission and

distribution as well as other businesses. The National Electric

Power Corporation was broken up into two transmission and

distribution companies separated along regional lines, five

electricity generation companies, and four other companies

offer-

ing engineering and construction services for the electricity

sector.

With the implementation of the plan, the number of players has

increased significant, but the state still maintains a dom-

inant position in the market. At the end of 2007, there are more

than 4000 plants with installed capacity above 6 MW in the

electricity generation sector. Central government controlled

enterprises, including the five companies that spun off from Na-

tional Electric Power Corporation 5 years ago, had a 53.95%

share of the installed capacity, up 4.43% age points from the

year

earlier. Local government controlled enterprises had a share of

41%, down 4 percentage points, and private and foreign in-

vested enterprises had a share of 6.05%, down 0.16 percentage

points.

14. The transmission and distribution sector is mainly divided

between State Grid Corporation of China and China Southern

Power Grid, the two companies that spun off from the National

Electric Power Corporation in 2002 (SERC, 2008). Each power

grid company is a monopoly transmitter, distributor, and retailer

of electricity in its region. Generators sell power to the

power grid company, and their access to the grid is mostly at

the mercy of the latter, even though in some cases access is

supposed to be determined by a bidding process.

2.3.2. Pricing policy

The second component of the plan is to develop a new

mechanism for price formation. The idea is to let the market

play a

more important role in price formation in the sector in the long

run.

The price that consumers pay consists of four parts (NDRC,

2005a, 2005b, 2005c). One is the cost for the distributor to

acquire electricity from the generating plant, the second is the

losses in transmission and distribution, the third is the price

for transmission and distribution, and the fourth is government

surcharge. The price for transmission and distribution is

determined by the government based on the cost of transmission

and distribution. The cost for the distributor to acquire

electricity includes the price paid to the generating plant and

taxes paid to the government. The price paid to the generating

plants is a two-part tariff. One part is the capacity price

determined by the government that is independent of the actual

amount of electricity that is purchased, and the second part is a

unit price that is either determined by a bidding process

or by the government based on industry average cost, depending

on whether the region has set up a functioning electricity

trading system.

Different consumers pay different prices. Households pay the

15. lowest price, followed by agricultural users. Non-agricul-

tural business users pay the highest price.

2.3.3. Regulation authorities

The third component of the plan is to reform government

functions in the sector. The State Electricity Regulatory Com-

mission (SERC) was formed to regulate the industry but the

power to determine the prices in the sector rests with the Na-

tional Development and Reform Commission (NDRC). SERC’s

main charges are to maintain competition, protect the interests

of various stakeholders, enforce price regulation set out by

NDRC, and guarantee the security of the electricity system

(SERC,

2008). National Development and Reform Commission and its

local bureaus are responsible for determining the prices when

they are not determined by the market.

Table 2

Investment in fixed assets in urban area by jurisdiction of

management and registration status: production and supply of

electric power and heat power (unit:

billion yuan).

Year Total By jurisdiction By registration status By registration

status

Central Local Domestic HK, Macao, Taiwan Foreign State

Collective Private

2004 485.4 169.9 315.5 446.3 23.8 15.4 392.4 6.3 8.7

2005 650.3 219.4 430.9 601.6 31.3 17.4 507.7 6 12

2006 727.4 266.2 461.2 682.2 27.4 17.8 571.7 42.4 80.3

Sources: China Statistical Yearbook 2005–2007 (NBS, various

16. years).

38 C.-E. Bai, Y. Qian / Journal of Comparative Economics 38

(2010) 34–51

2.4. Investment incentives

2.4.1. Sources of investment

Substantial amount of resources are invested in the electricity

sector each year. In 2007, 304.2 billion yuan was invested

in electricity generation and 245.1 billion yuan in transmission.

Investment in the sector is dominated by state-controlled

enterprises. This can be seen from the distribution of installed

capacity among various types of enterprises that we discussed

earlier. Table 2 also illustrates this point, among others. The

National Bureau of Statistics does not provide investment data

for the electricity sector alone, but it provides investment data

for electricity together with heat power, which should be

indicative of the electricity sector. From the table, we can see

that most of the investment was made by state-controlled

enterprises; most of the funds came from domestic sources;

local governments invested more than the central government.

As Table 3 shows, of the total invested amount, domestic loan is

the most important component. Self-raised funds follow

closely behind. Self-raised funds include extra-budgetary funds

from central government ministries and local governments,

as well as the self-raised funds of enterprises and institutions.

State budget is not an important component of the total

investment in the electricity sector. Note that Tables 2 and 3

show different amount of total investment. This is because

the two sets of statistics come from different sources and the

differences between them are statistical discrepancies.

2.4.2. Incentives and problems

A natural question to ask is: why are there incentives for

17. investment in the electricity sector given the dominant role

played by state-controlled enterprises.

In the pre-reform era, state plan was very rigid and large

amount of resources could be mobilized to develop a few

priority

areas of the economy, possibly at the expense of other parts of

the economy. Electricity was among the few priority areas.

The electricity sector grew very rapidly then, more so than the

whole economy did.

After economic reform started, state plan became less rigid and

priority was rebalanced. Without given sufficient eco-

nomic incentives, the electricity sector would not grow as fast

as they once did. This could explain why growth slowed down

in the first few years of economic reform.

Since 1985, economic incentives have been gradually

introduced. First, investment from outside of the state budget

was

encouraged and the producers were given more autonomy over

electricity generation from the new investment. Then, gov-

ernment functions and business activities were separated in the

sector, first at the provincial level in 1987 and later at the

national level in 1997. With this separation, electricity is no

longer considered a government service, albeit with a fee, but a

commodity produced and provided by enterprises. This could be

one explanation behind a sharp difference between China

and India in the electricity sector that electricity stealing is not

a significant problem in China and losses in transmission only

accounts for about 7% of total output and are mostly due to

technical factors. Enterprises that supply electricity in China

are

subject to less political pressure than they used to be and have

strong incentives to enforce payment by consumers.

