Télécharger en tant que PDF, PPTX

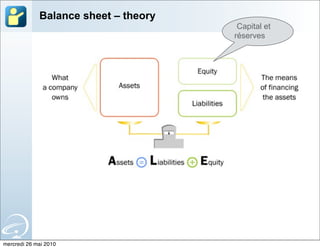

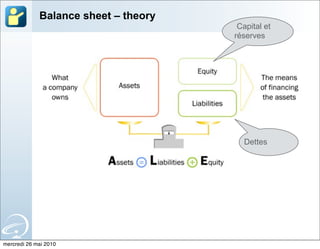

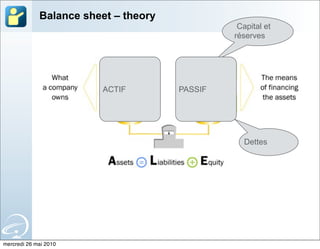

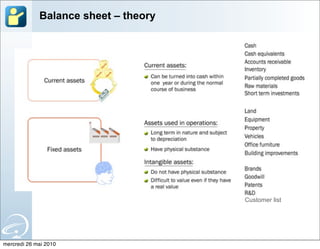

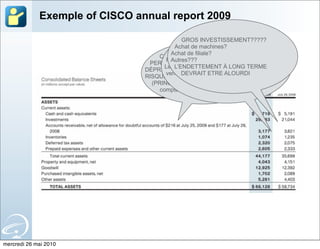

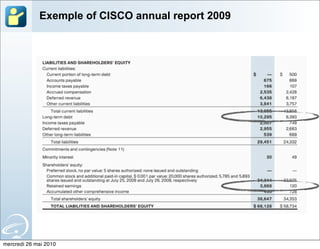

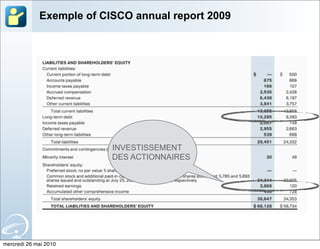

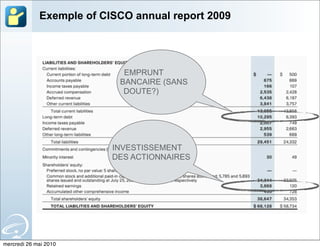

Le document est une introduction à la finance d'entreprise destinée aux étudiants en ingénierie informatique, abordant des exercices pratiques sur les bilans et les états financiers. Il couvre des concepts tels que le capital, les réserves, et la rentabilité, avec des exemples tirés de rapports annuels, notamment celui de Cisco. Des exercices pratiques sont également inclus pour illustrer l'impact de diverses transactions sur le bilan d'une entreprise.