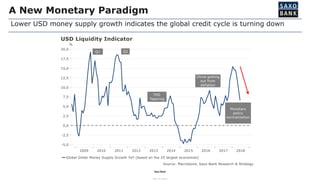

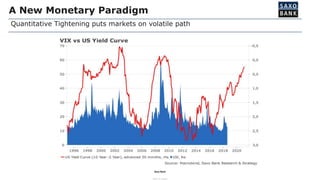

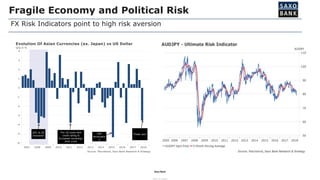

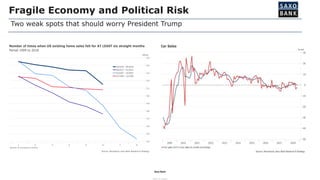

Le document présente des réflexions sur la normalisation de la politique monétaire et ses implications sur l'économie mondiale, signalant une fragilité accrue face aux risques politiques et économiques. Il souligne un changement vers des coûts de financement plus élevés, une volatilité accrue et une croissance plus faible, dans un contexte de resserrement quantitatif. L'analyse indique que, malgré des tentatives de relance en Chine, l'impulsion de crédit mondiale reste faible, marquant une approche vers la fin d'un cycle économique de près de dix ans.

![[FR] Column on European High Yield](https://cdn.slidesharecdn.com/ss_thumbnails/columneuropeanhighyieldfr-151005105753-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)

![Réunion apm 18 octobre 2016 apm paris tour eiffel [mode de compatibilité]](https://cdn.slidesharecdn.com/ss_thumbnails/runionapm18octobre2016apmparistoureiffelmodedecompatibilit-161019102222-thumbnail.jpg?width=640&height=640&fit=bounds)