18. At the same time, the price formation mechanism has gradually

become more market oriented, with the prices mostly

reflecting industry average costs and normal rates of return.

There are times when the price of electricity is not be allowed

to adjust accordingly even though the price of coal used to

generate electricity has increased substantially, but this mostly

happens during most difficult economic times.

Increased competition is another factor that drives investment.

With the 2002 break up of the National Electric Power

Corporation, and the establishment of other electricity

generating enterprises, competition among them intensified

even

though they are mostly controlled by the state. Among the big

firms, the competition is mainly about who will become

Table 3

Source of funds of investment in urban area by sector:

production and supply of electric power and heat power (unit =

billion yuan).

Year Total By sources of funds

State budget Domestic loans Foreign investment Self-raised

funds Others

2004 499.8 19.2 222.2 18 206.7 33.6

2005 643.7 25.6 296.7 13.6 269.7 38.1

2006 729 31.4 338.7 8.1 304.6 46.3

Sources: China Statistical Yearbook 2005–2007 (NBS, various

years).

C.-E. Bai, Y. Qian / Journal of Comparative Economics 38

19. (2010) 34–51 39

the industry leaders and maintain that position. Both of the two

power grid companies and seven of the largest electric

power generating companies are among the 150 largest state-

owned enterprises under the direct control of the State-owned

Asset Supervision and Administration Commission (SASAC) of

the State Council. All of these state-owned enterprises are un-

der strong pressure to be among the top three enterprises in

their respective sector or face the risk of being restructured.

Furthermore, electricity generating enterprises are currently

competing fiercely for most important strategic assets of the

sector, plant sites that have convenient access to coal and water,

the supply of which is limited. They are worried that if

the ideal plant sites are all taken by their competitors, they

would face great difficulty expanding their capacity in the

future.

For all the power generating firms, they have to compete to sell

to the monopsonistic buyers of electricity, the power grid

companies that are separated along regional lines. This is

especially true for smaller power generating firms. If they do

not

gain enough scale and achieve sufficiently low cost, it is hard

for them to survive in the long run. Such competitive pressure

also gives firms strong incentives to invest.

Local governments are also an important force behind

incentives for investment in the electricity sector. A large

electric-

ity generating company is at the same time a large tax payer.

Sometime, the tax revenue from a large electricity generating

company can be a very substantial part of the tax revenue of a

county government. There is strong competition among

county governments to have the electricity generating company

located within their county, even when the region in general

enjoys strong geographical advantages in attracting the

company. One of the instruments the county government can use

20. is

concession on the land price that the county government charges

the company. Such competition among the local govern-

ments lowers the cost of investment in the sector and

encourages investment.

Even though the electric power grid companies face little

competition, they still have strong incentives to make invest-

ment. In 2007, investment in power grids accounted for 45% of

total investment in the electricity sector (SERC, 2008). Similar

to electricity generation, the way prices for transmission and

distribution are determined is one reason for the strong invest-

ment incentives. The prices are determined based on the

allowable costs, the allowable rate of return, and the related

taxes

(NDRC, 2005a). Possible tunneling by the insiders of power

grid companies through transfer pricing may also be a contrib-

uting factor behind the strong investment drive. All the power

grid companies are state owned and the sector is dominated

by two power grid companies. However, the provincial branches

of the companies enjoy considerable autonomy and many

investment decisions are made at the provincial level. Many of

the provincial power grid companies have a sister company

that is often owned by their employees or managers. The state-

owned provincial power grid company does many businesses

with the collectively owned sister company, including the

procurement of equipment, electricity, and other related

services.

On paper, the state-owned power grid companies may not be

very profitable. However, their collectively owned sister com-

panies are often very profitable. Dividend payment from the

sister company can be a substantial part of the income of the

employees of the state-owned counterpart. Such a relationship

between the two companies can create powerful investment

incentives for the state-owned power grid company. After all,

investment by the power grid company creates demand for

21. equipment and services and is good for the business of the sister

company, and this in turn benefits the managers and

employees of the power grid company. A consequence of this

practice is that the income of some managers and employees

of the power grid companies is much higher than that of similar

people in non-monopoly sectors. This has becomes a source

of resentment against income inequality.

It is possible that these strong investment incentives may give

rise to overinvestment. Indeed, there was surplus of supply

in 1997 and there have been concerns about overinvestment in

the last few years. However, the economy is growing very

rapidly and any surplus supply will soon be met by increased

demand. The aftermath of the 1997 experience is a case in

point. After the government suspended investment in electricity

generation for 3 years, shortage of electricity follows a

few years later. Of course, the economy will eventually slow

down and by then, overinvestment will become more costly.

The current system seems to work in the current environment

but may not be the first best arrangement in the long run.

The lack of foreign investment in the electricity sector is

interesting given that foreign direct investment has played a

very

significant role in other parts of the economy. Possible reasons

are as follows. The transmission and distribution sector is off

limit to foreign investment. Even though the power generation

sector is open to foreign investment, foreign invested gen-

erators are disadvantaged because local relationship is very

important for a generator to gain access to the grid, and to

secure

stable and cheap supply of coal. Furthermore, the most

important reason for foreign direct investment in China is not to

bring in capital, but to facilitate the transfer of knowhow (Bai,

Lu, and Tao, 2009). Technology in electricity generation is easy

to transfer even without long term participation of foreign

22. investors, and therefore, the role of foreign investors is not as

important as in many other sectors.

2.4.3. Rate of return to investment

Using data from the 2007 annual reports of the top 10 publicly

listed electricity generating companies, ranked according

to their total asset values in 2007, we estimate the average rate

of return on equity of these companies from 2000 to 2007

(Fig. 2). The rates range from 10.45% in 2002 to 12.78% in

2001. These rates are higher than the normal rate of return the

government uses to determine the prices, which is 1 percentage

point above the annual interest rate paid by long term gov-

ernment bonds. The high rates of return on equity are achieved

through leverage. They compare favorably with the rate of

return to capital of the whole economy net of urban residential

housing estimated by Bai et al. (2006).

We also estimate the rate of return to capital in the whole

electricity and heat power sector. We estimate the capital stock

of the sector using the perpetual inventory approach and the

investment data from 1950 to now, and derive the capital in-

come data by adding operating profits and production taxes of

enterprises. The rate of return is estimated by the ratio of

10.00%

10.50%

11.00%

11.50%

12.00%

23. 12.50%

13.00%

2000 2001 2002 2003 2004 2005 2006 2007

Fig. 2. Average return on equity of the top 10 publicly listed

electricity generating companies. Sources: corporate annual

reports.

85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

05 06

Year

Rate of Return to Capital in the Electricity Sector

0.050

0.100

0.150

0.200

Fig. 3. Rate of return to capital (net of depreciation) in

electricity and heat water sector. Sources: authors’ calculation.

40 C.-E. Bai, Y. Qian / Journal of Comparative Economics 38

(2010) 34–51

capital income over capital stock at current price (see Appendix

A for detailed description of data and estimation method).

Fig. 3 shows that the rate of return has been fluctuating around

10% since the last 1990s. Again, these rates compare well

with those of the whole economy net of urban residential

housing estimated by Bai et al. (2006).

24. 3. Highways

3.1. Statistical summary of the transportation sector

The transportation sector has experienced very rapid growth

since 1978. In 1978, the total passenger-km was 174 billion,

but in 2006, it was 1919 billion, representing an annual growth

rate of 8.9%. Civil aviation grew fastest, from 2.8 billion pas-

senger-km to 237 billion passenger-km, or 17.2% a year.

Highways follow, from 52 billion to 1013 billion, or 11.2% a

year, and

then railway, from 109 billion to 662 billion, or 6.6% a year.

The passenger-km of waterways dropped from 101 billion to 74

billion, or �1.1% a year. Fig. 4 shows the growth in passenger-

km of various modes of transportation with the real GDP

growth as the reference.

Since different modes of passenger transportation have very

different growth rates, their relative shares in the sector in

terms of passenger-kilometer has changed significantly since

1978. Fig. 5 shows the shares in passenger-kilometers of var-

ious modes of transportation. It shows that highways have

replaced railways as the most important mode of passenger

transportation and the importance of civil aviation has increased

dramatically, from 1.6% to 12.3%.

Freight transportation has also experienced very rapid growth

since 1978. In 1978, the total ton-km was 983 billion, but

in 2006, it was 8895 billion, representing an annual growth rate

of 8.2%. Civil aviation grew fastest, from 97 million ton-km

to 9.4 billion ton-km, or 17.8% a year. Highways follow, from

27.4 billion to 975.4 billion, or 13.6% a year, then waterway,

from 378 billion to 5549 billion, or 10.1% a year. The ton-km of

railways and petroleum and gas pipelines grew at

(Logarithm with the 1978 Values Normalized to 0)

29. nt

Railways

Highways

Waterways

Civil Aviation

Fig. 5. Shares in passenger-kilometers of various modes of

transportation. Sources: China Statistical Yearbook (NBS,

various years).

(Logarithm with the 1978 Values Normalized to 0)

-1

0

1

2

3

4

5

19

78

19

80

31. 20

06

Year

GDP Indices

Railways

Highways

Waterways

Civil Aviation

Petroleum and Gas Pipelines

Fig. 6. Real GDP and freight ton-kilometers by various modes

of transportation. Sources: China Statistical Yearbook (NBS,

various years).

C.-E. Bai, Y. Qian / Journal of Comparative Economics 38

(2010) 34–51 41

approximately the same rate, 5.2% and 5% respectively, with

the former going from 535 billion to 2195 billion and the latter

going from 43 billion to 166 billion. Fig. 6 shows the growth in

ton-km of various modes of transportation with the real GDP

growth as the reference.

The relative shares of different modes of freight transportation

have also changed significantly since 1978. Fig. 7 shows

the shares in ton-km of various modes of freight transportation.

It shows that waterways have replaced railways as the most

important mode of freight transportation. The importance of

highways increased dramatically from 2.8% in 1978 to 14.4% in

1998, but gradually declined to 11% in 2006.

The rapid increase in the volume of transportation is only

possible with the improvement of the transportation infrastruc-

ture. From 1978 to 2004, the length of highways increased from

890.2 to 1870.7 thousand km. From 1978 to 2006, the

32. lengths of railways in operation, civil aviation routes, and

petroleum and gas pipelines increased from 51.7 to 77.1, from

148.9 to 2113.5, and from 8.3 to 48.2 thousand km respectively.

Fig. 8 shows the growth of the lengths of transportation

routes. The growth in the length of highways is higher than that

of railways.

Among highways, expressways have been growing the most

rapidly. Their length increased from 100 km in 1988 to 45.3

thousand km in 2006. From 1988 to 2004, the length of all

highways grew at an annual rate of 4%, but the length of

express-

ways grew at a staggering annual rate of 44%. Fig. 9 illustrates

this phenomenal growth.

For the railway, we have some data about its technical

efficiency. The data shows that technical efficiency has also im-

proved together with the increase in the length of railways. Fig.

10 illustrates the trend of some of the indicators of technical

efficiency. We can see that the running speed of passenger

trains and that of the freight trains have both increased, with the

former increasing faster. The abnormality of the 2001 data

about freight train speed is probably due to a statistical error.

The

density of passenger transportation and freight transportation

both show significant improvement. The handling time of

freight first increased from 1985 to 1999 and has then gradually

come down since 1999.

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

36. 19

94

19

96

19

98

20

00

20

02

20

04

20

06

Year

Railways in Operation

Highways

Civil Aviation Routes

Petroleum and Gas Pipelines

Fig. 8. Length of Transportation Routes. Note: The 2005 and

2006 data for highways use a different definition from that used

for earlier years and are

therefore left out. Sources: China Statistical Yearbook (various

years).

37. Length of Highways and Expressways (Logarithm with the 1978

Values Normalized to 0)

0

1

2

3

4

5

6

7

19

88

19

89

19

90

19

91

19

92

19

41. Density of Passenger Transportation

(10 000 person.km/km)

Running Speed of Freight Trains

(km/hr)

Density of Freight Transportation (10

000 tn.km/km)

Handling Time of Freight (hour)

Fig. 10. The technical efficiency of railways. Sources: China

Statistical Yearbook (various years).

42 C.-E. Bai, Y. Qian / Journal of Comparative Economics 38

(2010) 34–51

In summary, the transportation sector as a whole has grown

rapidly. The growth rates of passenger-kilometer and ton-

kilometer are not very far below the growth rate of GDP.

However, railway has lagged behind. Although its technical

effi-

ciency has been improving, its growth rates in terms of

passenger-kilometer and ton-kilometer are both much lower

than

that of GDP, and its length has also been growing much slower

than that of the other modes of transportation. As a result,

its shares in passenger and freight transportation have both

declined steadily. In the remainder of this paper, we will

discuss

the development of the highway and railway sectors

respectively.

C.-E. Bai, Y. Qian / Journal of Comparative Economics 38

42. (2010) 34–51 43

3.2. Evolution of highway policy

The evolution of highway policy can be divided into four

stages, with more market elements introduced from period to an

initial system of complete central planning.

3.2.1. Central planning

Before 1978, it was a complete state planning system. The

central government was responsible for a few strategically

important national highways, and the local governments were

responsible for the construction and management of all

the other highways. Roads were considered a pure public

service. Investment funds came from state budget in the form

of a grant that did not carry any financial cost. Users did not

pay any toll, but they paid a monthly highway maintenance

fee based their vehicle tonnage. Because of shortage of funds

and lack of incentives, the development of highways was slow.

3.2.2. Decentralization

In the next stage, state investment funds in local projects were

changed from grants to loans in 1980 and the cost of

investment was shifted to the local governments. New fees were

introduced in the following years to increase the amount

of funds available for highway construction. Among the newly

introduced fees was vehicle purchase surcharge, which was

started in 1985. The surcharge was 10% of the price for

domestically produced vehicles and 15% for imported vehicles.

This

surcharge goes into the State Highway Construction Fund.

3.2.3. Introduction of tolls and their current regulation

Highway tolls were introduced in the third stage. It was first

experimented in Guangdong province in 1981 when the local

43. government borrowed from foreign investors to finance the

construction of four bridges along the Guangzhou–Zhuhai high-

way and raised funds to construct the Guangzhou–Shenzhen

highway. Tolls were collected to secure the financing of these

projects. Gradually, toll collection became a widespread

practice in the whole country.

Currently, highway tolls are regulated by the Highway Law that

was promulgated in 1997 and revised in 1999 and 2004.

Among other aspects, the law regulates the types of highway

that are eligible for toll, the number of years in which tolls can

be collected on a highway, the toll rates, the transfer of the

right for toll collection, the setting up of toll gates, and the

coor-

dination between provinces when the highway crosses the

provincial border.

According to the law, only three types of highways are eligible

for toll collection. One type includes highways built by

local governments above the county level with loans or funds

raised from enterprises and individuals. The second type in-

cludes the first type of highways of which the right for toll

collection has been transferred to an enterprise. The third type

includes highways built with investment from enterprises. The

first type is called government highways with loans to be

paid off (zhengfu huandai gonglu), and the remaining two types

are called commercial (jingyingxing) highways. All toll high-

ways must have technical grades and scales above government

specified thresholds.

The transfer of the right for toll collection has to be approved

by the Ministry of Transport for national government toll

highways, and the transfer has to be approved by the provincial

department of transport and submitted to the Ministry of

Transport for record for other toll highways.

44. The length of the toll period and the toll rates have to be

approved by the provincial department of transport. When the

right for toll collection of a government highway is transferred,

the length of the toll period should be agreed upon by the

two sides of the transaction and be approved by the authority

that approves the transfer. Toll rates have to be approved by

the provincial price regulator as well. The principle governing

the determination of toll period and rates is to allow the return

of the loans or funds raised for government highways and to

allow the return of investment with reasonable profits for com-

mercial highways. The toll period is also subject to State

Council regulation. According to the State Council Regulation

of Toll

Roads promulgated in September 2004, the maximum length of

toll period is 15 years for government toll roads in general

and 20 years for government toll roads in economically less

developed central and western regions; the corresponding max-

imum lengths for commercial toll roads are 25 and 30

respectively. The law and the regulation were not very clear

about

when the maximum toll period clock starts ticking when there is

a transfer of the right for toll collection. In some cases,

the clock starts from zero again after a transfer. There is clearly

a coincidence of incentives for both sides of the transfer

to agree on a longer period of toll collection. Meanwhile, the

two sides of the transfer often have close connection to the

government authority that is to approve the terms of transaction;

in the case of a government to enterprise transfer, the

transferor is the government authority. This loop hole is a

subject of much debate.

The setting up of toll gates must have the approval of the

provincial government. For highways that cross provincial

boundaries, the setting up of toll gates should be agreed upon

by all relevant provinces; if an agreement cannot be achieved,

45. the Ministry of Transport will make the decision. The principle

is to have unified collection and proportionate sharing of toll

fees.

3.2.4. Expansion of financing instruments

The institution of toll has paved the way for a wider range of

choices of financing instruments. There are several ap-

proaches one can take to finance highway construction in

addition to bank loans. One is to form a joint stock company

and raise funds in the form of equity investment. Another is to

issue bonds. The builder can also choose to sell the right

to operate to other investors or even go through an initial public

offering after the highway is completed and operated

44 C.-E. Bai, Y. Qian / Journal of Comparative Economics 38

(2010) 34–51

for some time and toll income becomes predictable. The fund

raised from the transfer of right to operate can be used to pay

off bank loans or build new highways. There are also cases in

which the builder of the highway raises fund by issuing asset

backed securities with future toll income as the underlining

asset. An early example is Zhuhai Expressway. In August 1996,

Zhuhai City Government registered Zhuhai City Expressway

Company in Cayman Islands and used it as a vehicle to issue

200

million US dollars of asset backed securities. The proceeds of

the issue were invested to build railway and expressway be-

tween the cities of Zhuhai and Guangzhou.

3.3. Investment incentives

3.3.1. Sources of investment

According to the 2006 and 2007 Statistical Report for the

Development of the Road and Waterway Transportation Sector

46. published by the Ministry of Transport (various years), total

investment in road transport was 623.1 billion in 2006 and 649

billion in 2007. In contrast, total fiscal revenue of all levels of

governments was 3876 billion yuan and the total spending on

infrastructure from government budget was only 439 billion

(NBS, various years); that is, total investment in transport was

16% of all government revenue and 142% of government

budgetary spending on infrastructure. Clearly, it is impossible

to

finance the investment in road transport all by government

budget. Most of the funding has to come from other sources.

Table 4 shows the split of investment funds between central

budget and local funds, between domestic investment and

overseas investment, and between investment made by state-

controlled institutions and other firms. According to the Table,

the lion share of the investment is made by state-owned

enterprises, mostly controlled by local governments, including

pub-

licly listed companies in which the government has a

controlling share. In 2006, 604 out of 648 billion yuan of

investment

was made by these enterprises.

The records of the 12 publicly listed expressway companies are

also consistent with the above observation. Nine of the 12

companies are controlled by a holding company wholly owned

by a provincial government. Of the remaining three, North-

east Expressway Co. Ltd. is jointly controlled by the provincial

governments of Heilongjiang and Jilin; Huabei Expressway Co.

Ltd. is controlled by one of the largest state-owned enterprises,

China Merchants Group, through its expressway investment

arm Huajian Transportation Economic Development Center,

with Tianjin, Beijing, and Hebei governments as large

sharehold-

47. ers; Shenzhen Expressway Co. Ltd. is controlled by the city

government of Shenzhen, even though its largest shareholder is

Hong Kong Securities Clearing Company Ltd. Interestingly,

China Merchants Group is among the top three shareholders in 8

of the 12 publicly listed expressway companies, holding on

average 21% of the equity shares of these companies. The local

government owned controlling shareholders are generally under

the direct control of the local departments of transport, and

their average shareholding in these 12 companies is 42%. Other

large shareholders are asset management funds.

We use Jiangsu Expressway Co. which has 27 billion yuan of

assets, the largest among all publicly listed expressway com-

panies, to illustrate the ownership structure. Its controlling

shareholder is Jiangsu Transportation Holding Company, a

wholly state-owned enterprise under the provincial government,

and it holds 54.44% of Jiangsu Expressway Co., China Mer-

chants Group owns 11.69% and other eight largest shareholders

are J.P. Morgan Chase & Co., UBS AG, Sumitomo Mitsui Asset

Management Limited, HSBC Halbis Partners Limited, Schroder

Investment Management Limited, and three securities com-

panies in China.

According to the Statistical Report for the Development of the

Road and Waterway Transportation Sector published by the

Ministry of Transport (various years), the most important source

of the investment in road transport is bank loan, which ac-

counts for 40.7% of the total in 2006. The loans are backed by

government guarantees and toll revenue. The second most

important source is fund raised by the local government or

enterprises controlled by them, which accounts for 32.8% of

the total in the same year. Central government funding is small,

and is mainly used to subsidize the construction of national

trunk roads, road construction related to poverty reduction and

national defense. It comes from central government bond

and vehicle purchase tax. Few intercity highways are built

48. entirely with funding from government budget.

3.3.2. Incentives and problems

How can these enterprises yield sufficient returns to their

investment so that investment in road transport is sustainable?

One of the most important reasons is highway toll and the

regulations about toll. As long as the highway is not built only

with government budget and satisfies some technical conditions,

the operator is entitled to collect tolls on the highway.

Table 4

investment in fixed assets in urban area by jurisdiction of

management and registration status: road transport (unit =

billion yuan).

Year Total By jurisdiction By registration status By registration

status

Central Local Domestic HK, Macao, Taiwan Foreign State

Collective Private

2004 466.55 20.07 446.48 462.65 2.69 1.21 444.21 3.33 1.98

2005 558.14 28.44 529.70 550.58 4.98 2.58 520.31 4.21 4.22

2006 648.16 16.40 631.77 640.85 5.34 1.98 604.35 14.91 24.35

Sources: China Statistical Yearbook 2005–2007 (NBS, various

years).

C.-E. Bai, Y. Qian / Journal of Comparative Economics 38

(2010) 34–51 45

The principle governing toll collection is that the operator can

recover the cost of investment. In the case where the operator

is an enterprise, the regulation on tolls also guarantees a

reasonable rate of return in principle.

49. The commitment of the regulation to guarantee the recovery of

investment cost or reasonable return to investment is

credible because most of the operators of toll highways have

strong connections to the regulator. The more likely problem

is regulatory capture by the operator, rather than lack of

commitment from the regulator. One example of capture is

extend-

ing the toll period beyond what is allowed by the State Council

regulation using loopholes therein regarding the transfer of

toll rights that we discussed above. Such an environment may

not be the first best for public interests, but in the case where

demand is strong and willingness to pay by the users is high, the

efficiency loss from capture may be lower than that from

lack of commitment.

Dealing with toll regulation is not the only area in which

government connection helps. We again use Jiangsu Expressway

Co. as an example to illustrate areas in which government

connection is important in the highway business. One is project

approval and toll regulation. When the company wanted to

upgrade the Shanghai–Nanjing Expressway in 2004, it needed

the approval of National Development and Reform Commission

of the central government. To recoup the cost of the upgrade,

it needed the approval of the provincial government to extend

the toll period for 5 years beyond the original toll period.

When they wanted to upgrade the Shanghai–Nanjing grade-two

highway to grade-one highway, they again needed the ap-

proval of the provincial government to extend the toll period by

12 years. The second is tax concession and land concession.

Companies can get tax exemption, reduction, or rebate when

they invest in key basic infrastructure. However, these conces-

sions have to be negotiated with the Department of Finance of

the province and approved by the Ministry of Finance of the

central government. The situation with land concession is

similar. The third is government help with commercial

financing.

50. To get bank loans, the company needs loan guarantee from

qualified entities. In the case of Jiangsu Expressway Co. loan

guar-

antee has been provided by its largest shareholder, Jiangsu

Transportation Holding Company, a wholly state-owned enter-

prise. Government connection has also been crucial for the

company to get approval for private placement of its shares

before its IPO and its listing on Hong Kong Stock Exchange and

Shanghai Stock Exchange. The last item is future investment

opportunities. Excluding those held by Jiangsu Expressway Co.

Jiangsu Transportation Holding Company still holds 2016 km

of expressway in its portfolio. The rights to operate these

expressways are potential investment opportunities for Jiangsu

Expressway Co. Similar to getting favorable terms of toll

collection, other benefits from government connection discussed

here also promotes investment.

The importance of government connection is not without its

costs. One result is that there are very few private firms

engaging in the highway business and another is that there is

very little foreign direct investment in the sector, as Table 4

shows. Another barrier for private firms to enter the business is

that a highway company has to have at least 30% equity to be

eligible for bank loans. Given the policy risks involved with

highway projects, it is very hard for private investors to raise

such fund.

The dominant role played by the government in highway

development comes with high political costs. Corruption is ram-

pant in this sector. Since 1997, 20 director generals or deputy

director generals of various provincial departments of trans-

port have been convicted of bribery. In the case of Henan

province, three consecutive director generals have been

convicted

of the crime one after the other in unrelated cases. The

provincial departments of transport have almost unchecked

51. power in

offering highway construction contracts, even though the

contracts are ostensibly offered by a tender process. In some

cases,

the officials leaked the reservation price to some bidders. The

officials also control a large sum of highway construction funds

and can allocate the funds to lower level highway authorities

with much discretion. The reason for the high incidence of cor-

ruption in this sector is not lack of penalty. Of the twenty cases

above, there are five death penalties. The temptation is so

strong that even the risk of death penalty cannot deter

corruption. Table 5 presents a list of bribery cases involving top

pro-

vincial transport officials.

3.3.3. Rates of returns to investment

To quantify investment incentives, we estimate the rate of

return to investment. Using data from the annual reports of the

12 publicly listed expressway companies, we find that the

average rate of return on equity is 10.5%, with an average

leverage

ratio of 40%.

We also try to estimate the rate of return to investment for the

whole sector. The National Bureau of Statistics of China

provides data on investment and the breakdown of value added

for the transport, storage and postal service sector. This in-

cludes all modes of transportation plus storage and postal

service. We use two methods to estimate the rate of return in

this

sector. One method is similar to the one used in Bai et al.

(2006). This method deducts economic depreciation from capital

income to get the net rate of return. The other method uses

accounting depreciation. More detailed description of data and

estimation method is given in Appendix A. The estimated rates

of return to capital are given in Fig. 11. The rates of return in

52. the transport, storage, and postal service sector are very

respectable; they compare favorably with the rate of return to

cap-

ital of the whole economy net of urban residential housing

estimated by Bai et al. (2006).

Fig. 12 shows the composition of fixed asset investment in the

transport and postal service sector in 2006. Investments in

highway transport and railway transport together account for

76% of the total. We will show later that the rate of return to

capital in the railway sector is much lower than the estimated

rate of return in the whole transport and postal service sector.

Therefore, we can speculate with some confidence that the rate

of return to investment in the highway transport sector

should give the investors strong incentives to invest.

Table 5

Top provincial transport officials convicted of bribery.

Year Province Rank of the official Penalty

1997 Henan Director general 15 years

2000 Sichuan Director general Death, commuted

2000 Sichuan Deputy director general Death

2001 Henan Director general Life

2001 Hunan Deputy director general Life

2002 Guangxi Deputy director general 11 years

2002 Guangdong Deputy director general 13 years

2003 Guizhou Director general 17.5 years

2004 Guizhou Director general Death

2004 Heilongjiang Deputy director general Life

2004 Yunnan Deputy director general 2.5 years

2005 Guangdong Director general 13 years

2005 Beijing Deputy director general Death, commuted

53. 2006 Henan Director general Life

2006 Jiangsu Director general 20 years

2006 Anhui Director general 10 years

2006 Hebei Deputy director general 14 years

2007 Zhejiang Director general Life

2008 Fujian Deputy director general Death, commuted

Xinjiang Director general No news of conviction

Source: collected by authors.

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97

98 99 00 01 02 03 04 05 06

Year

net of accounting deprecition net of economic deprecition

Fig. 11. Rates of return to capital: transport, storage, and postal

service. Sources: authors’ calculation, see Appendix A for

details.

58%

18%

54. 9%

7%

4%

3%

1%

Highway

Railway

Waterway

Urban Public

Aviation

Storage

Others

Fig. 12. Composition of fixed asset investment in transport and

postal service sector. Sources: China Statistical Yearbook

(NBS, 2007).

46 C.-E. Bai, Y. Qian / Journal of Comparative Economics 38

(2010) 34–51

4. Railway

4.1. Evolution of policy

4.1.1. 1949–1982: rigid planning and low prices

The Ministry of Railway was part of the rigid planning system.

There was no separation of government functions with

55. business activities. The Ministry of Railway had very little

autonomy and the local railway bureaus had even less. Prices

were

uniformly set by the central authority. In 1955, the price was

0.0165 yuan per ton-kilometer for freight and 0.0149 yuan per

person-kilometer for passengers. By 1967, the freight price had

dropped to 0.01438 yuan per ton-kilometer.

C.-E. Bai, Y. Qian / Journal of Comparative Economics 38

(2010) 34–51 47

4.1.2. 1982–1985: greater local autonomy and some profit

retention by the railway system

Some autonomy on planning, finance, employment, personnel

decisions was given to the local bureaus of railway. At the

same time, the railway system could retain some profit

according to a formula after tax payment. Railway service

prices

were increased but they still lagged behind the general price

level. Compared to 1955, the 1986 freight price dropped by

20.8% relative to the consumer price index and passenger price

by 15.7%.

4.1.3. 1986–1992: financial independence of the railway system

In March 1986, the State Council gave the railway system

greater financial autonomy and responsibility. The railway sys-

tem was exempt from income tax and a few other taxes. The tax

revenue and profit that were previously paid to the State

Treasury were now retained by the Ministry of Railway to

invest in the railway system. The railway system was separated

from state finance but the railway system itself was still the

same entity that combined government functions with business

56. activities. In this period, prices were increased by very large

margins.

4.1.4. 1993–2002: corporatization

In 1993, the railway system started experimenting with

corporatization. Guangdong railway bureau was restructured

into a corporate group in February, 1993. Then Dalian railway

bureau became Dalian Railway Limited in 1995. Guangz-

hou–Shenzhou railway was publicly listed in Hong Kong and

New York in 1996. The whole system went through corpora-

tization in 1999. Five non-core businesses including

engineering, construction, equipment, materials, and

communications

were separated from the Ministry of Railway and became

independent enterprises in 2000. The corporatization effort at-

tempted to separate government functions from business

activities in the system. In the same period, the price policy be-

came more flexible. Some variation is allowed in prices. Prices

were allowed to depend on the quality, route, and season

of the services.

4.1.5. 2002 – now: more price flexibility

The National Planning Commission issued a document in 2002

that allowed a lot more flexibility in railway prices. The

document referred railway prices as under government guidance

rather than determination. The document specified ranges

for price adjustment, instead of exact prices. Within the range,

the Ministry of Railway has the authority to approve the

application of price adjustment submitted by local railway

bureaus. Public hearings are also conducted before main price

adjustments are made.

4.2. Investment

57. As shown in Fig. 13, fixed asset investment in the railway

sector went through a few steps. It was more or less stable in

each of three periods: at around 20 billion yuan a year between

1991–1992, 57 billion yuan a year between 1993–1997, and

87 billion yuan a year between 1998 and 2004. However, it has

been increasing very rapidly since 2004. The growth rates are

51%, 52%, and 22% respectively in 2005, 2006, and 2007. One

possible reason for the recent rapid growth is the adoption of

the ‘‘medium and long term plans for railway network” by the

state council in 2004 (SCC, 2004). The plan includes a target

growth of 39% in the total length of railways from 2002 to

2020. The target was recently revised up to 67% (SCC, 2007).

From

Fig. 14, we can see that more than 80% of the investment in

basic construction in the sector has been made by the ministry

of

railway. Table 6 shows that almost all the fixed asset

investment is made by domestic state-controlled organizations,

and

around 90% of the investment is made by the central

government. Table 7 shows that state budget plays the most

important

in fixed asset investment in the railway sector. All these

observations are quite different from the electricity and

highway

sectors.

0

50

100

150

200

58. 250

300

1991 1993 1995 1997 1999 2001 2003 2005 2007

Year

Fixed Asset Investment in Railway (unit = billion yuan)

Capital Construction Improvement Vehicle Purchase

Fig. 13. Fixed asset investment in the railway sector: 1991–

2007. Sources: Yearbook of China Transportation and

Communications (CCCTCY, various years);

Statistical Communiqué of Ministry of Railway (MOR, various

years).

82.0%

84.0%

86.0%

88.0%

90.0%

92.0%

94.0%

96.0%

59. 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Year

Fig. 14. Share of capital construction investment made by the

ministry of railway. Sources: Statistical Communiqué of

Ministry of Railway, 1998–2007

(MOR, various years).

Table 6

Investment in fixed assets in urban area by jurisdiction of

management and registration status: railway (unit = billion

yuan).

Year Total By jurisdiction By registration status By registration

status

Central Local Domestic HK, Macao, Taiwan Foreign State

Collective Private

2004 84.63 75.27 9.36 84.63 0.00 0.00 83.78 0.42 0.04

2005 126.77 112.18 14.59 126.72 0.00 0.04 124.45 0.99 0.05

2006 196.65 176.55 20.11 196.56 0.03 0.07 191.79 3.61 1.16

Sources: China Statistical Yearbook, 2005–2007 (NBS, various

years).

Table 7

Source of funds of investment in urban area by sector: railway

(unit = billion yuan).

Year Total By sources of funds

State budget domestic loans Foreign investment Self-raised

funds Others

60. 2004 82.95 32.27 17.85 0.47 25.26 7.10

2005 128.84 44.62 33.37 3.03 38.84 8.98

2006 194.56 58.76 33.15 2.49 71.05 29.10

Sources: China Statistical Yearbook, 2005–2007 (NBS, various

years).

48 C.-E. Bai, Y. Qian / Journal of Comparative Economics 38

(2010) 34–51

From Table 8, we can see that the railway system has been

profitable since 1998. However, the rate of return to invest-

ment in railway is low. Fig. 15 shows the rate of return to

capital since 1991. The rates are low in recent years even when

taxes are included in capital income. Given these low rates, it is

hard to imagine profit-oriented enterprises would have any

incentives to investment in the railway sector.

5. Conclusion

Of the three sectors we consider in this paper, railway stands

out being very different from the electricity and highways

sectors. The electricity sector, both in terms of installed

capacity and output, has kept in pace with the growth of the

econ-

omy, and so has highway transport in terms of business volume.

The growth in the length of expressways has also been phe-

nomenal. The railway sector, however, has seen its business

volume growing much slower than GDP for both passenger and

freight, and its share in the transport market shrinking fast. Its

route length has grown at the lowest rate among all major

modes of transportation.

One major difference between the railway sector and the other

two sectors is that the former is still very centralized and

its business is still essentially run by the central government,

specifically the Ministry of Railway. Almost all of the invest-

61. ment is made by the ministry. In contrast, in the electricity

sector and the highway sector, there is much autonomy at the

provincial level and at the enterprise level. Enterprises in these

two sectors have very strong profit orientation and many of

them are publicly listed companies, even though the government

often maintains a controlling share of them. Local govern-

ments are also motivated to help enterprises in the two sectors.

In the electricity sector, local governments compete for

investment in their region to increase their tax base, by offering

land concession among others. In the highway sector, local

governments are often one of the owners of the highway

companies and their incentives to help the companies are also

very

strong. Competition among enterprises created by

decentralization is another factor that drives investment in the

electricity

sector.

Prices in the railway sector are yet to be determined on

commercial basis, despite a general trend of relaxation of price

rigidity. Other goals dominate commercial viability in

determining the prices. There are clear indications that prices

are too

low for efficiency. According to the Development Research

Center of the State Council (2005), only 30–40% of the demand

for

railway freight transport is met. The shortage of railway

transport supply is especially severe for the transport of coal. It

is

Table 8

Financial indicators of the railway system (1991–2007).

Year 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

63. 640 713.3 787.2 865.6 929.4 1055

Net value of fixed

capital

101.1 107.2 119.6 219 240.9 288.2 311.4 345.8 381.8 383 458.4

515 565.8 628.8 666.8 769.7

Sources: Year Book of China Transportation and

Communications (CCCTCY, various years); Statistical

Communiqué of Ministry of Railway (MOR, various

years).

-0.050

0.000

0.050

0.100

0.150

19

91

19

93

19

95

19

97

19

64. 99

20

01

20

03

20

05

Year

Net of Taxes Gross of Taxes

Fig. 15. Rate of return to capital of the railway system (1991–

2006). Sources: Authors’ calculation based on data from Year

Book of China Transportation and

Communications (CCCTCY, various years).

C.-E. Bai, Y. Qian / Journal of Comparative Economics 38

(2010) 34–51 49

sometimes difficult for passengers to get tickets too. As a result

of the low prices, the rate of return to investment in the rail-

way sector is very low and it is impossible to attract profit-

oriented investors in the sector. In contrast, prices in the other

two sectors are mostly determined according the principle that

the recovery of investment cost and sometimes reasonable

rate of return to investment are guaranteed. As a result, the rate

of return to investment is sufficiently high to attract invest-

ment in a sustainable manner. Of course, there is also risk that

prices in these sectors become too low due to political pres-

sure. Such pressure may affect investment incentives.

Observations suggest that investment in the railway sector is too

low. For example, even though there is clear advantage

65. of railway transportation of coal over highway transportation of

coal, the latter is still very common. About 25% of coal is

transported via highway out of Shanxi province, the largest coal

producing province in China. The province is investing

28.8 billion yuan to build more highways for coal

transportation. There is strong reason to believe that efficiency

should im-

prove if the capacity of the railway system increases to

accommodate such need for the transportation of coal. Recent

surge

in railway investment seems a welcome trend, but the new

investment is still made mostly by the Ministry of Railway, and

the jury is still out on whether it will be allocated to areas

where it is most needed.

The other two sectors are not without their problems. In the

highway sector, bureaucrats still have too much control over

the planning and approval of projects, the provision of loan

guarantee, the choice of contractors, the approval of toll terms,

and the approval of the transfer of toll rights. The relationship

between the bureaucrats and the enterprises in the sector is

too close. The resulting corruption problem is politically very